Our guide to the Bank of England’s quantitative tightening

For all the recent talk of the Fed and ‘quantitative tightening’, it’s the Bank of England that’s poised to lead the charge on reducing the size of its balance sheet. Starting this week, policymakers are set to end a policy of reinvesting proceeds from government bonds maturing within its portfolio. We look at what this means for markets

What is the market impact of ending bond reinvestments?

The Bank of England is poised to hike rates to 0.5% this week. And this means that the Bank's own threshold for reducing the size of its balance sheet will be met.

According to guidance released last summer, step one of this process involves ceasing reinvestments of maturing government bonds entirely and immediately. That contrasts to the Federal Reserve, which is likely to take a more staggered approach by capping the volume of bonds rolling off the balance sheet each month

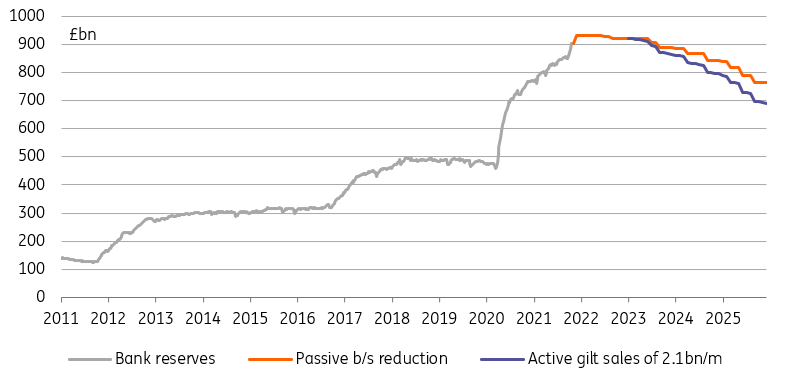

But despite this bolder start, the early phases of the BoE's balance sheet reduction (or quantitative tightening/QT) look manageable. Initially, it will simply amount to a large, predictable, and recurrent, buyer not turning up to buy gilts.

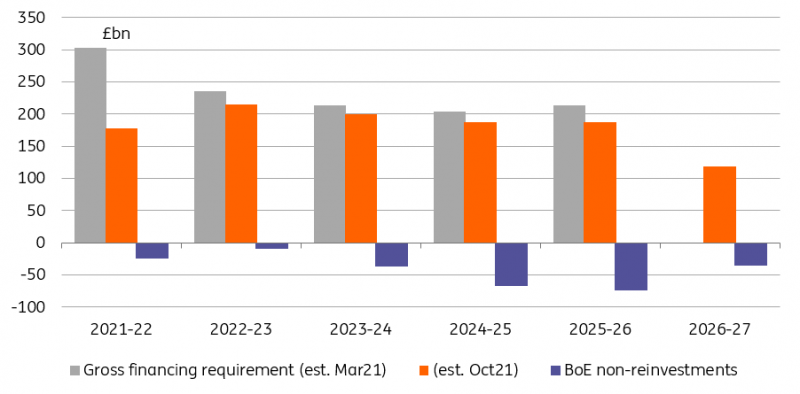

Assuming the Bank does end reinvestments altogether, this means £25bn of gilts will not be bought by the BoE this fiscal year (FY), compared to a counterfactual where it kept its balance sheet constant.

This is not a trivial amount, but it comes on the back of a substantial reduction in financing projections this and subsequent years. To put it into context, it compares with gross and net financing requirements of £178bn and £157bn for FY 2021-22 estimated by the Debt Management Office (DMO) last October. However as redemptions accelerate, and financing needs shrink, the shortfall for the DMO will peak in FY2024-25 and 2025-26.

An end to Bank of England reinvestments will create a demand shortfall for gilts

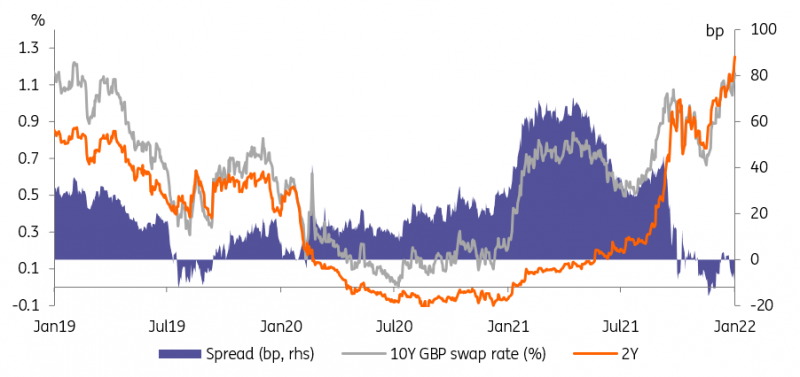

For markets, the logical conclusion would be that curve flattening pressure will ease this year as the BoE stops reinvestments. The BoE’s QE programme had a fairly long average duration, and the most recent iteration of purchases amounted to three weekly operations in the 3-7Y, 7-20Y, and 20Y+ maturity buckets.

But so far at least, it hasn’t played out this way. Private sector demand is solid and is expected to more than offset the BoE shortfall. Meanwhile, the BoE’s aggressive hiking campaign priced by the curve has displaced demand from short to long-end bonds.

Is this policy a substitute for rate hikes?

Probably not, at least initially. On the one hand, the Bank hasn’t done this before, unlike the Fed. Some of the more dovish policymakers may want to err on the side of caution and pause future rate hikes until the initial impact of QT becomes clearer.

Then again, Governor Andrew Bailey recently told the Treasury Select Committee that he expects the effect of ending reinvestments to be minimal, which we tend to agree with. He said, “We certainly cannot rely on it on its own” as a means of tightening policy, pointing towards possible symmetry between the latter stages of QE (where the market impact was much less than at the height of the market’s stress in spring 2020) and the early phase of balance sheet reduction.

We’d also note that the weighted average maturity of the Bank of England’s balance sheet is longer than that of the Fed. In other words, simply ending reinvestments will result in a more gradual unwind process in the UK.

In short, we are no longer convinced that ending reinvestments will hold the Bank back from hiking rates again over the coming months. Our most recent base case has another rate hike in August, though there’s clearly a chance that gets brought forward to May, or maybe even March, given the concern among policymakers about inflation.

Will the Bank be among the first to start actively selling bonds?

This is where things get more interesting. On top of ending reinvestments, the BoE said last summer that it would “consider” actively selling assets back into the market when the Bank rate hits 1% - something that could feasibly happen this year.

The motivation is understandable, given the relatively slow initial pace of balance sheet reduction that can be achieved by stopping reinvestments.

But it’s fair to say that actively selling bonds adds a number of extra complexities, not least how much to sell and how to sell it. What if markets entered a turbulent patch, would sales be paused or scaled back?

Governor Bailey said recently “we would not do QT during a period of financial instability”. And with that in mind, we suspect any foray into selling bonds would be fairly tentative. Based on the impact of QE in the previous cycle, we estimate that £25bn of gilt sales in any given year would have a comparable tightening effect on financing conditions as 0.125% to 0.25% of rate hikes.

BoE balance sheet reduction could accelerate with the active sale of gilt holdings

How could active sales work in practice, and what's the market impact?

Actively selling gilts is a process fraught with risks, many of which will only be known ex-post. So it is only natural for financial markets to bake a greater risk premium in anticipation of such an event.

‘Active’ QT could take one of many forms, each raising its own set of tricky questions, and each carries various implications for financial markets.

- Market neutral QT: It would basically work like QE, only in reverse. The BoE would set up auctions of bonds in their portfolio, with size proportional to their own holding in each maturity bucket. This option is the most ‘market neutral’ and predictable, but its disadvantage is that the BoE would be competing with the DMO in selling gilts. Market impact would be higher long-end rates and a steeper curve.

- Short-end QT: In this scenario, the BoE would only sell short-dated bonds in their portfolio (£291bn is sub-5Y, £432bn is sub-10Y) in order not to compete with the maturity buckets where the DMO is most active. The advantage is that market impact is more limited and the competition with the DMO is lower; the drawback is that this approach would reduce the scope for any ‘passive’ QT in the coming years if the BoE sells their short gilt holdings. The impact would be a flatter curve and potential disruptions in money markets.

- DMO QT: A final approach would be to convince the DMO to buy back old off-the-run gilts held by the BOE and to finance them by selling more on-the-run gilts via the usual auction/syndication process. This would leave the DMO in the driving seat in terms of debt management. The problem is that it might raise questions on Bank of England independence. The market impact in this case would be similar to ‘Market neutral QT’ but with fewer potential near-term disruptions, as there is only one seller and markets are used to the DMO’s way of operating.

Curve flattening pressure should ease with QT, but it hasn't played out that way yet

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article