OPEC+: Vienna waits for you

- 27 June 2019

The 1st and 2nd of July will see OPEC+ members meet in Vienna, where the main discussion will be whether the group extends its current production cuts into the second half of the year. We believe that broader macro uncertainty and concerns over demand will force OPEC+ to continue with the deal

Why is OPEC so afraid?

All was going to plan for OPEC+ earlier in the year, their production cut deal which was agreed at the end of last year had the desired impact of pushing prices higher. This was helped out by the fact that Saudi Arabia was cutting production by around 500Mbbls/d more than it agreed to over much of the deal, whilst exempt Iran continued to see flows edge lower as a result of sanctions. The expiration of waivers for buyers of Iranian crude oil only helped the market further.

However as we have moved through the year, the surprise breakdown of trade talks between China and the US, has re-ignited concerns over the impact trade tensions will have on the global economy, and as a result the knock on effect on oil demand growth. Furthermore the market has been too fixated on US inventory numbers, which have shown unusual builds over large parts of Q2, which is a reflection of prolonged refinery turnarounds, and unplanned outages. This is a trend we expect to reverse as we move through the summer months- we are already seeing run rates in the US recovering, and the EIA report this week showed the largest weekly fall in US crude oil inventories since September 2016

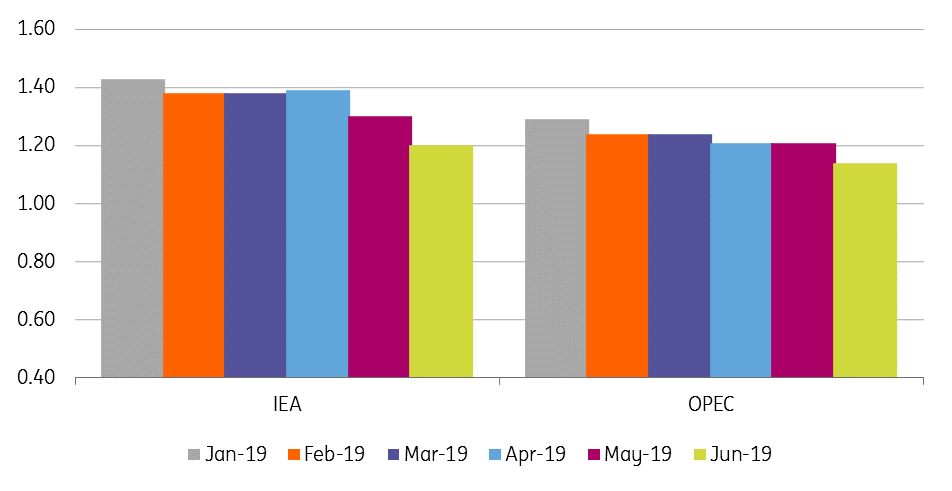

On the demand side, a number of agencies have slashed their demand growth forecasts for the year. The International Energy Agency are now forecasting that 2019 oil demand will grow by 1.2MMbbls/d over 2019, down from their forecast of 1.4MMbbls/d at the start of the year. A large part of this revision reflects weaker demand in the OECD over Q1, and in order to meet the IEA’s demand growth estimate for the year, growth will have to pick up over 2H19- something that will likely be dependent on how quickly a resolution can be found with current trade talks.

The sell-off that we saw in May, has shown OPEC+ how vulnerable the market is at the moment, with participants clearly concerned about the macro picture. It is because of this vulnerability that we believe that OPEC+ will decide to extend the deal of cutting output by 1.2MMbbls/d over the second half of the year.

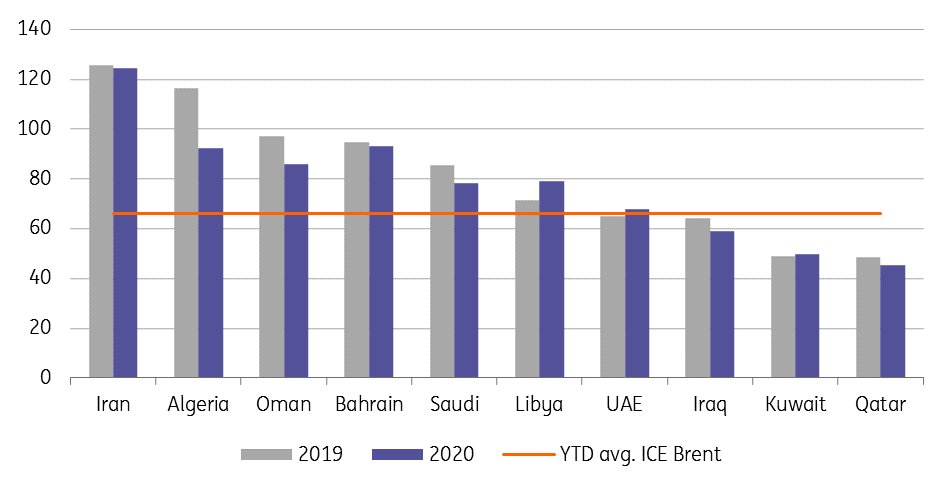

It is OPEC who have more to lose by not extending the deal, and this is evident through comments from a number of OPEC oil ministers in the lead up to the meeting, that they are confident that the deal will be extended. It comes down largely to fiscal breakeven oil prices- the Saudis have a breakeven price of around US$85/bbl, and so they will be concerned about potentially a widening gap between this level and where the market trades.

A no deal scenario does mean the potential for further speculative liquidation. Speculators are already concerned about broader macro concerns, and so ending supply cuts would likely make them only shy further away from the market. The managed money net long in ICE Brent has fallen from over 400k lots in early May to almost 270k lots as of the 18th June, whilst for NYMEX WTI the managed money net long has fallen from 314k lots in late April to around 147k lots as of the 18th June. Although admittedly, given the more recent rally in the market over 2H June, with the rise in Middle East tensions, these positions are likely to be somewhat larger at the moment.

Evolution of 2019 oil demand growth estimates (MMbbls/d)

Where’s the fire, what’s the hurry about?

As has become a common theme with OPEC+ meetings, there is always uncertainty around what Russia will do. They continue to take a more relaxed approach on whether the deal needs to be extended. Russia has a fiscal breakeven oil price below current levels, and so they are more comfortable with where the market is trading. The Russian energy minister just this week said that it is still too early to comment on whether the deal will be extended or not, and that a large part will depend on the outcome of the G-20 summit, where trade talks will resume between Trump and Xi.

However we do believe that at the end of the day, Russia will continue with cuts, given the risk that the market falls to levels where they do not feel so comfortable in the event of no deal.

Slow down, you’re doing fine

We continue to hold a constructive view towards the oil market, assuming that OPEC+ extends the deal. We are forecasting that prices will firm from current levels, with ICE Brent averaging US$69/bbl over Q3 and US$73/bbl over Q4. Furthermore lingering tensions in the Middle East should continue to offer some support to the market.

We should see a seasonal pick-up in demand over Q3, and this combined with continued cuts from OPEC+ and further declines from exempt Venezuela and Iran should see a tightening in the global oil balance.

While prompt ICE Brent time spreads have come off from their recent highs-reflecting more of a normalisation in Druzhba pipeline flows, the Aug/Sep spread is still trading at a healthy US$0.80/bbl, suggesting still a fairly tight prompt physical market. Meanwhile the forward curve continues to remain heavily backwardated.

Fiscal breakeven oil price (US$/bbl)

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

In case you missed it: It’s wait-and-see time

- This bundle contains 9 Articles