OPEC+ expected to ease cuts further

- 25 June 2021

- Commodities, Food & Agri Energy

OPEC+ is set to meet on 1 July to discuss what to do with output policy from August onwards. Given the recent strength in the market, there will be growing expectations for the group to increase supply. However, will an increase be enough to cool the rally?

Where are we now?

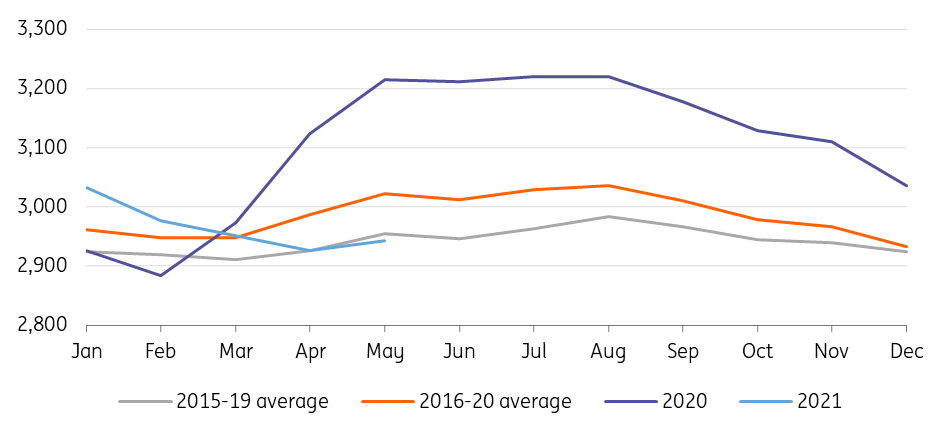

OPEC+ has done a great job in rebalancing the global oil market, following the Covid-19 induced demand hit. At its peak, OECD total oil inventories were more than 265MMbbls above the 5-year average in June last year. However, with unprecedented cuts from OPEC+, the group has managed in a little less than a year to bring OECD inventories back in line with the 2015-19 average. These numbers clearly ignore non-OECD countries, and as a result the large crude oil inventory builds seen in China. Over 2020, we estimate that China crude oil inventories grew by a little over 1.2MMbbls/d, whilst over the first 5 months of this year they have continued to grow on average by around 500Mbbls/d. However, the build in China in 2021 so far has been more concentrated to earlier in the year, with the last 2 months seeing stock drawdowns.

OECD total oil stocks (MMbbls)

The status of OPEC+ cuts

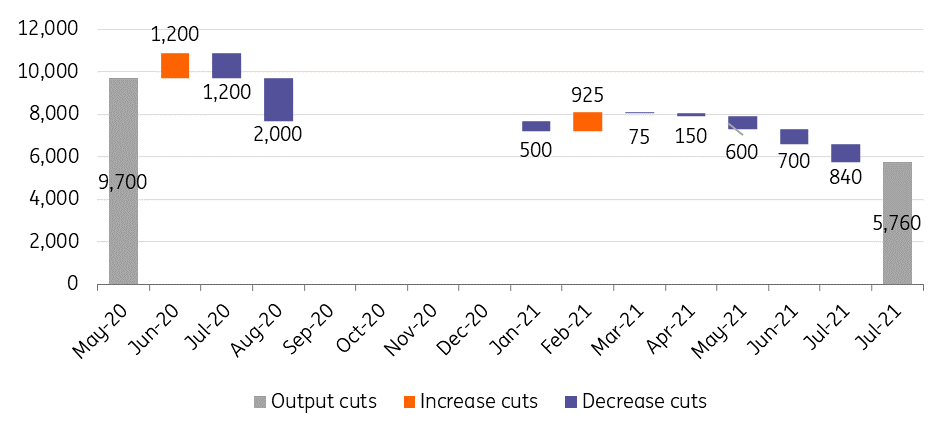

Since May last year we have seen record supply cuts from OPEC+. The group started with cuts of 9.7MMbbls/d, although given the high reference point used for the deal, the real cuts are somewhat smaller than the headline numbers suggest. Over time the group has gradually eased these cuts, and by the end of April 2021, the group had brought back 1.8MMbbls/d of this supply to the market. The easing appears more modest due to Saudi Arabia’s additional voluntary reductions.

From May this year, the group started to bring supply back onto the market at a quicker pace, with OPEC+ comfortable with the level of inventory drawdowns. Between May and July, the group agreed to return 2.1MMbbls/d of supply. This includes Saudi Arabia ending the additional 1MMbbls/d of voluntary cuts it has made since February. It was agreed supply could increase in May, June and July by 600Mbbls/d, 700Mbbls/d and 840Mbbls/d respectively. However, due to some involuntary reductions, OPEC members fell short of the agreed supply increase in May. Under the deal, OPEC members could have increased supply by 527Mbbls/d in May, however, supply from them only grew by 390Mbbls/d MoM.

By the end of July, the group will still have 5.8MMbbls/d of supply to bring back to the market. The key question is how quickly this supply returns.

Evolution of OPEC+ supply cuts (Mbbls/d)

What will OPEC+ decide?

With oil prices holding firm, and Brent trading now above US$75/bbl, there will be growing pressure on OPEC+ to ease production cuts further when they meet on 1 July. Pressure will likely not only come from within the group, but there will also be growing calls from key consumers to cool the market down, as countries come out of the other side of Covid-19 lockdowns. India in recent months has made it clear that they would like OPEC+ to increase supply. Just this week, the Indian oil minister held a meeting with the OPEC Secretary General, where he asked the group to increase output, with stronger oil prices adding to inflationary pressures in India.

We believe that the group will at least need to increase supply by 500Mbbls/d in August, and we are already assuming a supply increase of this magnitude in our balance sheet. In recent days there have also been reports that the group is considering a similar increase. The Saudi energy minister has said that OPEC+ has a role to play in containing inflationary pressures.

The group would ideally like more clarity on the likely outcome of Iranian nuclear talks, and if we do see an eventual lifting of sanctions, how quickly this could happen. However, its looking unlikely that there will be a deal ahead of the OPEC+ meeting. But, given that Iran is unlikely to boost supply immediately, we do not believe that this should sway the group’s decision for August. However, it could have consequences on what the group decides for later in the year. Iran is currently producing around 2.4MMbbls/d compared to a pre-sanction peak of 3.8MMbbls/d.

Anything less than 500Mbbls/d from OPEC+ would likely be enough to see the bulls push the market higher in the near term. The group will likely continue to take a cautious approach, and so we believe that there will be reluctance from some members to increase supply by more than the previously agreed 500Mbbls/d monthly limit. The Saudi energy minister in recent days has mentioned that it is not clear if the price is rallying on the back of real supply and demand, or whether its due to optimistic expectations. So, the group will want to make sure that if they increase supply, that the demand is there.

The other big uncertainty is timing. While, the group will need to discuss what to do with supply for August, it is not known whether they will agree for increases for later months as well. Agreeing on supply increases for a longer period would provide more certainty to the market and could ease some worries over tightness. If the expected demand recovery fails to materialize later in the year, or if Iran does make a quicker than expected comeback, the group could always revisit its easing plan at one of the regular monthly meetings.

What does this mean for the price?

We continue to hold the view that ICE Brent will average US$70/bbl over the second half of this year, with OPEC+ still sitting on plenty of spare capacity, whilst there is the risk of increased Iranian supply if/when US sanctions are lifted. However, this view is assuming that OPEC+ brings this capacity back onto the market in increments of at least 500Mbbls/d per month. Anything less would likely increase the potential for further price upside.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more