Omicron caution keeps Bank of Canada on hold

- 26 January 2022

- FX Canada

We thought Canada’s first interest rate rise could come today, but the Omicron wave appears to have made the BoC hesitant. March 2nd should see rates raised, based on their upbeat assessment, with at least three further hikes likely in 2022. Our bullish view on CAD for the rest of the year remains unchanged

No change from the BoC

Going into today’s meeting we thought the chances were good for a 25bp rate rise. Admittedly only a third of economists predicted it would happen, but financial markets were more confident with it roughly 70% priced. After all the economy is booming, jobs are at record highs, inflation is at 30-year highs and Covid containment measures are starting to be eased.

Canada inflation at 30-year highs

Omicron delays the inevitable

The BoC do admit we aren’t far away, but the Omicron variant’s economic impact made them hold fire with them acknowledging that it “is weighing on activity in the first quarter” and they are not certain as to how long it will suppress growth. Nonetheless, they are of the view that it will be “less severe than previous waves” and economic growth will then “bounce back and remain robust over the projection horizon”.

In terms of inflation, “as supply shortages diminish, inflation is expected to decline reasonably quickly to about 3% by the end of this year and then gradually ease towards the target over the projection period.”

Given a decent economy and elevated inflation they expect that “interest rates will need to increase, with the timing and pace of those increases guided by the Bank’s commitment to achieving the 2% inflation target." They also expect to start shrinking the size of their balance sheet later this year. Once they begin raising rates “the Governing Council will consider exiting the reinvestment phase and reducing the size of its balance sheet by allowing roll-off of maturing Government of Canada bonds.”

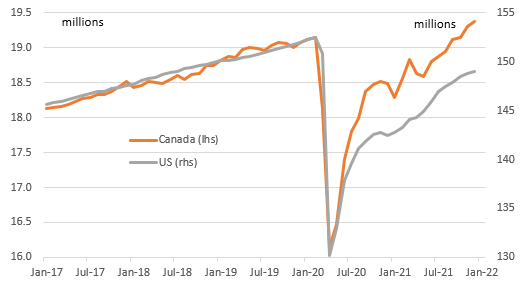

Canadian employment at record highs and is outperforming the US

A March hike the first of many

We expect the first interest rate now to come at the March 2nd policy meeting. The BoC acknowledged overall “economic slack [is] now absorbed” and that “the labour market has tightened significantly”. This is clearly evident in the chart above, which shows the outperformance of the Canadian jobs market versus the US’. Furthermore, the BoC’s own latest quarterly survey showed investment and hiring intentions are at record highs, which is consistent with our own GDP forecast of 3.5% for 2022 after 4.5% in 2021.

We are also less confident that inflation will fall as quickly as the BoC expect given supply chain strains and labour market shortages are showing little sign of easing. Consequently we see at least four rate rises in 2022 with the risks skewed towards the need for more aggressive policy tightening.

FX: Delayed hike is no game changer for the loonie

Markets had to price out today’s rate hike (which had around 70% of implied probability), which inevitably sent USD/CAD higher. However, the knee-jerk reaction in the pair saw the pair stall around 1.2640, indicating that there is not a strong appetite to turn bearish on CAD simply on the back of the BoC policy outlook. After all, the BoC statement clearly paves the way for a rate hike in March, which means that the prospect of five rate hikes in 2022 currently priced in by the market remains quite intact.

We continue to see the BoC tightening cycle as a positive factor for CAD in 2022, although external factors will play a big role too in directing the currency from now on. Assuming oil prices remain resilient and the global risk sentiment picture stabilises after the recent jitters, we think USD/CAD can stay on a downtrend for the rest of the year and hit 1.22 in 4Q22.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more