Oil demand uncertainties linger

- 23 September 2020

Price action in oil had been largely rangebound over the summer months. However a slower than expected demand recovery and returning supply has seen prices wobble more recently. While we still see prices moving higher from current levels, we have revised lower our price expectations due to the demand picture

Demand taking longer than expected to come back

Demand is the key uncertainty for the global oil market, and it is set to remain so, as long as Covid-19 disrupts our everyday life.

It has become clear that the recovery in oil demand from the peak lockdown period over 2Q20 is taking longer than many had initially anticipated. A resurgence in Covid-19 cases, continued remote working, and the fact that international travel remains heavily restricted is weighing on the recovery.

At the peak of the lockdown, global oil demand was estimated to have been down a little over 23MMbbls/d year-on-year in April according to Rystad Energy, while currently it is estimated to be down in the region of 8MMbbls/d YoY.

For full-year 2020, Rystad Energy is expecting demand to be down a little over 10MMbbls/d YoY. Then, as we move into 2021, demand is estimated to grow by almost 6.8MMbbls/d YoY, however, this still leaves it below 2019 demand levels. Over 2021, it continues to be the aviation industry that largely weighs on demand, with international air travel unlikely to return to anywhere near normal levels until there is a Covid-19 vaccine commercially available.

Chinese buyers take a step back

One of the key drivers behind the recovery in oil prices from their April lows was strong Chinese buying.

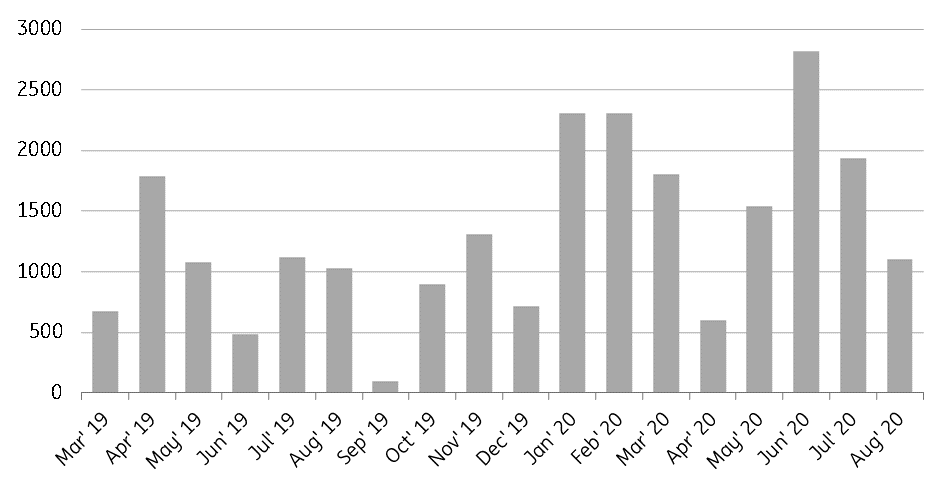

Imports in June hit an all-time high of just below 13MMbbls/d, up 34% YoY. Since then imports have eased, but we have still seen strong YoY growth. These imports do not reflect real consumption, instead, China has taken advantage of lower prices to stock up. The peak was in June, where the country appears to have added around 2.8MMbbls to inventories every day. Looking at the latest available data, in August, China added 1.1MMbbls/d to inventories.

One of the key drivers behind the recovery in oil prices from their April lows was strong Chinese buying, as they took advantage of lower prices to stock up

This should slow in the months ahead, with Chinese buyers noticeably quieter in the physical market, having stocked up already, as well as running low on available import quotas.

This has hit the physical market, with differentials weaker, and with a number of unsold cargoes from West Africa. There have been reports more recently that independent refiners in China are requesting for further import quotas to be issued for 4Q20, which if occurs could provide some needed support to the physical market.

China has built significant crude oil inventories in 2020 (Mbbls/d)

Refinery margins not providing much incentive

Another factor which has not been supportive for crude oil demand are weak refinery margins.

Globally refiners remain under pressure, with poor products demand, large product inventories and weak product cracks. As a result, there is little incentive for refiners to increase utilisation rates. According to IHS Markit, global refinery utilisation rates are below 75% currently, which compares to around 85% at the same stage last year.

While recent hurricane activity in the US Gulf hasn't helped, with some refiners in the region sustaining damages resulting in lower run rates. In addition, with refinery maintenance season approaching, this will likely weigh on crude demand further in the weeks ahead.

OPEC+ easing

The wobble in prices that we have seen more recently will be a concern for OPEC+, although they decided against recommending or taking any further action when the Joint Ministerial Monitoring Committee (JMMC) met on the 17 September.

The issue for OPEC+ is that as the demand recovery has slowed, and Chinese buying has disappeared while the group has eased output cuts. Between May and July, under the deal they agreed to cut by 9.7MMbbls/d (while for June, Saudi, the UAE and Kuwait decided voluntarily to cut by an additional 1.2MMbbls/d), and this was eased to 7.7MMbbls/d from 1 August.

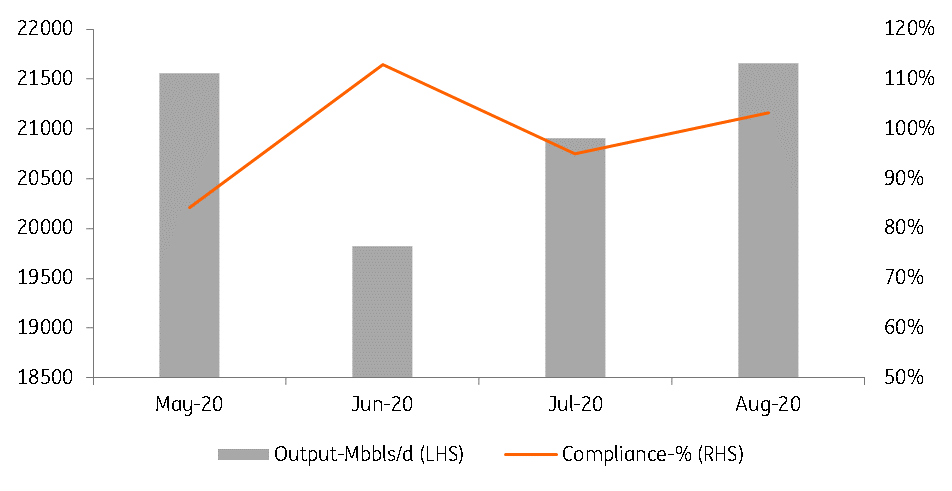

Meanwhile, and unsurprisingly there is always the issue of compliance, and at every OPEC+ JMMC, there is pressure on those producing above their quota to comply. The group have gone a step further this time, pushing those who have fallen short, to compensate for the lack of their compliance. While Iraq and Nigeria produced above their quota in the first few months of the deal, they do seem to be hitting compliance now, although will need to compensate for their previous poor performance in the months ahead. While more recently, the UAE has also started to slip with its compliance. However, according to the committee, compliance for the full group still came in at 102% in August.

More recently, OPEC member, Libya (which is exempt from the output cut deal, and has been suffering from near zero production due to an export blockade since the start of the year) looks set to see output return. Libya’s National Oil Corporation has lifted force majeure for a number of ports and facilities, whilst the East Libyan commander Khalifa Haftar has said that he will lift the export blockade from the country. This does suggest that in the coming months we could see Libyan supply increase from a little over 100Mbbls/d towards 1MMbbls/d. Libya’s NOC has said that output from the country is expected to reach 260Mbbls/d by next week. However as we have become accustomed to, it is safe to assume that Libyan supply will remain volatile moving forward.

OPEC-10 compliance (%)

Non-OPEC+ supply also returns

It is not just OPEC+ where we have seen supply come back to the market. The fairly strong and quick recovery we saw in prices from the April lows means that producers who had closed production, have brought it back fairly quickly.

This is most evident in the US, where producers have been very quick to bring back this production. US crude oil output bottomed out at a little over 10MMbbls/d in May, around 2MMbbls/d lower from the month before. But since May, output is estimated to be back in the region of 11MMbbls/d, although a fairly active hurricane season has meant that we have seen quite a bit in the way of supply disruptions in offshore US Gulf of Mexico.

While we have seen a short term bounce in US output, it is unlikely that output will continue to grow. Rig activity in the US has basically come to a standstill, and so it will be difficult to sustain current production levels, never mind grow it, unless we see a pickup in drilling. The industry will likely turn to completing drilled but uncompleted wells (DUCs), in an attempt to maintain output, and this is something we saw over August, with US DUC inventories edging lower.

Plenty of demand uncertainty, but market still set to move higher

Clearly how demand evolves is the big unknown, and so it is the key risk for the oil market. Further waves of Covid-19 and restrained air travel is a downside risk for demand and as a result prices.

However assuming that demand continues its gradual recovery, we believe that stocks will decline over 4Q20 and 2021, which should see prices trending higher from current levels. We do not believe that further waves of Covid-19 will lead to full lockdowns, instead, governments are likely to take a more targeted and localised approach. However we have revised lower our forecast for ICE Brent, and now expect prices to average US$47/bbl over 4Q20, this compares to our previous forecast of US$50/bbl. Meanwhile, for 2021, we have made some minor revisions, although the average for the year remains at US$58/bbl.

We have revised lower our forecast for ICE Brent, and now expect prices to average US$47/bbl over 4Q20

Apart from Covid-19 related demand risks, there are several other downside risks to our view. Firstly, is the OPEC+ deal, which is currently set to run all the way through 2021 and into 2022. If for some reason the deal was to fall apart, this would mean 5.8MMbbls/d additional supply coming onto the market in 2021, and this would be enough to push the market back to building inventories.

The second risk is related to US elections. The Trump administration has had a very hawkish stance with Iran, which saw the US re-implement sanctions against the country. If we were to see a Joe Biden victory, one would have to consider the possibility of the US lifting sanctions and rejoining the Joint Comprehensive Plan of Action. If this were to happen, we would likely see Iranian oil output recovering, leading to potentially more than 1.5MMbbls/d of supply returning to the market over time.

ING oil forecasts

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Covid spikes threaten the recovery

- This bundle contains 10 Articles