The irony of the financial system’s largest ‘known unknown’

- 29 June 2023

- Financial Institutions

Regulation helped Non-Bank Financial Institutions surpass banks in size. They are an increasingly important competitor, source of funding and client to banks. But their vulnerability and lack of transparency create the largest “known unknown” risk for the banking sector. Regulation will take time. Meanwhile, central banks may be forced to help out

Why you should know about NBFIs

Non-Bank Financial Intermediaries (NBFIs) have grown significantly since 2008 and as a result, the sector's influence has come under increasing scrutiny. Last year's UK gilt crisis was another wake-up call for regulators, with concerns rising over the growing vulnerabilities. Regulators across the globe are now asking for more and stricter regulation of these activities.

In contrast to NBFIs, banks have seen stricter regulation since the global financial crisis, leaving room for NBFIs to develop. However, in the face of the increasing complexity and interconnectedness of the sector, a severe shock to NBFIs could spread to banks, creating a new type of risk for the traditional banking sector.

NBFIs have many faces, including ones that can look like a bank

The term NBFI is used to describe a large variety of institutions. We are classifying them all as non-banks that take in cash and use it to generate a return. Most NBFIs take in cash, just as banks do, and deploy it in various securities and derivatives. The Financial Stability Board (FSB) monitors NBFI activity and divides the sector in two:

- NBFIs not engaging in credit intermediation nor bank-like activities (about 75% of the sector).

- All the entities which have bank-like activities, also called the “narrow measure”, where Money Market Funds and Fixed Income Funds make up the largest part (for other economic functions, see annex).

Another way of looking at NBFIs is simply by dividing them into the main components such as:

- Insurance Corporations (ICs)

- Pension Funds (PFs)

- Other Financial Institutions (OFIs), such as Investment Funds and Money Market Funds

- Financial Auxiliaries (FAs), such as insurance brokers and captive financial institutions.

Fast growth made NBFIs much larger than the banking sector

The stricter capital and liquidity requirements on banks put in place after the global financial crisis - notably through the implementation of Basel III - made some parts of lending less attractive for the banking sector. NBFIs were already present before 2008 but stepped in to take over portions of this business as regulatory requirements grew for banks. The IMF highlights that NBFIs have become a crucial driver of global capital flows for emerging markets and developing economies. Looking into the different NBFI components and sampling 21 major global economies and the euro area (list of countries in the annexes), the FSB reported strong growth for the sector in 2021, at 8.9% year-on-year. This is a significant development as the sector has seen average growth of just 6.6% over the last five years.

The NBFI sector has grown in every component since 2019 to reach $239.5tn

The component with most important growth is OFIs

The IMF estimated the size of the sector in more detail by looking at the respective share of the Global Financial Assets for each sub-sector of NBFIs.

Investment funds are the most important NBFI sub-sector representing 12% of global financial assets

Insurance companies and pension funds follow, at 9% of the global financial assets

Overall, these institutions now represent a 49.2% share of total global financial assets, surpassing banks at 37.6%. The rest of the market is composed of central banks and Public Financial Institutions.

The NBFI sector has more than doubled since 2008

In 2021, it reached 49.2% of total global financial assets with banks representing 37.6%

NBFIs represent 63% of national financial assets in the US. In the eurozone, the sector is less significant though it has still doubled in size since the global financial crisis.

Total NBFI assets in the euro area have doubled since 2009

Euro area NBFI assets diminished in 2022 as the sector sold higher risk assets acquired during the low interest rate period

Relative to the banking sector, NBFIs remain less important: The European Central Bank noted that the sector had reached about 80% of the size of the banking sector in the eurozone in 2022. This is significant but remains much smaller when considering the size of the sector globally.

In both geographies, the sector has developed significantly after taking a hit during the global financial crisis, benefiting from the stricter regulations on banks and the search for higher returns. In its 2023 financial stability report, the IMF highlighted that the previous low interest rate environment had prompted NBFIs to shift their investments to riskier assets in the hope of finding higher returns. But with rising yields and a worsening outlook for credit risk, NBFIs have started to sell their riskier assets. With this development comes recent concerns over increasing NBFI vulnerabilities.

The share of both banks and non-banks in relation to total domestic financial assets differs significantly between countries.

Luxemburg, Ireland and the Netherlands have very important NBFI sectors, the first two because they host many investment funds as the latter has a large pension fund sector. On the other hand, in France and Spain, total domestic financial assets remain mostly dominated by traditional banks. Variations in the NBFI sector size and type between Europe and the rest of the world, and also between European countries, indicate that Europe not equally exposed to the NBFI sector’s vulnerabilities.

NBFI share of total domestic financial assets varies significantly between countries

In Europe, the share of NBFIs of total domestic financial assets is the highest in Luxemburg

The sector is facing three main vulnerabilities

Non-Bank Financial Intermediaries were thrust into the spotlight once again this year following the recent turmoil in the banking sector. The main concerns arise from the lighter regulations and consequent lack of data and estimation of their risk exposure. While it remains difficult to clearly assess the sector’s exact exposures, international institutions identify three main risk factors stemming from the current state of the sector namely: financial leverage, liquidity risk and interconnectedness.

1. High financial leverage in times of lower interest rates

Low interest rates in recent years and asset price volatility incentivised investors to use leverage to boost returns. However, the level of vulnerability from leveraging has proved to be difficult to estimate both for authorities and market participants. The significant lack of data makes a concrete estimation of the risk challenging. Furthermore, the IMF has stressed that financial leverage used by NBFIs comes in many forms, such as the use of repurchase agreements, margin borrowing in prime brokerage accounts, or synthetic leverage associated with the use of various financial derivatives (like futures and swaps).

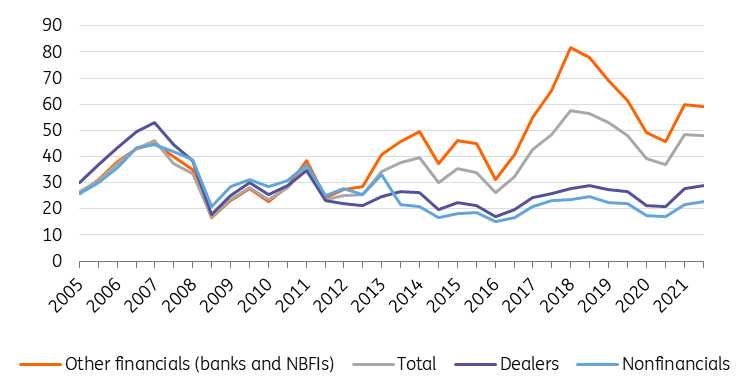

The recent focus on the use of leverage comes from the increased risk of financial distress due to the higher vulnerability to sudden changes in asset prices as interest rates increase rapidly. This may force NBFIs to de-lever, amplifying the initial price decline, with the gilt crisis being a case in point. The graph below from the IMF highlights well the recent increase in the use of synthetic leverage (where banks and NBFIs are lumped together), hence the growing vulnerability to sudden interest rate shocks.

The proxy for synthetic leverage shows an increase in leverage use by banks and NBFIs since 2016

The use of leverage dropped between 2018 and 2020 before spiking again until 2021 and stabilising today

2. A lack of liquidity could exacerbate financial market stress

Liquidity risks can come in different shapes and forms. In its 2023 Financial Stability Report, the IMF highlights several types of NBFI vulnerabilities linked to liquidity.

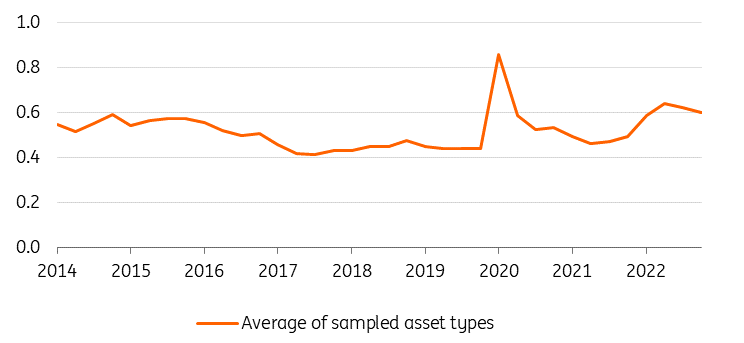

NBFIs tend to have a liquidity mismatch by holding relatively illiquid assets while sometimes allowing investors to redeem shares daily. This practice is not new as pre-2008, shadow banks were already making use of such a mismatch. The recent evolution in the sector highlights an increase in the liquidity mismatch of the assets held by NBFIs. Looking into the vulnerability measure capturing weighted average funds owning an asset and defining liquidity as the portfolio-level bid-ask spread across funds, the following graph from the IMF clearly highlights this point. It shows the spike in vulnerability to liquidity mismatches as Covid hit but also the more recent increase. While not as significant as the spike seen during the pandemic, recent trends are a reminder that the sector is still vulnerable to changes in liquidity, which can often worsen in times of stress.

Average liquidity mismatch has increased since the Covid crisis

The liquidity mismatch index, which spiked in 2020 and again over 2022, is now showing a decline

Furthermore, the combination of financial leverage and lack of market liquidity can lead to a decline in asset prices and a deterioration of funding liquidity (liquidity spiral). For most NBFIs, there is a risk that investors withdraw funds, especially when asset values drop, although for some there may be notice periods to negotiate. For example, hedge funds traditionally have a lockdown period under which there can be no withdrawals. If enough forced selling occurs, it adds to the pressure on the asset side, resulting in something of a death spiral.

In 2022, the period of stress in UK pension funds started with concerns about the UK fiscal outlook prompting a sharp rise in gilt yields, which led to large mark-to-market losses on the fixed-income portfolio of defined-benefit pension funds. This caused margin and collateral calls that pension and liability-driven investment funds had to meet through the sale of gilt securities, pushing gilt prices even lower. The Bank of England was forced to announce temporary and targeted purchases of long-dated gilts and index-linked gilts to stabilise prices. The goal of this intervention was to allow liability-driven investment funds to rebalance without amplifying the initial shock. This episodeshows that, even though pension funds and insurance companies are not really exposed to maturity transformation risks (like other NBFIs are), they are still at risk of being caught in a death spiral. Furthermore, other NBFIs would be exposed to the risk of investors withdrawing which would further amplify this risk.

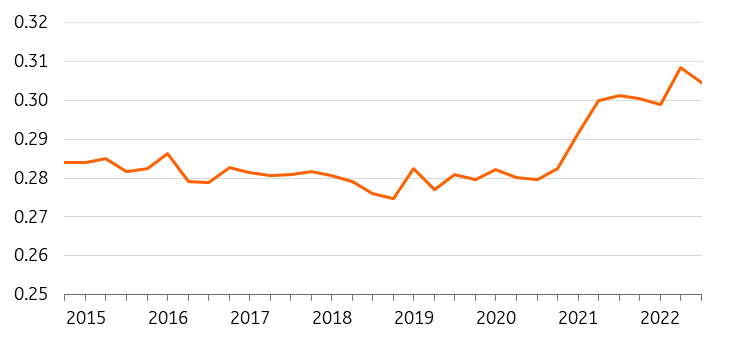

Additionally, exposure to a concentrated portfolio of assets combined with liquidity shocks can amplify stress events. For example, redemptions can force investment funds to sell assets, depressing prices and leading to further sales by other market participants with similar portfolio holdings, thus, amplifying the initial shock. Unfortunately, over the last two years, investment fund portfolios have become increasingly similar, increasing the threat of correlated liquidity shocks. This is even more important as NBFIs have also grown in size.

Increasing similarity in NBFI portfolios' asset class since 2020

IMF asset class similarity index reached 0.3 points in 2022

3. Interconnectedness

NBFIs have grown in importance since 2008, implying that their role has increased in both domestic and cross-border capital flows. They have also become more interconnected with the rest of the financial system which significantly increases the complexity of the sector. This could lead to growing vulnerabilities and risks and serve as a shock amplifier. The interconnectedness has not only increased between NBFIs and other financial institutions like banks but also between the different types of NBFIs.

OFIs' funding from banks dropped by 4 percentage points as percentage of total assets

Funding from pension funds remained stable and increased from other OFIs

Bank linkages to NBFIs have nonetheless been increasing over time which can be explained by the increasing size of the NBFI sector. With IMF data, we can see the increase in both claims and liabilities from banks to NBFIs.

NBFIs now make up about a fifth of banks' assets and liabilities

Banks' claims to NBFIs reached 22% of total cross border claims as liabilities are around 20% of total cross border liabilities

Bank liabilities towards NBFIs (as a percentage of total cross-border liabilities) have increased by five percentage points since 2015. The same pattern is visible for claims to NBFIs which went from 17% to 22% in the seven-year period.

Once again, the interconnectedness between the traditional banking industry and the NBFI sector greatly varies between countries. Data from the FSB allows us to investigate banks’ exposures and use of funding from different NBFIs in 2021 at a national level (for the 29 countries selected), showing significant differences.

Important variations in banks' use of funding from NBFIs as percentage of total bank assets in 2021

In Europe, Luxemburg is the front-runner with nearly 25% of its total bank assets funded by NBFIs

Important variation in banks' exposure to NBFIs as percentage of total bank assets in 2021

In the EU, Belgium is the most exposed to NBFIs, at 9% followed by the UK at nearly 7%

The importance of these three main risk categories also varies depending on the NBFI sub-sector. The following table from the IMF estimates the financial leverage, liquidity and interconnectedness risks for each NBFI sub-sector.

Investment funds are facing high vulnerability to liquidity and interconnectedness risks

As the largest sub-sector, investment funds high risk scores would imply a significant impact on the sector in the event of a major shock

Spillover risk to banks

The previous section looked at the most prominent risks for the NBFI sector. However, no data currently exists to make an estimation of the potential impact on banks if these institutions were to see significant stress events. Nonetheless, we can identify some direct and indirect channels through which stress on NBFIs would affect banks.

Direct impacts

Firstly, most banks rely on NBFIs for funding, as shown in the previous graphs. Stress in the sector might directly affect banks’ ability to fund themselves, possibly leading to a sudden shock in funding costs.

Secondly, banks have exposure to these NBFIs, which may lead to credit risk for banks. Some pain on the asset side, however, would not bring the typical NBFI down and the hit would mostly be taken by investors in the funds.

The Bank of International Settlements highlighted in the graph below, the different direct exposure that banks can have to NBFIs, and thus the potential direct impacts. It also makes clear the strong interconnectedness and resulting lack of transparency of both sectors.

Illustrative examples of assets and liabilities links between banks and NBFIs

Indirect impacts

Crucially, both the direct and indirect effects would add up as they would likely occur simultaneously. We see three indirect impacts that would occur in the event of intense stress on the NBFI sector.

1. Financial instability and asset value drop

As mentioned, shocks to NBFIs may lead to fire sales of assets, which could itself lead to turmoil in financial markets. Banks would also be affected via the drop in value of some of their assets.

Given the larger size of the NBFI sector, the effects will be stronger than in the past. This would hurt the value of the assets that banks use as collateral themselves (e.g. in liquidity operations with the central banks), thus hitting the ability of banks to fund themselves. Also, this would hit the collateral that banks require from customers. In the event that the resulting margin calls couldn't be met, this could lead to credit losses for banks and possibly result in doubts about the bank itself.

2. Wealth effects in the population

Shocks to NBFIs would induce a hit to the value of their investments. Most hedge fund investors and other financial intermediaries are considered to be high-income individuals, who would experience a negative wealth effect, leading them to spend less. Nevertheless, this would not have a big impact on the broader economy, as spending among high-wealth individuals actually has a limited relationship to their wealth. However, this is not the case for pension funds. One could expect a shock affecting many pension funds or one fund, in particular, (as we have seen in the UK) to affect the middle-income population. On top of being a huge confidence shock, this could potentially impact the solvency and default probability of a portion of banks’ middle-income customers. With a shock large enough, this could also imply less spending and a potentially significant slowdown of the broader economy.

3. Credit availability and costs, affecting the loan book

NBFIs play an important role in the economy by providing access to credit to those who cannot borrow at a reasonable cost through banks. An important stress could mean a contraction in credit and sudden higher financing costs in the real economy. This would slow the economy down and therefore also impact the banking sector.

Furthermore, the link between a client and an NBFI (such as an investment fund) is less strong than between a bank and its client. When the going gets tough, banks often support their clients. Investment funds may not have this same incentive. This may mean that banks will be looking at a situation where either they see their client defaulting (if the NBFIs do not extend their funding) or they are forced to refinance. These dynamics may pressure bank loan quality.

A financial shock that hits the NBFI sector could lead to financial stress in the banking system both via direct and indirect channels.

A banking crisis may also be worsened by the presence of NBFIs

We have looked at the effect of stress on the NBFI sector. However, if there is a stress in the banking sector, NBFIs may also exacerbate that stress, even if the are relatively safe themselves. During the banking crisis earlier this year, inflows to US money market funds were at an all-time high. Part of this has correlated with deposit outflows from US banks. In the unlikely, but not impossible, event of a flight from banks into money market funds, this could put banks under severe stress.

The largest 'known unknown'

As mentioned before, no data currently exists to allow us to make a clear assessment of the impact on banks if NBFIs were to see significant stress events. The difficulty stems from the lack of data on the sector. Indeed, even though the regulatory requirements vary between NBFI sub-sectors, there remains a general lack of regulation and data requirements. Without data giving a clear overview of NBFIs, one can only broadly estimate where the vulnerabilities stand: which are probably mostly in the US. We also know the vulnerabilities (leverage, liquidity and interconnectedness) as well as the direct and indirect channels through which the risk might propagate to the traditional banking sector. All in all, we see this as the largest "known unknown" risk for the financial system.

A long road ahead towards more regulation

Major financial institutions such as the IMF and FSB and central banks are clearly aware of the NBFIs' vulnerabilities and lack of transparency. They have emphasised the need for regulation of NBFI activities and suggest, for example, allowing certain NBFIs access to central bank liquidity in times of stress. Also, they see a strong need to bridge the current data gaps and incentivise NBFIs to apply stricter risk management. The ECB has also recently requested that banks put more effort into the regulation and monitoring of their NBFI counterparties, passing the ball back into the court of the banks. In any case, the implementation of such regulation in an international, growing, diverse and increasingly complex sector will take years.

The road ahead to a fully regulated industry is still very long. In the meantime, if the sector faces severe stress which spills over to banks, monetary authorities might be forced to step in. Central banks remain the backstop and could – possibly reluctantly – have to lower the risk of an all-out financial crisis stemming from the growth of the Non-Bank Financial Intermediaries.

The irony

So, if the going gets tough for Non-Bank Financial Intermediaries, the banking sector could be affected by the shock wave.

After a decade of bank regulation that curtailed banks’ risk profiles and lowered the vulnerability of the banking sector, financial risks in other parts of the system have grown, posing an indirect risk to the banking sector and a possible reason for central banks to step in. It's an ironic situation, both for banks that have seen this sector grow much faster than the banking sector itself, as well as for regulators who were hoping to have dealt with financial stability. In trying to minimise risk, the risk has been significantly compounded.

Annexes

FSB classification of narrow NBFI and respective share of global market (end of 2021)

List of countries included in the 21 + euro area group

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more