New Zealand: Migration poses risk to disinflation and rate cut prospects

The spike in net immigration in NZ does not have obvious implications for prices but recent data suggests the inflationary effect via the housing channel is outweighing the disinflationary relief to labour supply. This means, in our view, that the RBNZ will not deliver a clear dovish pivot in February, which is likely to benefit NZD beyond the near term

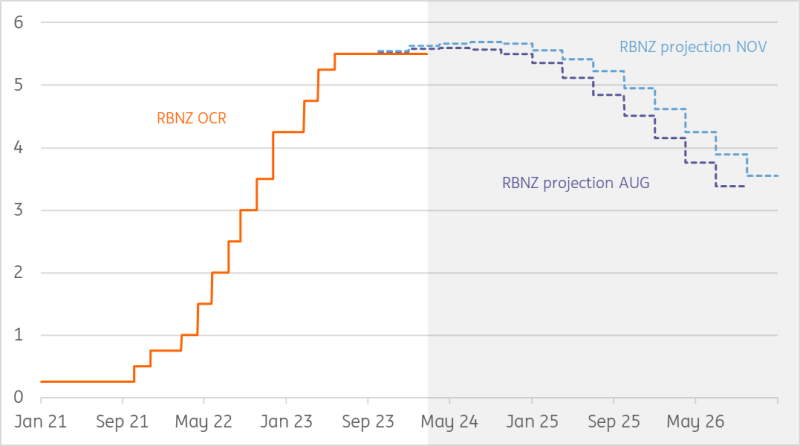

The Reserve Bank of New Zealand's announcement in November was a big hawkish surprise. Policymakers dismissed growing expectations for monetary easing and signalled that rates could be raised further. The November rate projections showed a 75% probability of another rate hike by 3Q24, and levels below the current 5.50% OCR only from mid-2025.

Since the November meeting, global developed central banks have increasingly opened the door to monetary easing, and New Zealand's headline inflation has decelerated faster (4.7%) than projected by the RBNZ (5.0%) in 4Q23. We think rate hikes in New Zealand are quite unlikely, but equally, pivoting to a dovish stance is not on the cards for the 28 February RBNZ meeting. The key reasons are the inflation outlook and the impact of booming migration.

The RBNZ retained a hawkish bias in November

Non-tradeable inflation warrants caution

The RBNZ differs from other developed central banks in that it announces policy less frequently - seven times a year versus eight from the Federal Reserve, European Central Bank and Reserve Bank of Australia – and has at its disposal quarterly, not monthly, inflation and jobs numbers. These two factors are often the cause for rapid changes in policy directions by the RBNZ, which normally relies on assumption-heavy projections. However, we don’t think there are the conditions for a policy shift already in February.

A new set of economic projections will be published at this meeting, and the fresh inflation outlook will be watched as much as the OCR rate path. Despite faster headline disinflation than forecast in November, non-tradeable CPI slowed less (1.1% quarter-on-quarter) than the RBNZ projected (0.9%). Inflation expectations declined from 2.76% to 2.50% in 1Q, as largely expected.

The resilience in non-tradeable inflation is a key concern for the RBNZ

The resilience in non-tradeable inflation is a key concern for the RBNZ, as it mirrors price pressures from a tight labour market and rising immigration. The 4Q23 jobs data was strong. Employment rose 2.4% year-on-year (RBNZ projections 2.0%) and the unemployment rate ticked only marginally higher to 4.0% (RBNZ projections 4.2%). Wage growth was lower than expected in the 4Q average hourly earnings report, falling to 6.9% YoY (RBNZ projections 7.2%), although still worryingly high.

Migration looks increasingly inflationary

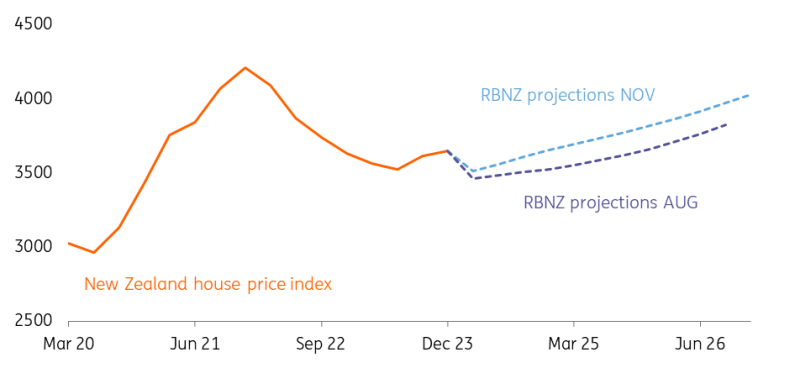

The theme of rising net immigration is another key subject. In August 2023, the RBNZ published a note to discuss the impact of migration on New Zealand's inflation. The results of the bank’s research were not conclusive: while net immigration helps relieve the labour market’s supply constraints, it is also proven to generate an inflationary impact on rents and house prices.

Net immigration is proven to generate inflationary pressure on housing and rents in New Zealand

The origin and age of migrants are very relevant: the largest share of post-pandemic arrivals in New Zealand are aged 30-49 and come primarily from India, China and the Philippines. Migrants from that age bracket tend to have a larger inflationary effect (mostly through the housing channel), although research shows that those arriving from those Asian countries generally have a less inflationary impact than migrants from advanced economies (like the UK and Australia, which dominated pre-Covid inflows).

In August, the RBNZ said, “our central forecast continues to incorporate a low but positive impact of net immigration on inflation”. In the November statement, they stressed that the spike in net immigration was a key contributor to the rebound in house prices and the faster-than-expected increase in rents.

As they meet in February, we believe policymakers will need to take into account that the fourth quarter jobs report pointed to only a modest impact on the labour supply from migration, thereby removing one key argument for the disinflationary impact of new migrants. All in all, we think data will continue to suggest the intense wave of arrivals into New Zealand has a more positive net impact on non-tradeable inflation than previously assumed.

New Zealand house prices are rebounding thanks to net immigration

A gradual pivot, cuts from August

As rates will almost surely be kept unchanged at the 28 February meeting, the RBNZ will use its OCR projections as the main communication tool. We think that the impact of migration and the implications for non-tradeable inflation highlighted above will preclude a substantial pivot to the dovish side. We must remember that since December 2023, the RBNZ’s remit only includes price stability, and no longer maximum employment.

OCR projections may signal the tightening bias remains on

February’s projections may show rates being reduced below the current 5.50% in early 2025 or even late 2024, versus the mid-2025 indication in the latest projections. But the front-end of the rate path may well continue to be projected above 5.50%, signalling the tightening bias remains on.

As discussed above, any new assumption on the inflationary effect of migration and the direction of non-tradeable inflation will be key to determining the extent to which the current monetary policy bias is a mere guidance instrument (i.e. keeping market rates supported) or effectively denotes a serious intent to maintain policy restrictive for a prolonged period of time. We currently forecast a further decline in headline inflation in the first quarter, but non-tradeable inflation looks likely to remain supported for longer.

Our baseline scenario is that the RBNZ will start cutting rates in August, delivering a total 75bp of easing this year. However, we admit there is an increasing risk that cuts will only start in October.

Market impact: NZD to have good carry for longer

We expect a neutral or modestly positive impact on the New Zealand dollar from the February RBNZ meeting. Expectations for rate cuts in New Zealand are contained (around 40bp in the next 12 months), and signalling cuts in late 2024 or early 2025 should keep those broadly unchanged. There are, however, upside risks for the currency as some investors may have positioned for a more decisive dovish shift.

The carry advantage remains the core driver of NZD strength

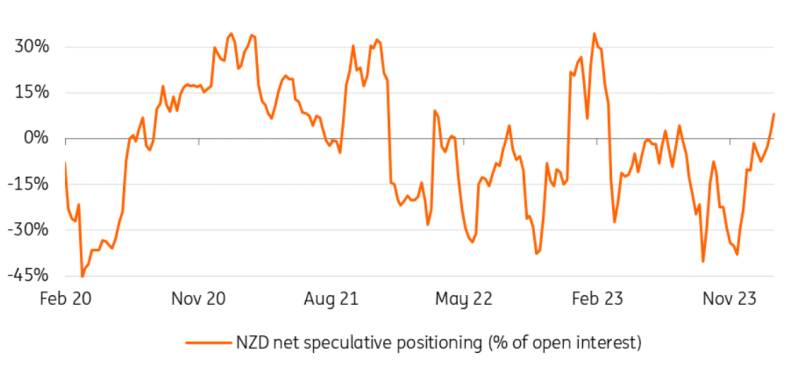

The Kiwi dollar has had a strong month of February, emerging as the best-performing G10 currency. The carry advantage remains, in our view, the core driver of NZD strength, and justifies the sharp rise in net long positions since November (chart below). NZD two-year swaps are trading close to 5.25%, approximately 75bp above USD and 120bp above AUD.

It is actually the positioning picture that may be slightly concerning in the short term. NZD is now an overbought currency according to speculative positioning data from CFTC, which raises the chances of investors favouring other – oversold – currencies like the Aussie dollar once the US dollar enters a stable declining path.

NZD has moved back into net-long territory

Our view that rate cuts in New Zealand won’t start before August, and that the Fed should instead start cutting during the summer translates into a bullish NZD/USD profile for the rest of the year. However, external volatility can offset the positives of a hawkish RBNZ in February and favour a near-term slide to more attractive levels for longer-term bullish positioning. We see NZD/USD breaking the 0.6500 mark in 3Q24. Some downside risks related to the US elections and potentially negative implications for China-related sentiment may warrant a less optimistic NZD profile in 4Q24.

Download

Download articleThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more