National Bank of Hungary Preview: Staying the course

- 17 July 2025

- Hungary

In our view, interest rates in Hungary are likely to remain unchanged for an extended period. Persistently high inflation expectations and ongoing global uncertainties continue to cast a shadow over the outlook and play a central role in the decision-making process

Our call

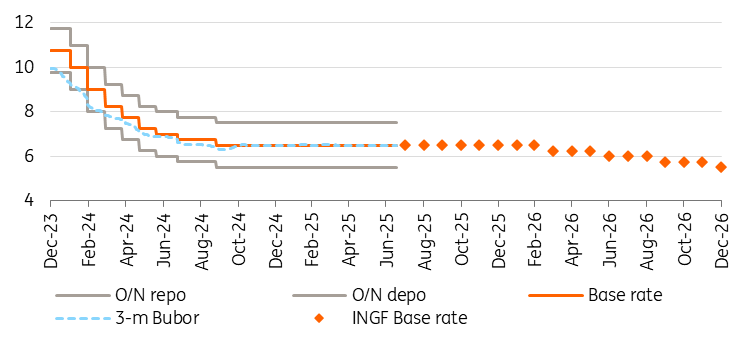

Taking everything into account, we still see no scope for the National Bank of Hungary (NBH) to ease monetary policy in the short term. In line with this view, the central bank is expected to leave interest rates unchanged at its next rate-setting meeting in July. The base rate will likely remain at 6.50%, with a +/- 100bp interest rate corridor - a high-conviction call.

Looking further ahead, we still expect no rate cuts this year, as the Monetary Council prioritises addressing elevated inflation expectations. Regarding 2026, we predict a total easing of 100 basis points. However, in all fairness, predicting next year's interest rate path in such a volatile environment is more akin to playing roulette than applying economic principles.

The main interest rates and ING's forecast (%)

Despite government interventions (which have shaved off approximately 1.0-1.5ppt), inflation has remained high. These measures have also proven ineffective in significantly lowering inflation expectations. However, the latest consumer price index was in line with the NBH’s forecast, therefore causing no surprises. Nevertheless, the Monetary Council is committed to fighting inflation. The current interventions will stay in place until August; however, they are likely to be extended, adding another layer of uncertainty to policymaking.

Our market views

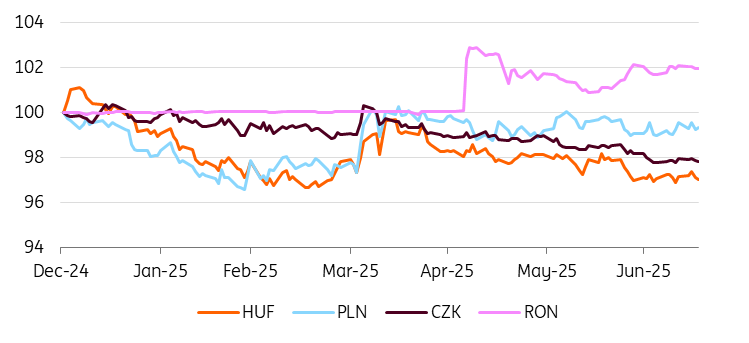

The forint saw a decent rally in June, and we have seen increasing long positioning in the market amid expectations of high carry and lower volatility during the summer. While there have been many market calls at 390-395 levels, we remain in a more neutral camp at current levels around 400 EUR/HUF. The market has priced out most of the rate cuts, and we don't see more support from this side in our view. Although we do not expect rate cuts this year, July should show weaker inflation numbers and economic surprises to the downside, which may lead to more dovish market pricing and again undermine HUF strength.

At the global level, the quick recovery of sentiment in Europe after "Liberation Day" supported the HUF's rally although for now, this seems like an exhausted story, and we cannot see more support here either. Thus, we don't expect much from current levels now and expect EUR/HUF to rise again to 410 by the end of the year amid more dovish market pricing.

CEE FX performance vs EUR (end-2024=100%)

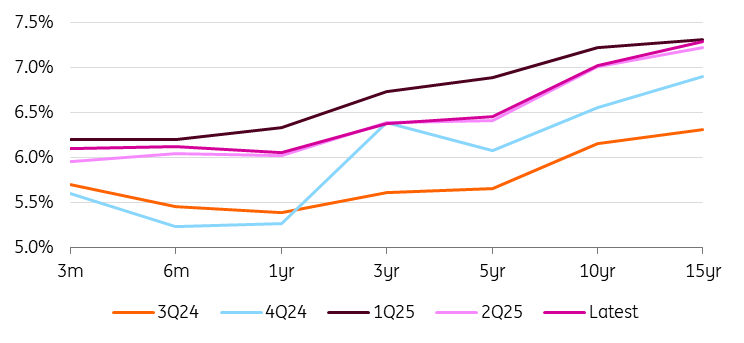

The rates market has calmed down compared to the big swings in the first half of the year, and the market remains range-bound in rather hawkish territory. The priced terminal rate is roughly 5.65% over a two-year horizon, slightly above our economists' forecast. At the same time, for this year, the market still expects almost one 25bp rate cut versus no cuts in our forecast. The front-end does not look very attractive at the moment and in our view, will remain anchored more on the upside given the hawkish NBH tone. But at the same time, the economy continues to surprise to the downside, which could raise the risk that the market will be more dovish on potential rate cuts next year.

Hungarian yield curve

More interesting is the long end of the curve, where the 5y5y is climbing back up currently around 7.30%, near this year's highs. The spread vs core rates has tightened here, suggesting pressure from core rates rather than higher market concerns about the inflation outlook. Although this story may continue, with our view of higher long-end core rates in coming months, further signs of a weaker economy or inflation may attract receivers to the belly and long end of the curve, given the attractive levels here.

The background

As expected, the NBH kept its key interest rate at 6.50% in June. The interest rate corridor remained in place, maintaining a range of +/-100bp around the base rate. In line with its stability-oriented approach, this decision was largely influenced by elevated inflation expectations and global uncertainties.

Since the last rate-setting meeting, US tariffs and further tariff threats have created additional pro-inflationary risks. Conversely, the ceasefire in the Middle East has improved global market sentiment; however, the forint has remained within a narrow range, glued at 400 to the euro. In this respect, the HUF has not been able to capitalise on rising risk appetite and, in our view, remains vulnerable to a sell-off induced by profit-taking if something goes wrong.

Headline inflation accelerated to 4.6% year-on-year in June, however, this was in line with the NBH’s forecast. Our forecast for 2025 as a whole is now at 4.6% for headline inflation, assuming the margin freezes end by the end of August. The current price curb measures are being discussed for extension, although there has been no official communication about this yet. If they were to be extended, this could lower inflation in the short term (shaving some tenths off this year's figure), but in the long term, we expect higher inflation as a trade-off, adding to our baseline forecast of 4.0% for next year. Moreover, these kinds of interventions could negatively affect household confidence by making them think that the situation is so bad that the government has to introduce so many measures. This could further worsen confidence, which has weakened for two consecutive months and dropped to an 18-month low.

In terms of risk perception from a monetary policy perspective, the budget deficit in June was the best June balance seen in the 21st century. However, this was due to dividend payments and a technical coincidence; therefore, the recent monthly surpluses could be somewhat misleading. We believe that the government's deficit target of 4.1% will only be achievable with considerable effort. This creates another reason for the central bank to remain cautious. As for external balances, there has been no deterioration to change the outlook, so this area of the economy at least remains a silver lining.

Last but not least, in support of our 'no change' call, the NBH's forward guidance has remained hawkish, focusing primarily on inflation. It emphasises the need for stability-oriented, cautious and patient monetary policy and therefore tight conditions. Consequently, the central bank is prepared to maintain interest rates at their current level for the foreseeable future.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more