National Bank of Hungary Preview: Look away if you’re hoping for a near-term rate cut

- 13 November 2025

- Hungary

The strengthening of the forint helps the central bank fight inflation, but there's still a long way to go. We don't see any room for a cut in the base rate yet. The messages will likely be as hawkish as possible so markets should be able to take advantage of the opportunity offered by the carry trade

Our call

Taking everything into account, we still can't see any clear-cut reason for the National Bank of Hungary (NBH) to ease monetary policy in November. In line with this view, we expect the central bank to leave the interest rate complex unchanged at its next meeting on 18 November. The base rate will remain at 6.50%, with a +/- 100bp interest rate corridor – a high-conviction call.

Looking further ahead, we still do not anticipate any interest rate cuts this year or in the first half of next year, given that the Monetary Council remains focused on addressing high inflation expectations. Furthermore, there are new developments which look to be pro-inflationary over the monetary policy horizon (new fiscal targets, extended price shield measures).

Therefore, we stand by our hawkish base case scenario. We expect the interest rate to remain at 6.50% throughout the first half of next year. Then, in the second half of 2026, a backloaded easing of a total of only 50bp will come into play rather than 100bp of easing which was anticipated earlier. The risks are balanced. On the one hand, a growing risk of a global dovish tilt among major and regional central banks would increase the relative room for an earlier (or stronger) easing. On the other hand, the pro-inflationary nature of the government measures and the possibility of sovereign credit downgrades pose hawkish risks.

Our market views

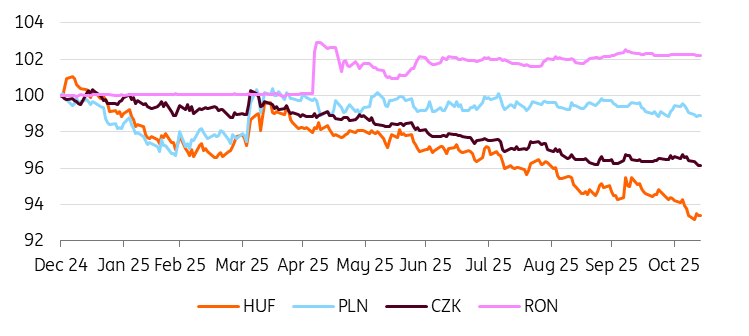

The forint continues to rally despite the sideways movement of other CEE currencies, supported by the hawkish tone of the central bank and high carry-to-vol. Still, it seems that long positioning isn't a significant problem and probably a large part is hidden in the options market. This week, EUR/HUF hit lows of just over 383 before correcting back to around 385 after news of a new deficit plan was announced for next year. The NBH meeting, combined with the announced “US financial shield,” could help stabilise FX markets following recent fiscal headlines, and a return to recent lows should not pose a challenge. This is supported by global factors such as EUR/USD rebounding from its lows, lower gas prices and the global risk-on mood coming from the equity market.

CEE FX performance vs EUR (end-2024 = 100%)

Overall, the positive sentiment in the HUF market may stay with us for a while. Still, this week's fiscal headlines cannot be ignored and investors will be paying even more attention to the bond market and rating reviews at the end of November (Moody's) and the beginning of December (Fitch), where some negative response to FX can be expected if we see action from the agencies.

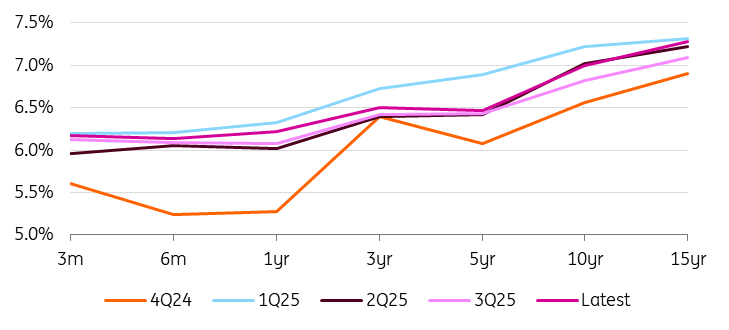

In the rates space, the first full rate cut is priced in for the April meeting next year and overall, the market sees less than three rate cuts with a terminal rate of 5.83% in the two-year horizon. Although we do not anticipate rate cuts in the near term, market pricing over a two-year horizon remains well above our forecast. That said, inflation is expected to ease, the economy continues to deliver downside surprises, and disinflation is supported by a stronger HUF.

The NBH remains hawkish, but there is likely little to add beyond the forward guidance provided in recent meetings. As a result, the risk now leans toward a dovish tilt if we see any indication of openness to rate cuts. While this is not our baseline scenario, the risk of earlier cuts is increasing given the state of the Hungarian economy and rate cuts elsewhere, such as in Poland and the US. Therefore we see scope for the short end of the curve to decline, while the long end should remain under pressure from fiscal headlines, likely resulting in further steepening.

Hungarian yield curve

In the bond space, the increase in the deficit for this year is unlikely to mean a significant change for Hungarian government bond issuance this year given the jumbo front-loading in October. However, for next year, the revision indicates issuance will be higher compared to initial expectations, while local demand may be the same or lower. On the other hand, valuations remain attractive, with HGBs trading above Romanian government bonds now, which should keep foreign investors interested. HGBs are likely pricing in most of the bad news at this point, but rating and political headlines may delay the recovery.

The background

As expected, the NBH kept its key interest rate at 6.50% in October. The interest rate corridor remained in place, maintaining a range of +/-100bp around the base rate. In line with its stability-oriented approach, this decision was largely influenced by elevated inflation expectations and pro-inflationary risks on the horizon.

Based on the October inflation prints, the current inflationary environment is still uncomfortably high, with out-of-range headline and core inflation figures despite the government’s mandatory and voluntary price shield measures. On that note, price shield measures were once again expanded, both regarding time (until end of February 2026) and the list (14 more food products were added). As we can see, there is a strong chance that there will be at least one additional three-month extension, which would mean that the measures would be lifted only after the general election. With this policy uncertainty looming in the monetary policy horizon, we anticipate that the central bank will maintain high interest rates for an extended period.

We have just witnessed the Hungarian economic policy’s Dr Jekyll and Mr Hide moment. While monetary policy is tight, the government has announced a relaxation of its fiscal targets, aiming for a stable deficit-to-GDP ratio of 5% rather than gradual tightening. It has also shifted from a zero primary balance target to roughly a 1% primary deficit. Since the National Bank of Hungary’s September Inflation Report was based on a 4.1–4.5% deficit in 2025 and 3.8–4.2% in 2026, these new targets imply a stronger fiscal impulse and greater pro-inflationary risk ahead.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more