National Bank of Hungary preview: Gradualism versus a stronger start

- 18 June

- FX Hungary

A rate cut in Hungary next week looks to be a done deal. Given the downside surprise in inflation and the de-escalation in geopolitics, everything appears to be in line for a 50bp cut. Still, we think the decision-makers will opt for the safest option of regular-sized easing

Our call

Compared to last month, the policy backdrop has turned clearly more dovish, giving the National Bank of Hungary (NBH) room to cut rates on 23 June. In light of last month's events, including the latest inflation data and communications from the central bank, we anticipate a 25bp reduction in the base rate, bringing it down to 6.00%.

We expect further rate cuts for the rest of the year, given the positive developments seen in recent months. Our current base case is a total of 75bp, but given the latest developments, we are leaning towards a total of 100bp easing overall.

Inflation outlook improves

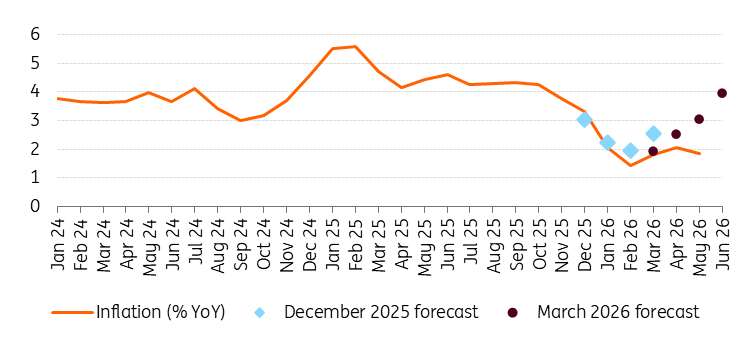

The latest inflation data surprised significantly to the downside, likely prompting a substantial downward revision of the NBH’s forecast from March. According to our calculations, inflation is likely to remain below 4% for the rest of the year, remaining within the central bank’s tolerance band all year. In contrast, three months ago, staff projections expected an above-5% peak in inflation this year.

Inflation in Hungary versus the NBH's projections

The new staff projection

The central bank is also going to update its staff projections. This revision of inflation should reflect lower realised inflation, a stronger forint and improving external conditions (e.g., geopolitics, energy prices). In turn, we see the 3.8% inflation forecast for 2026 revised significantly downward in the vicinity of 2.5%, while next year’s print can remain roughly unchanged (upward impacts from base effect, downward on improving general inflation pressures). We expect GDP forecasts of 2026-2027 (1.7% and 3.0%) to remain largely unchanged.

End of the war in Iran opens the door entirely

Improved geopolitical sentiment has reduced risks, with the forint at multi‑year highs and yields falling sharply. On the latter, the risk premium on German Bunds has dropped to the lowest decimal of historical spreads. Unsurprisingly, the market pricing now points to significant easing, with around 150bp of cuts expected this year and roughly 50bp cut over the next month. Furthermore, yields on retail government bonds have been lowered by 100bp over the past two months.

Some reasons for caution

Stronger domestic demand, supported by fiscal stimulus, real wage growth and improved sentiment, could fuel inflation over the monetary policy horizon. The not-so-remote possibility of rising oil prices, coupled with the imminent lifting of the fuel price cap and a more hawkish Federal Reserve, could also raise some concerns among members of the Monetary Council.

Communication matters

We expect that an interest rate cut will be announced at next Tuesday’s meeting. The question is how large the cut will be: 25bp or 50bp? As policymakers have not indicated a larger rate cut in their communication, we do not expect the NBH to surprise the markets without prior warning. Therefore, our base case scenario is a 25bp move. Consequently, the June decision is expected to favour gradualism over aggressive easing.

Argument for a bolder move

Given the improved inflation outlook and supportive market conditions, a 50bp cut could be justified without jeopardising stability. While a 25bp cut would likely cause the forint to strengthen further (since the market has already priced in more than that for next week's rate decision), a 50bp cut could limit the currency's appreciation. This could provide some relief for exporters, who have already complained about the pace of strengthening. It is in the economy’s interest to maintain stability while ensuring lower interest rates. In a rapidly changing world, market environments can also shift quickly; if this opportunity is not seized now, it may be gone in the future.

In our view, if decision-makers realise that the opportunity exists and are willing to make the move, there will be advance communication, despite the imminence of the monetary policy decision. They could do so without losing credibility, given that the recent geopolitical de-escalation has serious implications for monetary policy.

Our market views

The Hungarian forint has appreciated by around 6.2% versus the euro since the general election in April and recently hit 350 EUR/HUF, our mid-year target. The real effective exchange rate is reaching new highs and almost matches the historical highs from 2008. On the other hand, the forint still looks cheap in real terms compared to regional peers, suggesting that there may be room for further appreciation, which could be a problem for the economy sooner or later.

The combination of both the lowest inflation rate and the only central bank with inflation below target in the region, the market is pricing in an aggressive rate cut cycle of around 125bp for this year and a landing zone for the NBH somewhere around 4.75% next year. This does not seem stretched compared to 2024 pricing, and we expect the market to price in even more rate cuts from current levels once the central bank starts its cutting cycle. Given that long positioning is concentrated mainly at the long end of the curve, we expect further bull steepening in the short-term.

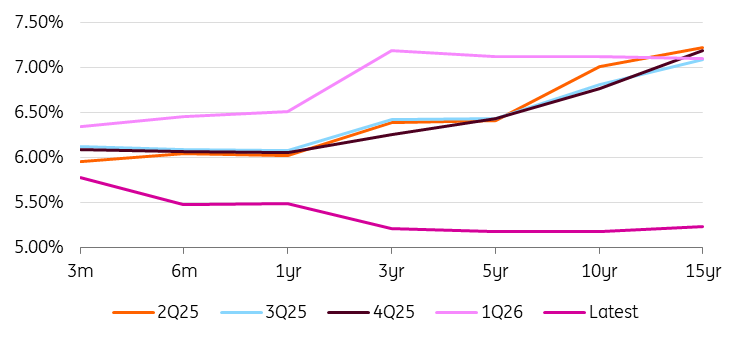

Hungarian yield curve

The implications for FX are not clear at this point. The typical reaction would be for the forint to weaken as soon as the central bank starts cutting rates. In this case, however, FX is driven by positive sentiment as well as the high demand for HUF assets triggered following the April general elections. Rate cuts do not necessarily mean FX weakening, especially in a situation where the market is already on the dovish side of pricing.

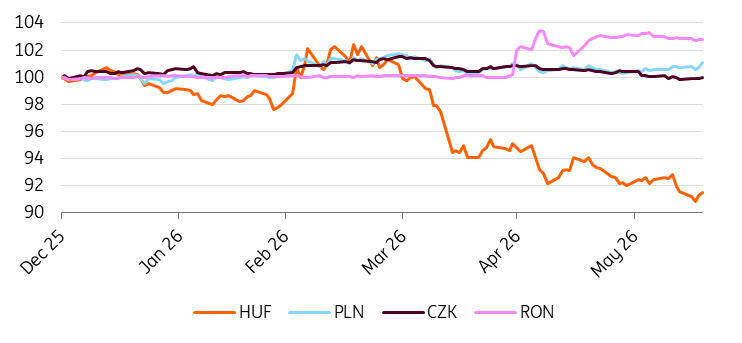

CEE FX performance vs EUR (end-2025 = 100%)

On the other hand, the outlook for FX carry here is deteriorating significantly, and that may reduce the forint's attractiveness. However, this should ultimately stabilise EUR/HUF rather than push it higher, and we should see compression in vol. Therefore, as a baseline, we expect that any upward correction in EUR/HUF could potentially attract new interest at higher levels. A stronger US dollar and NBH rate cuts may get us somewhere around 355 in the short term, where some resistance could emerge.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more