National Bank of Hungary Preview: Chances of rate cut grow, but patience needed

- 22 January

- Hungary

The National Bank of Hungary’s tone has changed, but the data hasn't supported its stance over the past month. We are getting closer to a rate cut, but circumstances suggest that there will be one more pause before it happens

Our call

We believe that the National Bank of Hungary is more likely to keep interest rates unchanged than to reduce them at its next meeting on 27 January. The base rate should remain at 6.50%, with a +/- 100bp interest rate corridor.

Looking further ahead, we believe there may be scope for monetary easing in the latter part of the first quarter when inflation is expected to fall significantly but temporarily. The outlook appears favourable for a rate cut in February and March (2x25bp), but the general election on 12 April will strongly influence what comes next.

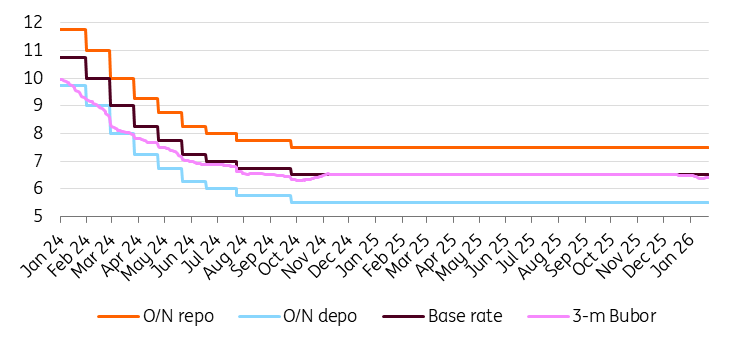

The main interest rates (%)

We don’t expect any changes regarding the communication and tone. The central bank will probably emphasise the upside surprise in the latest inflation figures and the fact that recent geopolitical uncertainty is currently an obstacle. However, the emphasis on a data‑driven stance and a month-by-month approach (i.e. that every meeting is a live meeting) will also remain in place, leaving the door open for a rate cut in February. If this is going to happen, we don't think that monetary easing will be a one-and-done move.

The tricky part comes with the general election and the related possibility of FX volatility, which could be too great for continued easing. In the event of a significant market response and a weaker forint, the central bank may opt for a pause, resuming easing only later in the year once the government and fiscal policy changes (if any) have settled.

The bottom line is that we see a total rate cut of 50bp in 1Q, with one or two additional 25bp cuts scheduled later in the year. The risks are balanced. On the one hand, a dovish tilt among major and regional central banks would increase the scope for stronger easing. Significant downside surprises in local inflation and further strengthening of the forint could prompt the NBH to consider an outsized cut in February or March.

On the other hand, the pro-inflationary nature of government measures is expected to become apparent soon. Also, growing geopolitical tensions could be seen as a risk to the expected cuts. To be fair, we still see a slim chance of a cut at the January meeting, should the Monetary Council decide that it is better to start earlier than risk missing the window due to further escalation in external developments.

Our market views

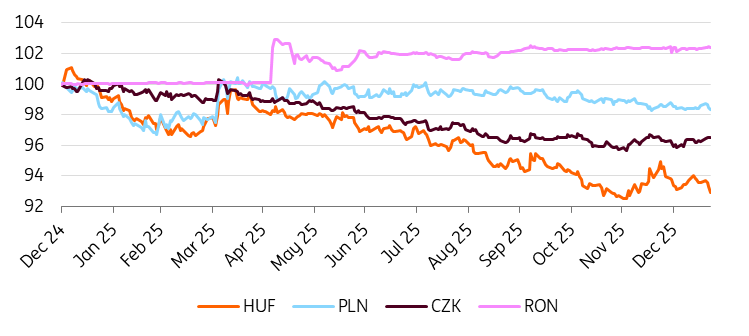

Although the Hungarian forint was under expected pressure after the NBH's dovish turn in December, we saw a very quick recovery. A weaker dollar and usually stronger CEE regional seasonality helped at the end of the year. And in January, higher than expected inflation and the market's return to carry trades helped as well. Overall, however, it seems that FX should not be an imminent problem for the NBH to restart the cutting cycle with EUR/HUF near recent lows. After the December inflation figure, the market moved the start date for rate cuts from January to February and is fully pricing in two 25bp rate cuts for the next four meetings, close to our expectations. Therefore, it would seem that the backdrop looks supportive for the NBH, and the forint should not see significant problems in the coming weeks.

CEE FX performance vs EUR (end-2024 = 100%)

In the longer term, the key is, of course, the outcome of the April general elections and how quickly and how far the NBH will want to cut rates. Putting the elections aside for now, given that the market has room to price in more rate cuts in the longer term, move the terminal rate lower and take into account the weak outlook for the Hungarian economy, the forint should see more downward pressure overall. Positioning remains long carry and the start of rate cuts could prompt investors to start unwinding these positions. Together with global uncertainty which could bring momentum in both directions for the forint, we expect levels around 385 EUR/HUF in our forecast.

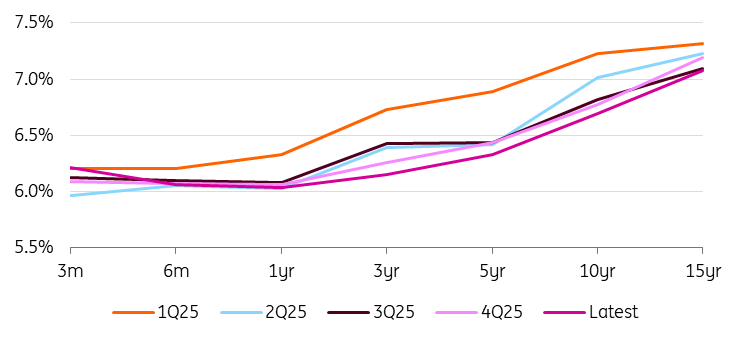

Hungarian yield curve

On the rates side, the story seems much simpler. Although very front end pricing is close to our forecast, we still see a fair amount of room for the IRS curve to price in a lower rates path over the year. The priced terminal rate is steadily above 5.50% and we expect the entire curve to move lower if the NBH starts rate cuts as we expect. The front of the curve clearly has the most potential and we should see the curve steepen further.

The background

As expected, the NBH maintained its key interest rate at 6.50% in December. The interest rate corridor remained in place, maintaining a range of +/- 100bp around the base rate. In line with its stability-oriented approach, this decision was largely influenced by elevated inflation expectations and pro-inflationary risks. However, the tone had changed. The NBH began to communicate that decision-making had shifted to a data-driven mode and that market pricing will be taken into account, too.

The December inflation data painted a mixed picture. On the one hand, the headline inflation figure fell within the central bank's target range, which is positive. However, a closer look at the details reveals that the month-on-month service inflation rate was much higher than expected at 0.8%. Furthermore, underlying structural inflationary issues are being obscured by base effects and the government’s mandatory and voluntary price shield measures. The latest decree states that the price shields will end at the end of February 2026. However, there is a strong chance that they will be extended until the elections.

The Hungarian government is set to introduce an additional utility price cap in January, which will cover the cost of increased household heating consumption during the cold spell. This will provide significant relief for headline inflation, which would have been greatly affected by rising household energy costs.

In addition, on 12 January, NBH Governor Mihály Varga stated that the NBH would prioritise the December inflation data, particularly service inflation, in its upcoming decision. Based on this, a rate cut in January is a wild card and would catch markets somewhat off guard.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more