NAFTA: What now for the “worst trade deal ever”?

- 24 October 2017

- Canada United States

Donald Trump seems set on ripping up NAFTA, but what does he want and what is he likely to achieve?

The NAFTA battleground

Throughout his Presidential election campaign, Donald Trump railed against free trade with NAFTA (North American Free Trade Agreement) the focus of his ire. Trump threatened to rip up the 24 year deal between the US, Canada and Mexico, calling it the “worst trade deal ever”. In his view it has cost jobs – US Trade Representative Robert Lighthizer “certified” that “at least 700,000 Americans have lost their jobs due to changing trade flows from NAFTA” – and contributed to the ballooning US trade deficit. Consequently, Trump wants things to change, but as we have seen with Obamacare and taxes, this isn’t always easily done.

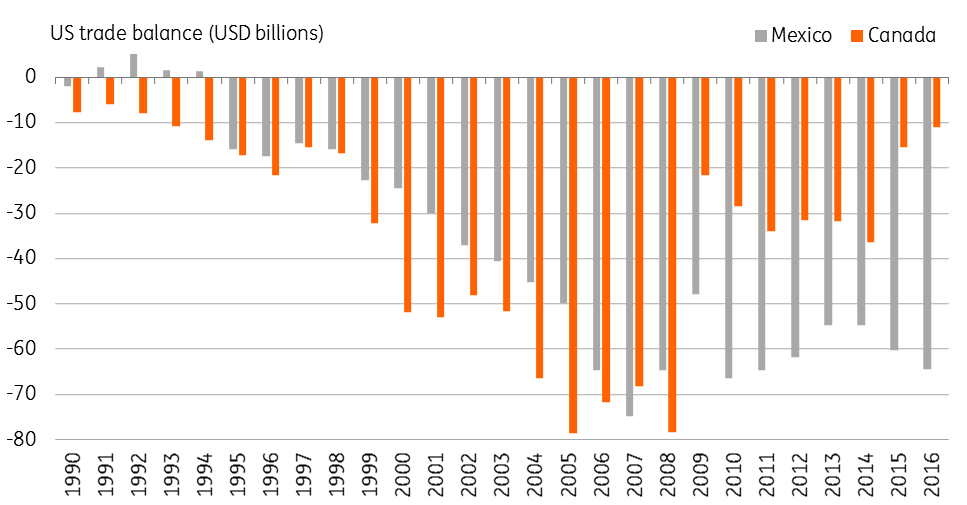

How the US trade balance has changed under NAFTA

What has NAFTA achieved?

NAFTA was intended to remove barriers to trade, increase cross-border business activity and investment, and increase choice for consumers while making North America more competitive on the international stage. Most economists would say it has achieved these aims with NAFTA now accounting for 25% of world trade with millions of jobs in the three nations dependent on that trade.

However, as with all deals, there are going to be winners and losers with critics arguing that American workers have been displaced by a cheaper Mexican workforce with businesses exploiting this for their own gain. At the same time, competition from Canada is perceived to have cost US jobs too. Consequently, “cheap” imports have been substituted for expensive American products and the US trade balance has worsened.

Technological advances are a far bigger threat to manufacturing jobs than NAFTA

The obvious response to this is that technological advances are a far greater threat to manufacturing jobs than NAFTA. For example, President Trump heralded Ford’s decision to reverse a plan to put a car plant in Mexico and instead invest US$1.2bn in Michigan. Yet such a vast sum of money only created 130 new jobs. Indeed, General Motors now employs 225,000 workers, around a third of the number it employed 40 years ago, yet it produces significantly more vehicles each year.

As for the trade argument, national accounting identities show that the only way the US can experience a meaningful narrowing in the current account is through higher national saving (household, business and government) or lower investment. With Trump looking to cut taxes and potentially invest in infrastructure (and Mexican wall building) this seems unlikely to be achieved.

Moreover, Trump has likened running a trade deficit to a company that is constantly leaking cash, implying it is bad for an economy to keep running such deficits. However, economists only have to cite Japan, which has run consistent trade surpluses and gone through several recessions versus Australia, which has had 25 years of deficits but experienced solid growth throughout.

Trump doesn’t buy it

President Trump doesn’t accept these arguments so his threat to pull out of NAFTA has led to negotiations on reworking the deal with US officials proposing a number of changes. A key proposal includes a five-year “sunset” clause in which the NAFTA contract would have to be re-approved every five years, meaning regular bouts of uncertainty over trade. Then there are proposals on government procurement and the dispute resolution mechanism, which would benefit the US.

US officials then want to see the rules of origin changed so that to benefit from the NAFTA deal North American-made content must exceed 85% for autos by 2020, up from 62.5% currently. They are then suggesting they want new National Minimum Content Rules, meaning a guarantee that 50% must be made in the US to qualify. However, with the US charging just 2.5% tariffs on car imports from outside NAFTA many firms may ignore the rule and instead just pay the tax to avoid supply chain disruptions.

| 62.5% |

North American content requirement for autos |

Will Trump get what he wants?

Canada and Mexico had seen little need to re-open talks and disparaging comments about Mexicans from President Trump and arguments over the border wall have not helped with regard to goodwill in the talks. Indeed, the Mexican presidential election next July intensifies the risk that anti-US sentiment could build, making the Mexican position more steadfast.

At the same time, free-trade supporting Republicans have lobbied the Trump Administration, with several hinting that if free trade is damaged Trump may not get the support he wants and needs for tax reforms. Business is also lobbying hard for politicians to oppose major changes while farming communities in states that backed Trump at the last election are also nervous about the implication for their exports should talks break down.

That said, having failed on healthcare and making little progress (so far) on tax reforms, it is a question of third time lucky for Trump. This could suggest that he will be even more focused on getting what he wants in NAFTA negotiations.

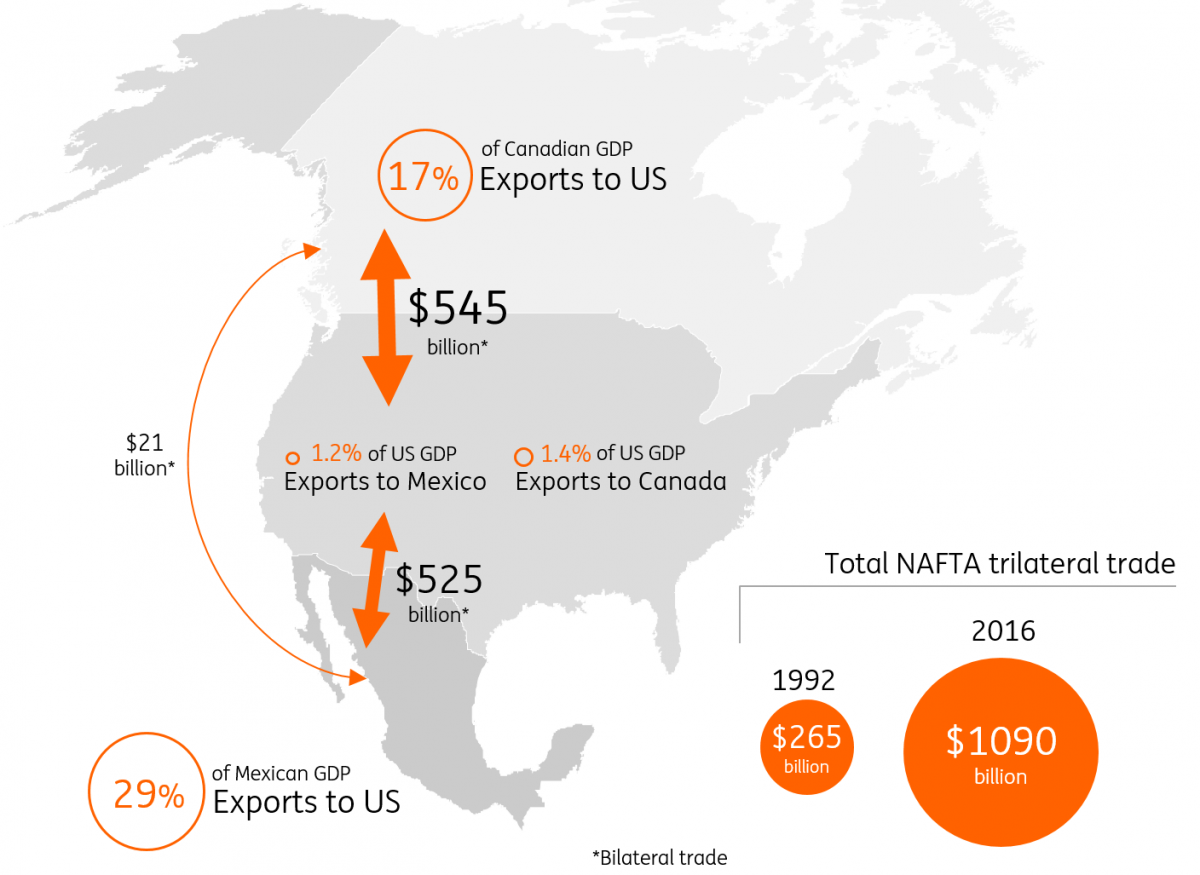

President Trump knows the US can walk away from NAFTA with relatively little impact on the economy. US exports to Mexico represented 1.2% of US GDP in 2016 and exports to Canada equated to 1.4% of US GDP. However, Mexican exports to the US were equivalent to 29% of Mexican GDP and Canada’s exports to the US were 17% of Canada’s GDP in 2016. Therefore national pride may end up giving way to economic pragmatism, providing Canada and Mexico with the incentive to “give some candy” in the negotiations as demanded by current US Trade Representative, Robert Lighthizer.

So while the end game of Mexico and Canada reluctantly agreeing to a watered down version of Trump’s original demands seems the most likely outcome, Trump’s reluctance to compromise suggest that this is not a forgone conclusion.

NAFTA trade in numbers

What happens if the US does pull out of NAFTA?

The fifth round of talks is scheduled for 17-21 November in Mexico with negotiations set to be brought to a final conclusion in 1Q 2018. If there is no agreement by that point Trump could announce plans to withdraw from NAFTA. However, there is some uncertainty over whether Trump has the legal authority to pull out of the agreement without Congressional support should he fail to get his way given that Congress ratified the original deal. If he proceeds, there is a six month notice period which could yet see last-minute concessions given from Mexico and Canada.

If NAFTA does end then the implications for Mexico are far worse than they are for the US or Canada. US-Canada trade may well revert to the 1988 Canada-US Free Trade Agreement, which would preserve tariff-free trade, but there still would be implications in terms of rules of origin and minimum content for products to qualify.

If NAFTA ends, the implications for Mexico are far worse than for the US or Canada

For Mexico, trade with the US and Canada would likely revert to World Trade Organisation Rules (if you download the US schedule from the WTO website you will find there are 192,275 lines of different tariffs). Luis Videgaray, the Mexican Foreign Minister (and former Finance Minister) suggested that such an outcome could actually lead to a deterioration in the US trade position with Mexico as tariffs on US exports to Mexico (7.1% on average) would be substantially higher than for Mexico (3.5%) and Canada (4.2%) to the US under WTO schedules.

This doesn’t alter the fact that Mexico is far more vulnerable economically to trade disruption given exports to the US are equivalent to a third of all economic output. We also have to remember that Trump could escalate the situation and impose extra tariffs such as the 20% levy on Mexican imports he has proposed to “pay for the wall”.

The key outcome is that businesses in all three economies would experience higher costs and disrupted supply chains and consumers would be faced with higher prices, particularly for cars, clothing food/agriculture and medical devices. The auto sector is particularly vulnerable given the complex supply chains and the fact that US imports of cars and car parts from Mexico are larger than the overall US-Mexican trade balance.

Canada and Mexico could choose to continue with NAFTA, but Canada-Mexico trade is actually a small overall part of total NAFTA trade at US$20bn – less than 2% of the total NAFTA trade. However, with Europe having signed the Comprehensive Economic and Trade Agreement (CETA) with Canada, and Mexico looking to improve on the 20-year-old deal currently in place with the EU, some US trade could be substituted for European. We also have to remember that Mexico and Canada are still in negotiations to join the Trans-Pacific Partnership which would remove tariffs from trade with key Asian economies.

| 192k |

Number of individual tariffs in US WTO schedule |

What would markets do?

President Trump is sanguine about the implications of pulling out of NAFTA while Robert Lighthizer suggested that all three countries will be “just fine” if it happens. However, markets are unlikely to be as relaxed with stock prices of impacted companies coming under pressure. The Federal Reserve may be modestly concerned about some short-term disruptive economic effects, but the mild hit to US economic activity will be offset by potentially higher inflation and we doubt monetary policy will be majorly impacted.

Markets are unlikely to be as relaxed

However, it will be a very different story elsewhere. The Bank of Canada has hiked interest rates twice this year with markets pricing in more tightening next year – we currently expect two further 25bp rate rises. We would remove one from our forecast due to concerns over the uncertainty it creates and the impact to economic activity. But the weaker Canadian dollar and higher imported inflation would provide a partial offset in the BoC’s thinking.

The reaction in Mexico would be greatest. Reduced export-oriented investment into Mexico, disruption in some manufacturing supply chains and higher trade deficits would likely trigger a selloff in both FX and local debt markets. Rating agencies are likely to react as well, possibly implementing a one-notch downgrade.

Market concerns would be compounded if the NAFTA disagreement helps left-wing candidate Andres Manuel Lopez Obrador win next year’s Presidential election and he proceeds with a major change in economic direction. Such an environment could see USD/MXN return to the 20-21 range in the first half of 2018. We don’t expect the currency to overshoot to the near-22 high seen in January.

The weaker peso should give the central bank, Banxico, no choice but to sound relatively hawkish throughout this period. The official rhetoric should display a willingness to act by raising rates if needed, but we don’t expect the bank to hike. At 7%, the carry should be sufficient to stabilise the peso, after the (justified) correction the currency should suffer. At most, we would expect Banxico to resume the FX-NDF swaps interventions the bank did once, closely following Brazil’s BACEN (central bank) playbook. As in the case of Brazil, these interventions should not change the magnitude/direction of the currency adjustment, rather they should just moderate the speed of that adjustment.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more