Mood in Czech industry turns gloomy

Both business and consumer sentiment dropped in April. Industry continues to grapple with weak demand and stagnant investment, as consumers remain cautious about growth prospects. Still, spending momentum persists, and the construction boom is set to support the rebound. The Czech National Bank will weigh risks to growth amid potent core inflation

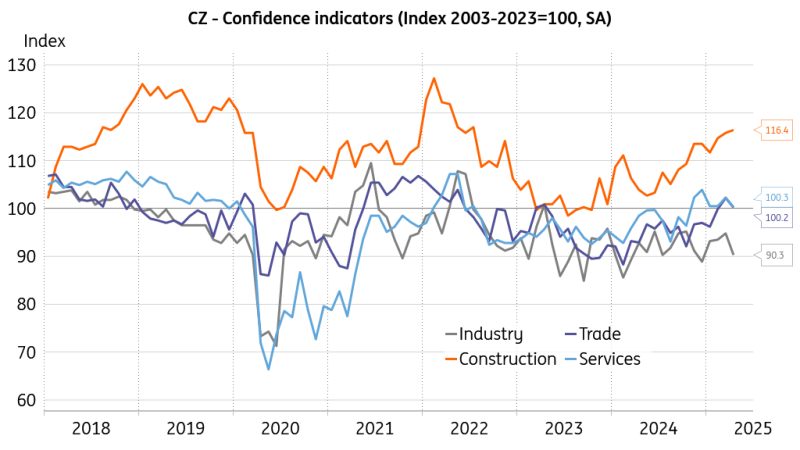

Industrial confidence slides while sentiment in construction improves

The consumer confidence indicator dropped by 1.1 points to 97.7 in April, while business confidence shed 3.1 points to 96.5 - the weakest level since last October. The aggregate confidence indicator deteriorated by 2.8 points to 96.7, well below the long-term average of 100. All the leading sentiment indicators came in weaker than market participants had foreseen.

Business confidence in April dropped 4.5 points in industry and 2.0 points in both the trade and service sectors. Industrial entrepreneurs are still struggling predominantly with insufficient demand, which was cited as a barrier to production growth by almost 44% of respondents in April. In contrast, the mood improved further in the construction sector by 0.6 points, reaching an upbeat 116.4. Czech households channel their resources and savings into property purchases, driving robust demand for new mortgages and pushing residential property prices higher.

Industry and construction take different paths

The share of consumers expecting the economic situation in Czechia to worsen over the next year increased in April. The share of households expecting their financial situation to worsen over the same period also rose. Meanwhile, the number of households rating their current financial situation worse than in the previous year remained unchanged, and the number of respondents not planning large purchases dropped for a second consecutive month. The consumer mood oscillates just below its long-term average, while the main worry is a possible deterioration in the economic outlook, coupled with stronger concerns about price hikes.

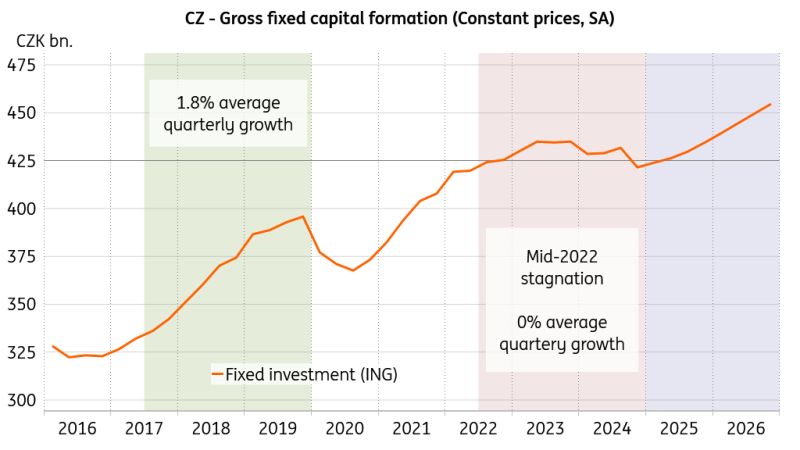

Appetite for investment falters while consumer spending takes the spotlight

The Czech National Bank will face a dual challenge, as core inflation is set to remain potent over the coming months, while the economic rebound faces some headwinds linked to global uncertainties. We see some space for further rate reductions to help the Czech economy return to its potential, especially as the appetite for investment is increasingly sluggish amid the ongoing tariff negotiations and undermined conviction about global economic performance. Everyone knows that investment is key to future economic expansion and prosperity, so it is essential to cultivate an environment that fosters an appetite for investment and not an appetite for destruction.

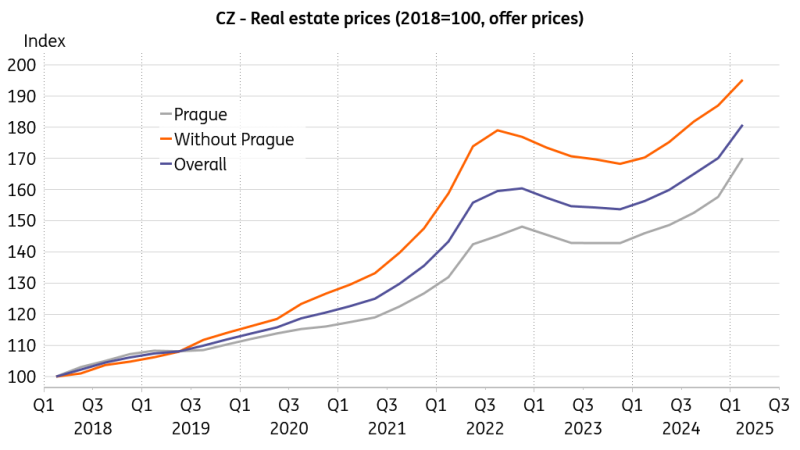

Property prices accelerate

In contrast, the consumer remains sanguine, and the booming residential sector may add fuel to core inflation in the foreseeable future. Offer prices of flats rose 15.6% from the previous year in the first quarter, while quarterly growth increased to 6.3%, more than double the previous year's final quarter. Such a strong rate will enter into the imputed rents, which are included in core inflation and make up 10.3% of the overall consumer basket. So, the timing of possible rate cuts will come down to the upcoming inflation figures, with the April preliminary estimate available a day before the board meets.

Stagnant investment is terrible news for the growth outlook

We foresee a slowdown in overall inflation in April due to a favourable base effect in the food segment, yet with a pickup in core inflation. In our view, a 25bp cut is the right way forward to set the environment for investment to find solid ground. However, given the recent communication of some board members, further easing in May is not a sure thing. The new forecast will also enter into policymakers’ decision-making. That said, the coming CNB forecast will be prepared under fresh supervision, as no stone was left unturned in terms of the recent changes in employment in the forecasting section. We are curious about how the Spring forecast will perform in terms of consistency and storytelling.

Every crisis creates an opportunity

The recent tariff upheaval and most abrupt reshaping of the global trade landscape in decades hit sentiment in industry across Europe in April. Meanwhile, every reshuffle creates opportunities, and we see quite some appetite from large Czech companies to invest in Europe. According to anecdotal evidence, the current situation is perceived as an opportunity to acquire shares in German firms while the economy faces severe structural issues. These growth hurdles are embedded in the German economic environment, which has little propensity for tangible reform.

Industrial confidence comes under pressure

Indeed, we see this growth mindset of the large Czech firms as the right move under the assumption that Germany will be able to find a new growth model in the foreseeable future. It is key for Czech manufacturing that the recent hype about European competitiveness and the appetite to succeed economically are not left in the realm of proclamations and quietly forgotten about, to simply gather dust in libraries, but are translated into reality sooner rather than later. If progress towards creating the right conditions for European firms to invest and grow remains sluggish, the Czech industrial sector risks fading into irrelevance. As Matthew Henry wisely noted, hope for the best but prepare for the worst. Please let me know if you have any insights on how to master this delicate balancing act.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article