The UK’s new prime minister faces immediate test as recession looms

With inflation set to hit 16-17% in January, a UK recession looks inevitable. The depth depends heavily on how much support the new prime minister offers to households and small businesses when he or she takes office next week.

Energy bills set to increase six-fold based on latest price data

The UK, like the eurozone, looks like it’s headed for a recession. The UK may benefit from greater security of gas supply and larger LNG regasification facilities. But a lack of gas storage means that Britain is vulnerable to price volatility across Europe this winter.

Indeed if wholesale gas prices were to settle at their most recent peak, we could see the average household energy bill hit almost £7,000 on an annualised basis next April. That compares to roughly £1,100 in previous years, and our latest forecasts suggest that inflation could hit 16-17% in January next year – or perhaps even higher.

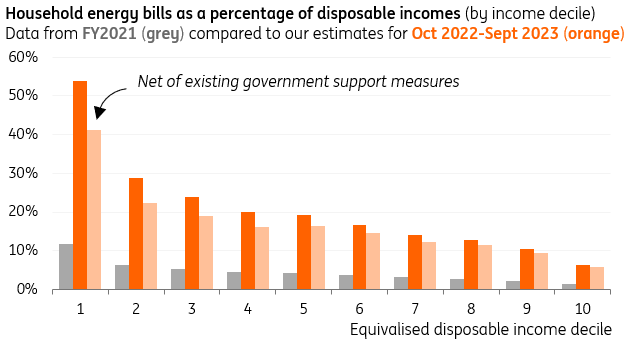

Unmitigated, that would see most households paying more than 10% of their disposable income on energy, something that could amount to material cuts in non-essential spending. The government has announced £37bn worth of support so far, but that was when energy bills were expected to peak at around £3,000. Households will need to find an extra £65bn to pay for energy bills from October to the same period next year, to offset the further rise in gas prices we’ve seen since the last round of support was announced.

Households in most income deciles set to pay more than 10% of disposable incomes on energy

This gives a sense of what the new prime minister, who will be announced on 5 September, will face. Foreign Secretary, Liz Truss, who is odds-on to succeed Boris Johnson, has stated a preference for using tax cuts to help households. However, the sheer scale of the energy bills that are likely to hit next year suggests that this will need to be coupled (or replaced) with additional direct payments to households across the income spectrum.

The most obvious mechanism for that would be to dramatically increase the existing £400 discount on energy bills that households receive from October. Importantly that will probably need to be extended, in one form or another, to small businesses, which are unprotected by the regulator’s price cap and are already experiencing potentially-existential price hikes.

Savings stockpile and tight jobs market could insulate economy if government support is ramped up

The key message is that the UK is heading for a recession, though its magnitude depends heavily on the scale of government support. In our base case, we’re assuming that support is materially increased and the scale of the economic downturn can be kept relatively shallow, at least by recent historical standards.

Remember that households still have ‘excess savings’ accrued during subsequent lockdowns, which amount to roughly 8% of GDP – albeit these are heavily skewed towards higher earners. For the time being, the jobs market is also very solid and remains characterised by ultra-low redundancy levels and staff shortages, though higher energy bills for corporates could begin to change that picture. Vacancy levels have begun to decline.

We’re pencilling in a hit to GDP of roughly 1%, though this is highly conditional on how much government support is offered.

Markets are assuming that a large government support package would raise the chances of a forceful reaction from the Bank of England. We agree with this assessment even if current swap rates wildly overestimate the scale of tightening that’s likely. We expect at least one, if not two, further 50bp rate hikes.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

1 September 2022

ING Monthly September: Recession’s coat of many colours This bundle contains 14 Articles