Pain from ECB hikes is set to shift south

The impact of the ECB's aggressive hiking cycle has been taken well by southern countries within the eurozone, but rapidly declining borrowing indicates that this is set to turn. We expect the impact of ECB tightening to have a larger impact on southern than northern eurozone countries in 2024

In 2023, southern eurozone countries defied the impact of monetary policy tightening

While expectations initially were that southern European countries would face significant problems if the European Central Bank (ECB) raised rates aggressively, this has not materialised so far. In fact, it rather seems to be the other way around – several indicators point to a stronger transmission of tighter monetary policy on northern and not southern European countries.

Take the stock market for example, where performances in northern European main indices have been weaker than in southern Europe. Also, price developments in the housing market point to a larger impact in northern Europe. Germany, the Netherlands and France have seen house prices fall below their recent highs, while Italy, Spain, Portugal and Greece still experience increasing house prices according to the latest available data. Turning to investments, the surge seen in southern European countries is remarkable. Admittedly, there is more to investments than only interest rates; think of the impact of the Recovery and Resilience Fund and some of the delayed impact of low interest rates, as well as the search for yield and successful structural reforms.

Differences in transmission are starting to show

The pain of monetary tightening is likely to be felt more in 2024 than 2023 due to the long and variable lags of monetary policy transmission. It just takes a while before the impact of tightening really impacts the economy. There is increasing evidence that the transmission of monetary policy in 2024 will be less favourable for southern European economies.

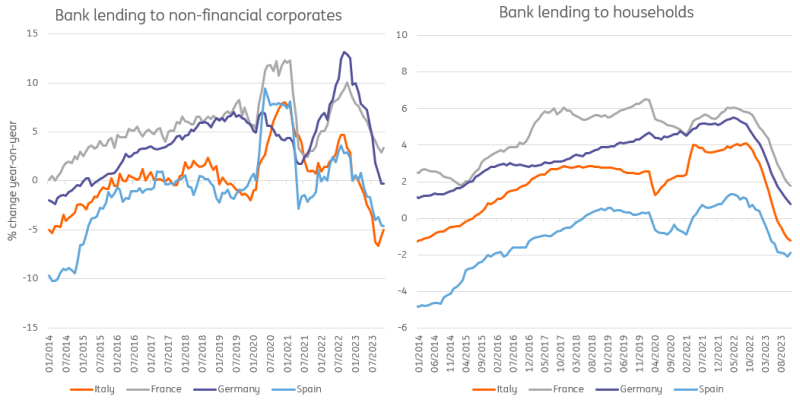

Take the most recent lending data. Lending volumes are currently falling in most southern European economies. In Italy, it's looking really rather serious as the 6% year-on-year fall of borrowing by non-financial corporates is worse than during the Global Financial and euro crises. Spain, Portugal and Italy see declining borrowing volumes for both households and corporates, while northern European economies are still seeing year-on-year growth in borrowing.

Bank lending is diverging quickly, likely resulting in weaker investment in the periphery

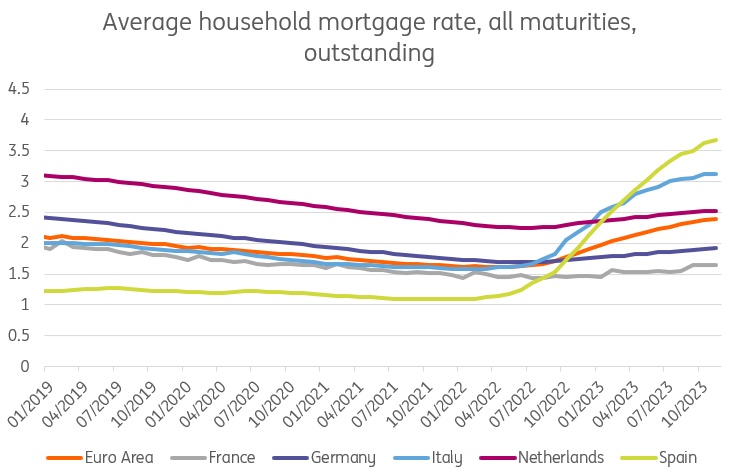

But the impact of higher interest rates is not only seen in new loans and new investments. It also impacts the economy through increasing interest rate payments. Average mortgage rates have gone up more in southern Europe as variable interest rates on mortgages are more common. The impact of higher mortgage burdens could play out through adjustments in the housing market and weakened consumption, as they reduce the opportunity for disposable spending elsewhere. And there is another transmission channel through which higher mortgage rates will affect economies: redemptions on mortgage loans have increased markedly in Italy and Spain since higher rates have kicked in. This essentially means that higher rates have kicked off a process of household deleveraging in the south, which will weigh on consumption and economic activity.

Average mortgage rates have risen far faster in southern eurozone markets

When looking at net interest rate payments for corporates, we see that German and Dutch companies have barely seen any impact so far. This could also be because they hold more cash reserves, which have started to generate positive interest flows. In Spain, Italy and France, net interest payments have risen to the highest level in more than seven years.

For governments, interest rate payments are also starting to increase, but again much more in the South than the North. While most countries have lengthened the average maturity on their debt, higher rates are starting to result in higher interest payments. We note that the increase has been fastest in Italy, where net interest rate payments have returned to 2015 levels. Overall, expect the gap to widen as more debt gets rolled over. This will cause discussions about austerity to become more pressing. Then again, at this point it is clearly Germany that leads the way in terms of belt-tightening, so we don’t see austerity efforts moving along the traditional North-South lines in 2024.

This year, the impact of tightening on the periphery looks worse than for the North

Even if ECB rates have peaked, and we might even see rate cuts later this year, 2024 will still be one where the full impact of monetary policy tightening of the last 18 months will unfold. While southern eurozone countries surprisingly seemed to defy the adverse impact of monetary policy tightening last year, we fear we'll not see something similar in 2024.

Download

Download article

8 February 2024

ING Monthly: Reasons to be cheerful, Part 3 This bundle contains {bundle_entries}{/bundle_entries} articlesThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more