Rates: Are we there yet? Nope

- 4 February 2022

- Rates

When kids ask that question, they already know the answer. It's a journey for market rates, and we're still on it. Even if macro oomph is met by demand for bonds, there are looming liquidity reductions ahead. These can tip the balance, as can actual rate hikes, not to mention the threat of central bank bond selling

We've already hit some milestones with market rates, yet the Fed has not even started to tighten

It’s been quite a start to the year for rates, with some key levels hit. For example, the US 10yr touched 1.9%, its highest since the pandemic began. The Euro 10yr swap rate is almost at 60bp now, compared with negative territory for most of 2021. And the 10yr German yield has broken above zero for the first time since mid-2019 and approaching 15bp. There are stories behind all of these moves, but the common theme is one of a pronounced macro reflation, and a nod from central banks that this has their undivided attention.

The US Federal Reserve in particular has increasingly acknowledged that supply-induced price hikes have indeed morphed into an inflationary process. And it is telegraphing an intention to calm that process through monetary tightening. Yet, so far the Fed has done nothing apart from talk. It has tapered its bond purchases, but it is actually still buying bonds, still expanding its balance sheet. And its first rate hike is not till March. It’s all talk. The walk lies ahead.

Meanwhile, both the ECB and Bank of England have ramped up the interest rate risk too, and markets are keen to price in steeper money curves. Central banks are on a mission to catch up with the inflation genie that was unleashed in 2021, and left untamed till now for good reason – recovery from the pandemic took precedent.

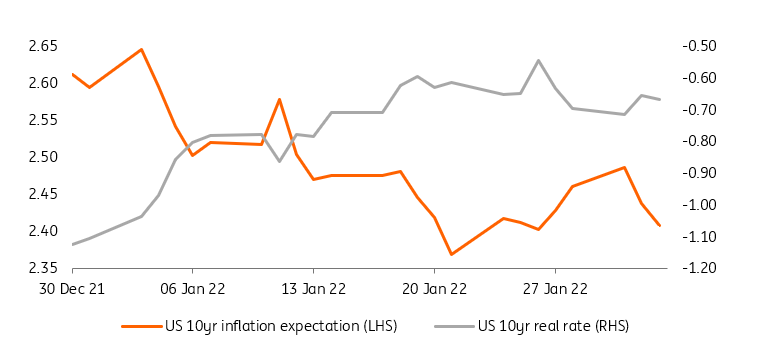

Real yields have risen as inflation expectations have fallen

The market reaction has not just been seen in higher 10yr nominal rates. Under the hood, we see that rises in real rates have been the dominant driver. Inflation expectations have in fact been easing, and thus acting to curb rises in nominal rates. But as real rates have risen by more than inflation expectations have fallen, the net effect is higher nominal rates. Lower inflation expectations will please central banks, as it shows that their actions (even if only verbal, e.g. the Fed) are having the required effect.

A tightening in liquidity conditions through 2022 will prove the tipping point for another lurch higher in market rates

The big question is what happens now. macro factors beyond the Omicron-impacted turn of the year are robust and should pull rates higher. This will be muted by buyers of bonds that continue to show up as a supportive factor on the flows front. Weak data in the current quarter will provide a short-term excuse to buy bonds, although the market should look through this.

So, other factors? There are many, in particular on the liquidity reduction front. By mid-year, the Fed will have started to take liquidity out of the system by allowing maturing bonds to roll off the curve. This has the rounded effect of reducing bank reserves and tightening liquidity. Basically, the imbalance in the US between liquidity and collateral needs to shape-shift, and that will require significant volume reductions in liquidity before having an effect. It is still a tightening though, even if it's not having a material effect until later in 2022.

One measure of the ample room the Fed has for liquidity reduction

In addition, early eurozone targeted longer-term refinancing operations (TLTROs) repayments in June (€800bn) will effectuate a tightening of euro financing conditions, against a backdrop where the European Central Bank (ECB) will also taper in 2H22, and is shaping up to hike rates in 2022 (yes we used the word hike, a foreign term in ECB circles for more than a decade). This is a big deal. The discount is building already, but there is much more to go.

There are two other factors that will evolve over the course of 2022. First, both the Fed and the ECB have the potential to sell bonds back to the market. Now they are unlikely to do this, but it remains a possibility, especially for the Fed, that the market should at least acknowledge as it discounts where market rates should sit. Second, as the Fed hikes rates, foreign players will find it easier to synthetically create alpha through buying dollars cheaply in foreign exchange forwards, which can reduce demand for vanilla US treasuries.

There is enough here to force market rates higher than they are today. The US 10yr should break above 2%. We’re not calling for it to go much above 2.25%, as we acknowledge the demand effect which is robust and is likely to remain a factor. The euro 10yr swap rate should get to the 75bp area, or at the very least remain comfortably above 50bp. And the 10yr German yield should not be dipping materially negative again. In fact it is on a journey to 25bp.

And let's first put the Russia / Ukraine issue out there. Suffice to say that a deepening in the crisis puts a typical flight-to-safety bid into US treasuries, pulling market rates lower. How much? Depends on how bad. For now we're assuming a status quo. But it's digital – an unpredictable on/off switch that can flick back in to dominate. Let's leave it at that.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: The masks, and the gloves, are coming off

- This bundle contains 15 Articles