US growth to rebound as Omicron caution fades

- 4 February 2022

- United States

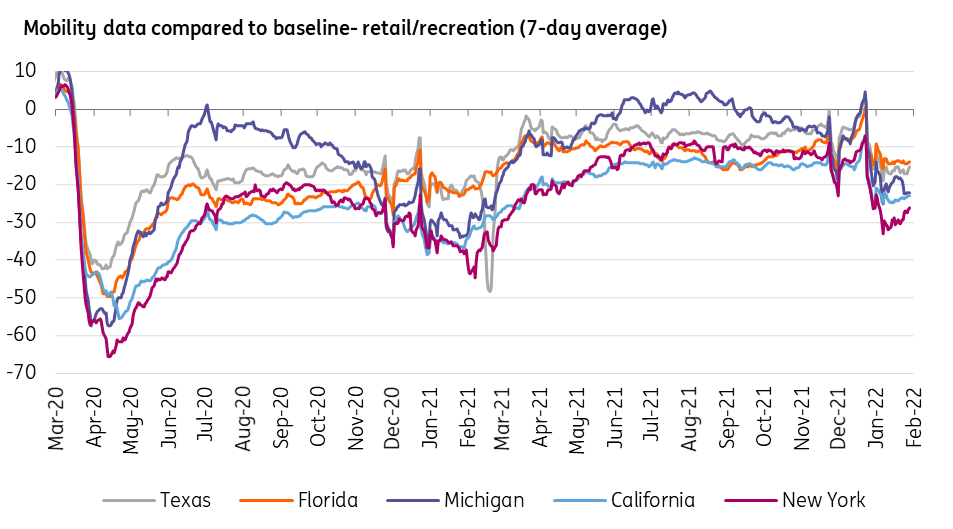

The steep fall in mobility and consumer spending in December and January reflects Covid caution and threatens economic contraction in the first quarter. But as the Omicron wave passes, strong underlying fundamentals point to a rapid recovery that will set the Federal Reserve on the path of five rate hikes in 2022

Fed sounds the call for action

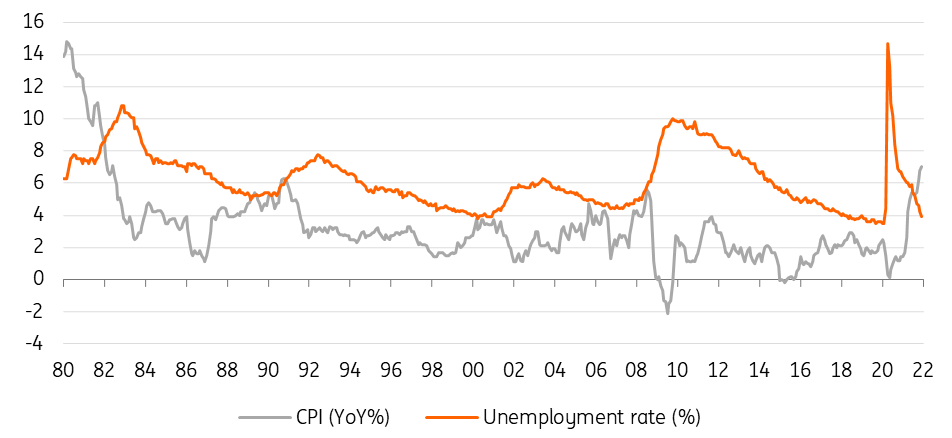

The US economy is now more than 3% larger than before the pandemic struck, inflation is running at 7% year-on-year and the unemployment rate is back below 4%. Given this backdrop, the Federal Reserve has given markets the nod to say it is ready to raise interest rates in March and follow this up with a series of rate hikes throughout 2022.

After a hawkish post-Federal Open Market Committee (FOMC) assessment from Fed Chair Jerome Powell, where he refused to rule out raising rates at every meeting this year, the market is now settling on four or five hikes for 2022. We are at the more aggressive end and expect the Fed to kick off with consecutive 25bp moves in March, May and June with additional increases in September and December.

They could of course do more, but with the Fed set to allow some maturing assets to run off its $9tr balance sheet from July onwards, this quantitative tightening can do some of the heavy-lifting with the added benefit of helping to keep the yield curve positively sloped.

US unemployment rate versus consumer price inflation 1990-2021

Covid caution means near-term economic weakness

There have been some calls for an initial 50bp as a signal of intent to get inflation under control, but given the Omicron wave dampened activity and hiring in the early part of 2022, we think this is a low probability event.

In fact, our 1Q gross domestic product (GDP) growth forecast is now 0% with consumer weakness in November and December showing little sign of abating through January. The massive inventory rebuilding experienced in 4Q21 is also likely to partially unwind and we doubt that exports will grow anywhere near the 24% annualised rate seen in the final three months of last year. As such we can’t rule out the possibility of a negative 1Q GDP print.

People movement dropped sharply through December and early January

Worker demand to keep boosting houshold incomes

Nonetheless, we are hopeful that better data in February and March will set us up for that first rate hike as well as a strong economic expansion in 2Q. Covid cases are falling in many parts of the US and this should result in consumers and businesses engaging more fully with the economy again.

Household fundamentals are in good shape with household wealth having risen $30tr since the end of 2019. Workers are also feeling more of the benefits from growth through higher incomes. Demand for workers is at record levels – the chart below shows there are 1.7 job vacancies for every unemployed person in the US – and the quit rate is also near record highs, suggesting companies are not only having to pay workers more to recruit staff, but also consider paying more to retain current employees.

Ratio of job vacancies to unemployed people has never been higher

Economic strength set to broaden

While wage growth isn't keeping pace with the cost of living at the moment, we expect better news for the second half of the year as inflation starts to slow. Fed rate hikes will take some steam out of the economy, but inflation is being primarily driven by supply-side pressures and we are cautiously optimistic that production bottlenecks and Covid-driven worker shortages will gradually improve and allow inflation rates to slow towards 3-4% by year-end and back to 2-3% in 2023.

At the same time, corporate investment intentions remain firm and inventories will continue to be rebuilt over the next couple of years. Then there is the already-approved Federal government investment programme, while President Joe Biden is seemingly acknowledging that by dropping some of the more contentious policies within his Build Back Better plan he stands a better chance of getting at least part of the package approved. After all, he needs all the good news he can get going into November’s mid-term election where the Democrats risk losing control of Congress, which would bring their legislative agenda to a grinding halt.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: The masks, and the gloves, are coming off

- This bundle contains 15 Articles