Monitoring Turkey: Inflation fever

Turkey's inflationary downtrend ends as most factors are likely to exert upside pressure in the near term. While the Government pledges to fight inflation, its target is a soft landing in economic activity that implies quite a slow normalisation in economic policies amid a challenging disinflationary process

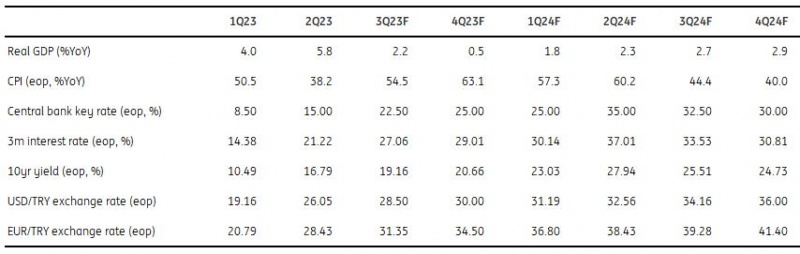

Turkey at a glance

- According to early indicators in July, moderation in business sentiment, both sectoral and consumer confidence are likely reflecting currency volatility in the aftermath of elections, and that's hinting at some easing in activity.

- With a near double-digit monthly increase, annual inflation jumped again in July, ending a deceleration phase which started in October.

- The Central Bank of Turkey raised its year-end and 2024 inflation forecasts by 35.7pp to 58.0% and 24.2pp to 33.0%, respectively. Following these revisions, the CBT’s year-end projection moves closer to that of market consensus as economists have started revising year-end forecasts to 60% or more.

- The CBT hiked its policy rate by 250bp (to 17.50%) with another under-consensus move. The bank announced a number of "quantitative tightening and selective credit tightening” measures, as signalled by the MPC.

- The balance of payments data once again confirms a growing need for a rebalancing in the economy. Going forward, we will likely see an improvement in the current account, as evidenced by the normalisation of energy prices and continuing strength in tourism.

Quarterly forecasts

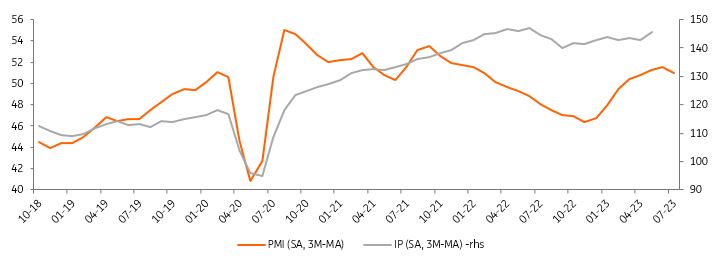

PMI below 50 in July

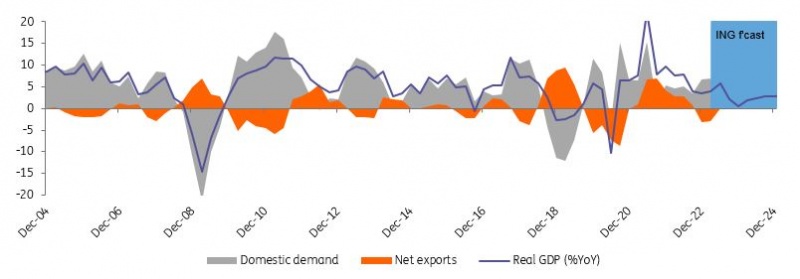

As hinted by May industrial production figures, economic activity remained robust in the second quarter, which was also evidenced by other indicators and confidence indices:

- After the negative impact of the February earthquakes, all sectors have recovered according to turnover indices

- Capacity utilization continued to increase in the 2Q

- Real sector confidence maintained recovery since the beginning of this year and turned stronger last quarter, while construction, services and trade sectors contributed to activity.

However, for the third quarter, moderation in business sentiment, sectoral and consumer confidence indicators hint at some easing in the activity. Additionally, manufacturing PMI that was above 50 in the first half returned below that threshold in July, standing at 49.9 and implying a momentum loss. This is likely attributable to currency volatility in the aftermath of elections, weighing on both input costs and selling prices and adversely impacting demand, hence making it harder for firms to secure new business.

Turkish Real GDP

%YoY, and contributions (ppt)

Industrial Production close to its peak

May's Industrial Production figures revealed a calendar-adjusted decline of 0.2% YoY, while in seasonally adjusted terms, it rose by 1.1% MoM, pulling the index close to the peak we saw just ahead of the February earthquake. Given that the religious holiday moved from May to April for Ramadan and the 'bridge day' impact attributable to the extended holiday is not fully captured by regular seasonal and calendar adjustments, the overall IP performance is hard to assess. With the May data, the performance in 2Q has strengthened to 2.0% QoQ implying robust economic activity.

Breaking it all down, intermediate goods provided the highest contribution to the headline with 0.4ppt though the sequential increase was weak with 1.0%. This was followed by capital goods pulling the headline by another 0.4ppt, while on the negative side, nondurable goods dragged by -0.1ppt. As for sectors,, motor vehicles, other transportation (dominated by defence industry products) and fabricated metal production were the major supportive items.

IP vs PMI

Unemployment rate again in single digits

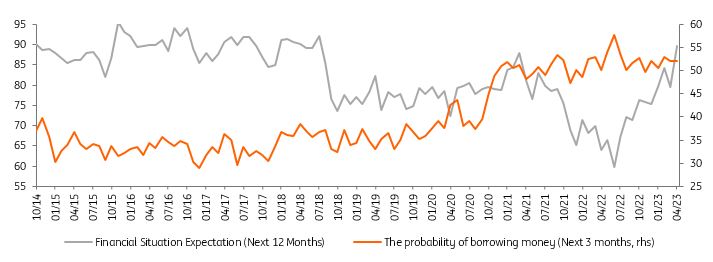

According to the May data, retail sales volume on a calendar-adjusted basis increased by 28.4% YoY in May, while the seasonally and calendar-adjusted index rose by 2.1% MoM, standing now at a new historical high. Again, looking at the breakdown, non-food sales (excluding automotive fuel) and food groups surged by 36.9% YoY and 22.6% YoY, while automotive fuel sales rose 10.9% YoY.

The highest annual increase in non-food sales was again observed in the computer-communication devices group, with 73.4% YoY. The data reflected that domestic demand growth maintained its strength in the middle of the second quarter after a robust performance in 1Q. On the other hand, the (seasonally adjusted) unemployment rate recorded a sharp drop in May to 9.5%, the lowest rate since early 2014. The data showed that the labour market left the earthquake's impact behind.

Retail sales vs consumer confidence

Central bank more than doubles its inflation forecast for 2023

In her first public appearance, Central Bank of Turkey Governor Hafize Gaye Erkan held a news conference to introduce the third Inflation report of the year. The CBT raised its year-end and 2024 inflation forecasts by 35.7pp to 58% and 24.2pp to 33%, respectively. Following these revisions, the CBT’s year-end projection moves closer to the market consensus, as economists have started revising year-end forecasts to 60% or above.

According to the CBT, the factors that played an important role in the revision of inflation forecasts for this year and next are food inflation, TRY-denominated import prices, the output gap, administrated prices and unit labour cost, and finally, forecast deviation and a change in the forecasting approach. With respect to the latter, Erkan, who was appointed in June, said that in the path presented in the previous inflation report, the forecasting approach put a higher emphasis on the intermediate target, while in the latest report, the bank's projections have been aligned with its technical forecasts, in view of the changing macroeconomic outlook.

CBT’s Inflation Forecast

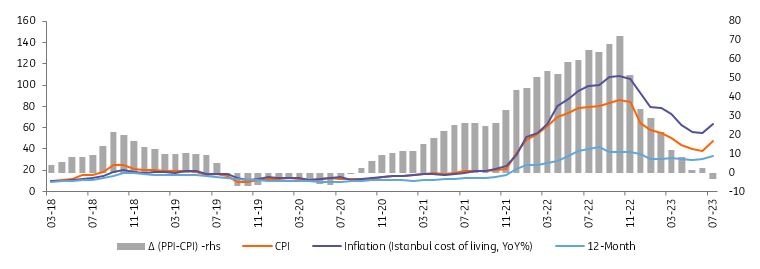

Record high July CPI inflation

Turkey's CPI inflation rate jumped to 9.49% in July against a consensus of 9.1%. It's the highest July figure since the current series began in 2003. Annually, consumer prices have jumped to 47.8% from 38.2% a month ago, marking the first increase since October. Despite supportive base effects, the monthly inflation was much higher than the long-term average of previous July readings.

With the July data, cumulative inflation in the first seven months of this year reached 31.1% (vs 58% CBT forecast for the whole year in the latest inflation report). The uptrend will likely continue until the second quarter of next year, given that all major inflation drivers are becoming less supportive with pressures from FX-related effects, administered prices and wages.

The Central Bank of Turkey envisages a transition towards a disinflation and stabilisation period. It expects inflation to peak at around 60% in the second quarter of 2024 and adopt a declining trend thereafter. In this environment, while the CBT has taken the initial steps towards normalisation in interest rates and exchange rate policy after the elections, the equilibrium point of exchange rates and interest rates will be key issues watched by the markets, along with the policy moves related to macro-prudential regulations and publicly determined prices.

Inflation outlook (%)

Higher deficit and unidentified outflows weigh on reserves

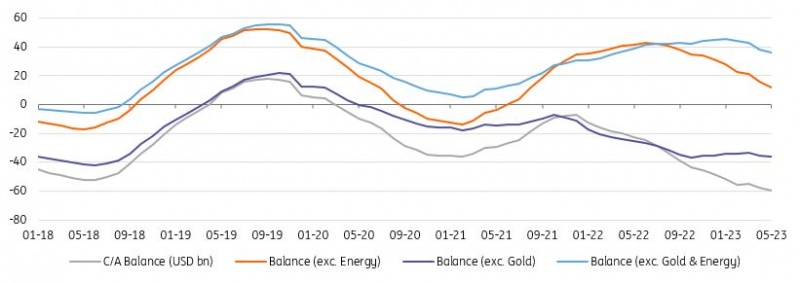

External developments have remained challenging in May with another higher-than-expected current account deficit at US$7.9bn, widening the 12M rolling figure further to US$60bn (translating into c.6.1% of GDP), the highest since late 2013. A quick glance at the May data points to a similar performance in the services balance with respect to the same month of 2022 though a relatively wide deficit in the goods balance driven by higher core trade and gold deficits despite improving energy trade balance.

The Capital Account, on the other hand, saw net outflows at US$-1.2bn. With the monthly C/A deficit and outflows via net errors & omissions at US$7.4bn, official reserves recorded another large decline at US$16.6bn (not only the cumulative deficit in the first five months but also part of large unidentified outflows at US$13.7bn in the same period).

Turkey's Current Account

12M rolling, US$bn

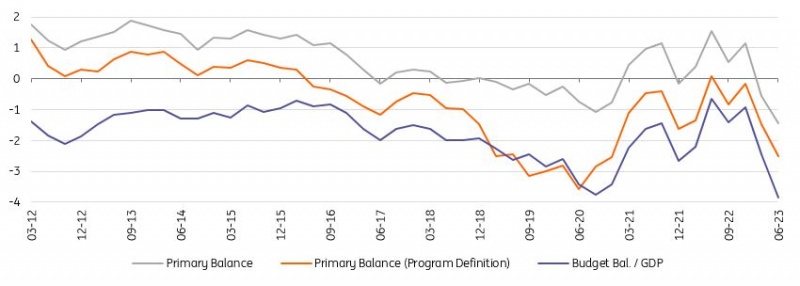

Budget deficit remains a rapid widening trend

In June, the budget posted a deficit of TRY219.6bn from a mere TRY31.1 in the same month of last year, while the deficit for the last 12 months rose to TRY715.9bn (3.9% of GDP). According to the programme (IMF) defined primary balance realisation, which excludes one-off revenues, the 12-month rolling primary deficit was at 2.5% of GDP.

The June budget results reflected a significant year-on-year deterioration with a more pronounced increase in non-interest expenditures due to higher current transfers, FX-protected deposits related costs and transfers to SEEs, despite the increase in direct and indirect taxes. According to Finance Minister Mehmet Simsek, earthquake-related expenses are expected to reach TRY761.7bn (US$29.2bn) this year, equivalent to 3.1% of national income. In the MTP (Medium Term Programme) announced last year, the budget deficit for 2023 was estimated at TRY659.4bn (3.5% of GDP). However, after the recently introduced supplementary budget, revenues were raised to TRY4.9tn and expenditures to TRY5.6tn, while the budget deficit forecast remained unchanged.

Budget performance

% of GDP

The 'under'-delivery continues

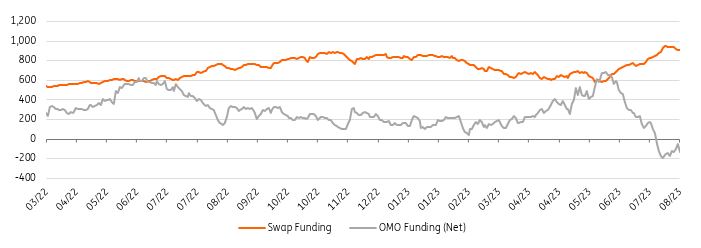

Following its first hike in more than two years by 675bp in June, the CBT continued the hiking cycle with another 250bp to 17.5%, though the pace has remained below what market consensus envisaged. While the bank has maintained a newly adopted inflation focus, the forward guidance has remained unchanged with the reiteration of additional tightening moves "in a timely and gradual manner until a significant improvement in the inflation outlook is achieved".

The CBT also signalled "quantitative tightening and selective credit tightening to support the monetary policy stance" in its rate-setting statement. Following that signal, it hiked Required Reserve Ratios for FX-protected deposits to 15% to mop up excess liquidity in the system. With the decision, TRY450bn is expected to be withdrawn from the system, again creating a TRY liquidity deficit.

We've also seen a number of other noteworthy measures:

- A revision of monthly growth limits for different types of credits

- The removal of the first tier for TL commercial loans

- Additional moves to support exporters’ access to financing, i.e. regulation changes related to rediscount credits from the CBT.

Central bank funding

Policy actions to shape market movements

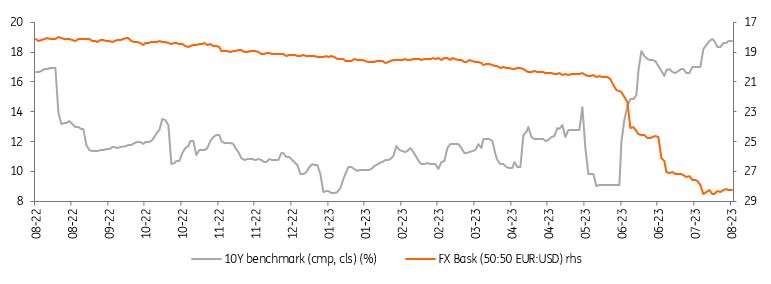

Since May's elections, the lira has posted a more than 30% drop, moving from the 19-20 range to around 27. While there is stability lately with lighter liquidity and higher tourism revenues, continuing external imbalances, capital flow developments, and the level of FX reserves will likely determine the TRY outlook for the rest of the year. In a news conference, the CBT Governor reiterated the decision to provide banks with FX directly if there is demand due to maturing FX-protected accounts. She added that the CBT does not utilise the protocol signed with the Treasury to facilitate state banks' activity in the currency market. It's worth noting that the CBT`s FX reserves have significantly increased since the elections.

Changes in the MPC sending a signal that the shift towards a more conventional monetary policy framework will continue has lately supported sentiment. The CBT will likely continue rate hikes though the pace is expected to be gradual. However, with the downtrend on the inflation side ending, rising inflation challenges and the gradualist stance of the CBT imply the real policy rate is set to remain in deeply negative territory. A loose fiscal stance should also keep the pressure on local issuance. Given this environment, the revisions in macro-prudential rules related to security maintenance requirements and the CBT being actively involved in the bond market (though purchase auctions ceased recently) will be closely watched.

10Y local bond vs FX basket

Clearer policy shift needed to see further spread tightening

Recent news around clear and direct investment commitments from the Gulf states and signs of a policy shift in the right direction has been taken positively by investors in Turkey's dollar sovereign bonds. However, given inflation pressures are set to increase while the external and fiscal pictures remain challenging, EM investors will likely need to see more significant steps towards monetary tightening for Turkey's sovereign credit spreads to tighten further from current levels.

There likely remains some scepticism about the durability of recent policy changes, especially given the first few steps have underwhelmed versus expectations. At the same time, credit spreads for Turkey are at the tight end even of their 5-Year Range, although strong technical support from local demand should help avoid a significant selloff in the event that global sentiment turns more negative.

ICE US$ Bond Sub-Index Spreads vs USTs

Download

Download articleThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more