Monitoring Hungary: Heading into the great unknown

- 10 February

- Hungary

In our latest update, we reassess our Hungarian economic and market forecasts at a time when the country is approaching a general election that could bring about significant changes regardless of who wins. We’ve entered the year with the hope that this will finally mark the end of the prolonged period of stagnation

Hungary: At a glance

- Due to a weaker-than-expected performance in the fourth quarter of 2025, we have downgraded the GDP outlook for 2026 from 2.3% to 1.9%, due to the carry-over effect.

- December's retail sales and industrial data were disappointing, but based on some important leading indicators, we believe that a potential upturn is closer than ever.

- The labour market is under pressure from a shrinking working-age population, labour hoarding and strong minimum wage growth.

- The external surplus is still holding up well. While stronger growth in domestic demand will increase imports, export activity will be boosted by new productive capacities.

- Inflation caused an unwelcome surprise in December, mainly driven by the service sector. Recent price trends in fuel and food, as well as government measures, will keep inflation at an average of 2% in the first quarter of 2026.

- Low inflation and a strong forint will provide the Monetary Council with a golden opportunity to begin the easing cycle in February. We predict a total of 75bp cuts in 2026, with the base rate ending the year at 5.75%.

- We see fiscal slippage in 2026 and 2027 based on recent history and our differing macro projections compared to those of the government.

- We forecast a deficit-to-GDP ratio of 5.2-5.5% in 2026-27, with higher bond supply than planned.

- The general election is taking place on 12 April 2026. Some political analysts are warning that the governing party, Fidesz, has a higher chance of winning a simple majority than is generally believed.

- Forint benefits from a weaker US dollar and growing hopes of a peace deal between Ukraine and Russia, while domestic rates provide significantly better carry within CEE peers, pushing EUR/HUF to new lows.

- Rates have room to price in more NBH rate cuts, especially in the belly curve, given the view of low inflation and a weak economy. Bonds should see gains in most post-election scenarios while valuations remain cheap.

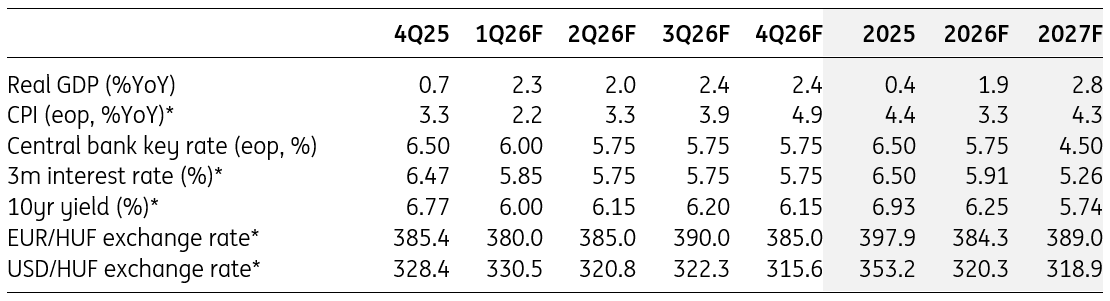

Quarterly forecasts

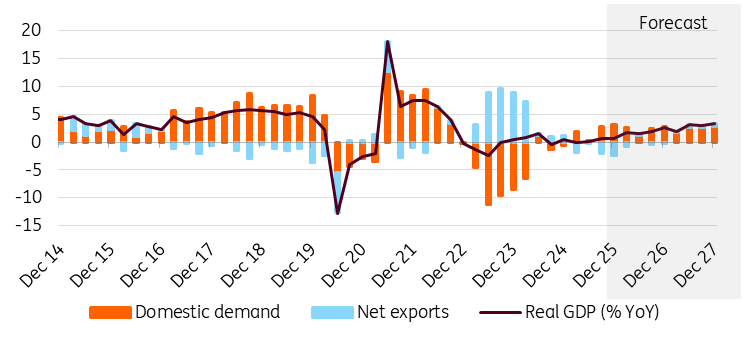

After an abysmal year, Hungary may be heading towards growth

The lacklustre fourth quarter performance of 0.2% QoQ and the full-year GDP growth of 0.4% were both disappointing. Increased government spending has not been a factor in the economy's overall performance. We are still hoping for a turnaround in 2026, although this may be slower than previously anticipated. Our forecast of 2.3% GDP growth has been revised down to 1.9% for 2026.

Consumption may be the driving force in the early part of this year, primarily due to new fiscal stimuli in an election year. In the second half of 2026, we see improving export activity driven by new factories gradually ramping up production in 2026. Strong import demand driven by consumption, coupled with some recovery in investment and improving but sluggish external demand, suggests that net exports will hurt economic growth this year.

Real GDP (% YoY) and contributions (ppt)

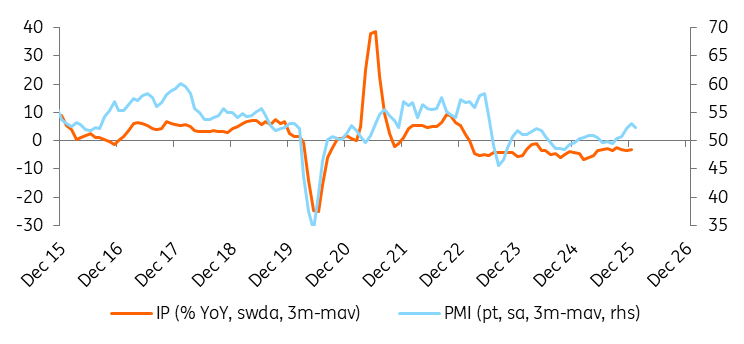

Hopes emerging around the Hungarian industry

Growth in the volume of production was 0.9% MoM, which seems decent at first glance. However, given the 2% MoM decline in November, Hungarian industry as a whole was unable to make up for this with the December improvement. Due to last year's extremely low base, the year-on-year index improved significantly, not just in general but in all major sub-sectors.

Given the new export capacities that have become available throughout this year, we can perhaps be optimistic about a more lasting improvement. However, we believe this is more likely to occur in the second half of the year. By the end of 2026, the fixed-base index may approach the monthly average for 2021. Therefore, while not explosive, the overall annual performance of Hungarian industry in 2026 may see sectoral growth of around 3% year-on-year on average.

Industrial production (IP) and Purchasing Manager Index (PMI)

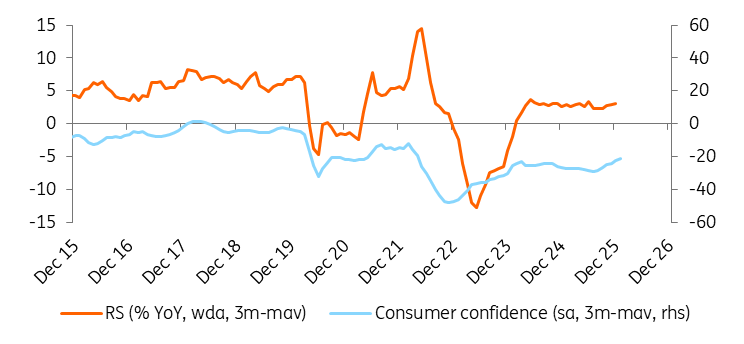

Retail sales growing steadily, with potential to grow faster

Volume of retail sales grew by just 0.2% MoM in December. The silver lining is that we have now seen modest growth for three months in a row, so the sector's performance is more consistent. However, the end of the year was disappointing overall.

Looking at the longer-term trends, retail sales volume in December was 3.4% higher than the monthly average for 2021, indicating that the sector is growing slowly but surely. While retail sales lack booming momentum, improving consumer confidence in recent months may indicate a more sustained upturn in consumption, which would put the economy on a steeper growth path. However, if the demand stimulus induced by this improving confidence fails to materialise, it could pose a serious problem for the real economy, since consumption is the only factor capable of driving the economy in the short term.

Retail sales (RS) and consumer confidence

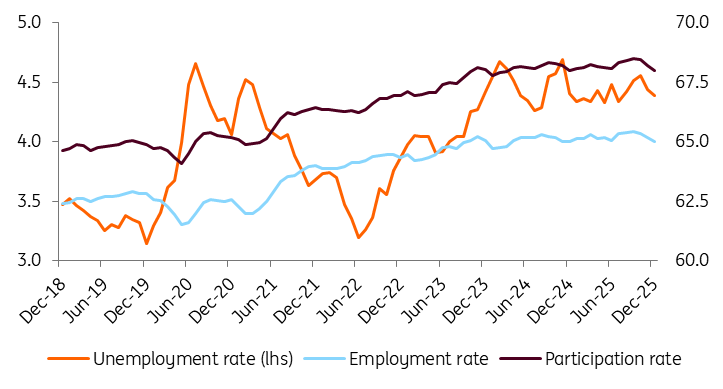

The labour market is still tight but there is a big problem

The unemployment rate was 4.4% in the fourth quarter of 2025, with all the other major labour market ratios looking relatively sound. However, looking beyond the short term, a serious long-term problem is emerging in Hungary. Since mid-2022, when the number of unemployed people was at a record low, the working-age population has fallen by 142,000. This equates to the total population of Hungary's fifth-largest city.

In the meantime, the number of people in employment fell back to around the average of 2021-22. Hence, the lack of easing of the labour market has an impact on average wage growth, which remains high in almost all sectors. As a result of expected lower inflation and continuing high nominal wage growth (around 10.5% in 2026), we expect real wages to grow even further.

Historical trends in the Hungarian labour market (%)

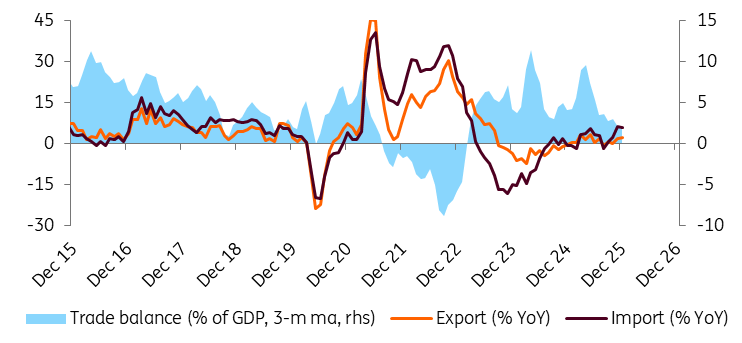

External balance will be supported by new capacities

Export volumes fell by 0.5% in 2025, while imports rose by 2.8% YoY. The external goods balance was €0.44bn lower than in 2024, standing at €8.25bn. As the large FDI projects in manufacturing entered their final phase, imports increased, while the lack of external demand kept exports in check. The outlook is somewhat mixed.

Some companies have decided to reduce the number of shifts due to retooling and demand issues, while new producers will gradually increase production and exports throughout the year. If the growth of consumption accelerates and there is a minor shift in investments, this could boost the country’s import needs. The net impact could be slightly positive in terms of value, so we see an improvement in the external surplus in 2026. However, volumes will tell a different story, with net exports having a minor negative impact on real GDP growth.

Trade balance (3-month moving average)

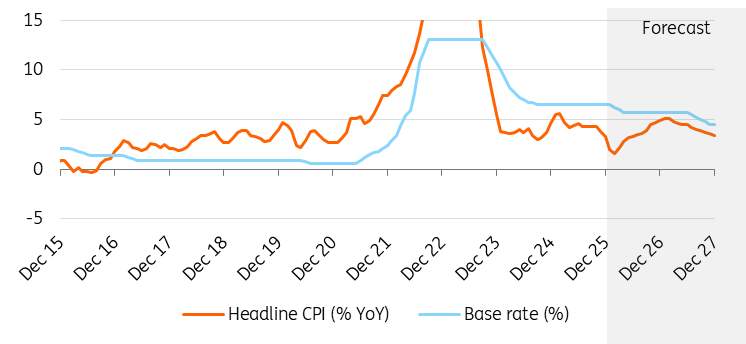

Inflation to hit an eight-year low rate in early 2026

The latest inflation print for December has left analysts with a somewhat bitter taste in their mouths. At 3.3% YoY, the inflation rate exceeded the market consensus; however on a monthly basis, prices rose by only 0.1%.

The biggest surprise came from services, primarily those related to transport, tourism, and telecommunications. These were mostly one-offs, and we expect the muted monthly repricing to continue in the coming months. Lower fuel prices, the possible extension of price shield measures, and the one-off capping of household energy prices will result in lower-than-usual repricing in the first quarter. Therefore, we forecast inflation to average around 2.0% in 1Q26, followed by an acceleration to 4.0-4.5% YoY by the end of the year. This would result in a comfortable average inflation of 3.3% in 2026, followed by a 4.3% average in 2027.

Inflation and policy rate

Monetary easing will begin in February

At its first rate-setting meeting of 2026, the National Bank of Hungary kept the base rate unchanged. This followed the rather unfavourable inflation figures in December and was widely expected. However, this was probably the last stop before the easing begins, with the long-awaited rate cut expected at the 24 February meeting.

Inflation is expected to drop to a multi-year low in January, with EUR/HUF approaching its lowest level in two-to-three years. This should convince the Monetary Council to cut the 6.50% base rate by 25bp in February. We think it won't be a one-off cut, as the central bank will follow this with another 25bp cut in March.

The tricky part comes with the general election in April and the related possibility of FX volatility, which could be too great for continued easing. The NBH still favours stability and would prefer to see a strengthening trend rather than a weakening. However, if the situation is favourable, we believe another rate cut may follow, bringing our terminal rate forecast for 2026 down to 5.75%.

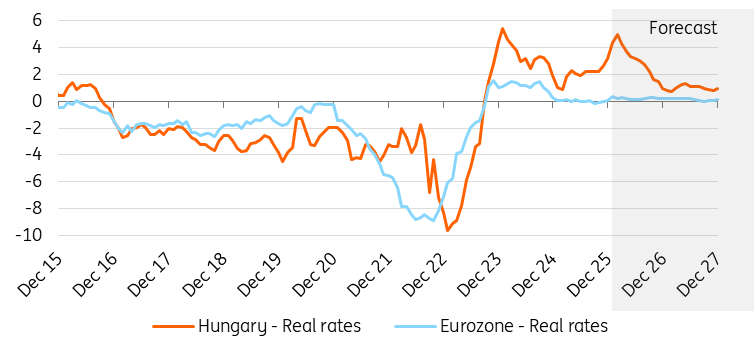

Real rates (%)

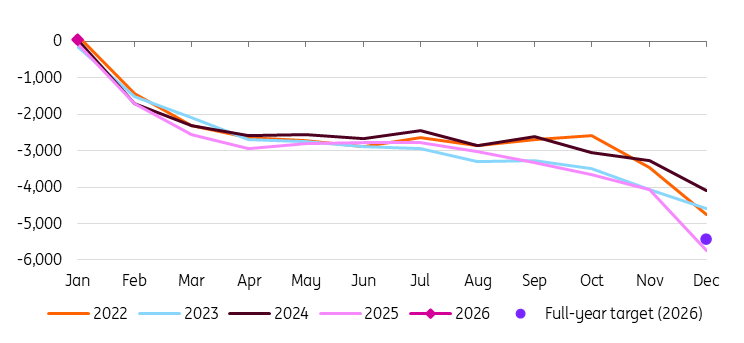

Hungarian budget under pressure

The cash-flow budget deficit at the end of 2025 was HUF 5,739bn, which is significantly higher than the figure projected in November. The extremely high monthly deficit of HUF1.7tr in December is mostly related to increased government expenditure on lending programmes, as well as on some EU projects and on state asset-related expenditure.

From an accrual perspective, last year's deficit was around 5% of GDP, and the debt-to-GDP ratio rose by 1ppt to 74.6%. Both figures are higher than those flagged by the Ministry before the end of the year. Based on the latest official data, the government is aiming for a deficit of 5% of GDP in 2026, but, in contrast to previous communications, the primary balance is expected to be far from balanced at -2.5% of GDP.

In a recent interview, PM Viktor Orbán discussed a 5% deficit for 2027, despite the Ministry's target of 4%. Overall, based on the difference in the macro projections, we expect the deficit to be in the range of 5.2-5.5% over the next couple of years. Therefore, we expect an increase in financial needs and a higher bond supply, especially if Hungary fails to secure the planned EU funds (some RRF and SAFE money).

Budget performance in cash-flow perspective (year-to-date, HUFbn)

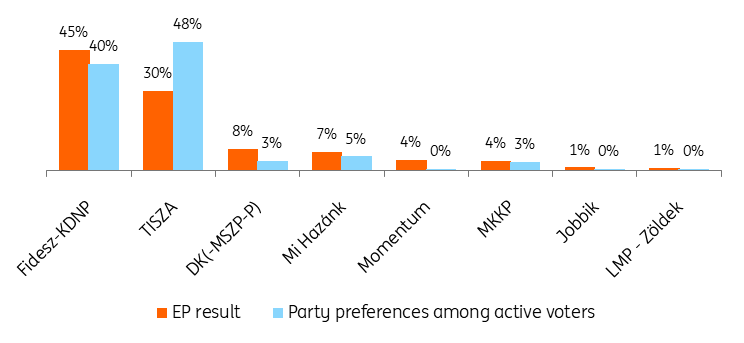

The political race can be tighter than you think

The general election, which will decide the fate of the 199 seats in the Hungarian Assembly, will take place on 12 April 2026. Of these, 106 will be allocated via single-member constituencies, while the remaining 93 will be decided by the party list system. As the election polls are based on party list voting, it is worth taking these numbers with a pinch of salt.

According to most political analysts, the main opposition party (Tisza)'s recent lead can be translated into a tight race based on the electoral system. While public opinion suggests a high likelihood of a change in power, some analysts warn that the governing party, Fidesz, has a higher chance of winning a simple majority than is generally believed.

In our view, the worst-case scenario is a hung parliament and lengthy legal debates about the fate of some seats, which could create major market volatility. Our forecasts are based on a no-policy-change scenario, in line with academic standards.

Average of opinion polls (end-Jan 2026) and the results of the 2024 EP election

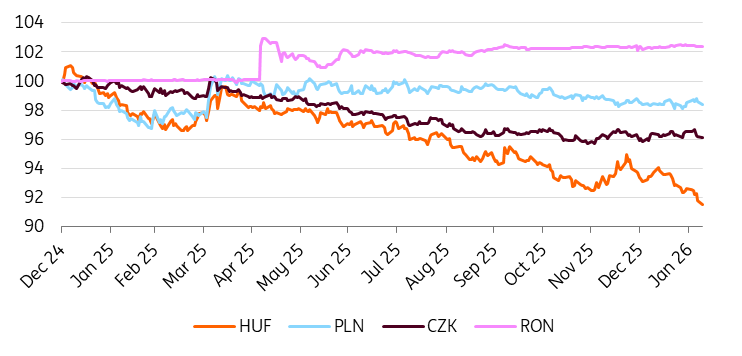

Forint benefits from global and domestic factors

The forint continues to enjoy market favour. While EUR/PLN and EUR/CZK have remained range-bound since the beginning of the year, EUR/HUF is reporting new lows every day with fresh more than two-year lows.

On the one hand, we see global factors behind this, such as a weak US dollar and higher hopes for a peace agreement between Ukraine and Russia, from which we believe the forint would benefit the most in the CEE region. On the other hand, high rates versus peers and attractive carry are helping locally despite the impending restart of the cutting cycle.

We see more gains in the months leading up to the elections, given that a rate cut in February or March is almost fully priced in. However, further direction will depend entirely on the election outcome and the steps of the new government, in our view.

CEE FX performance vs EUR (31 Dec 2024 = 100%)

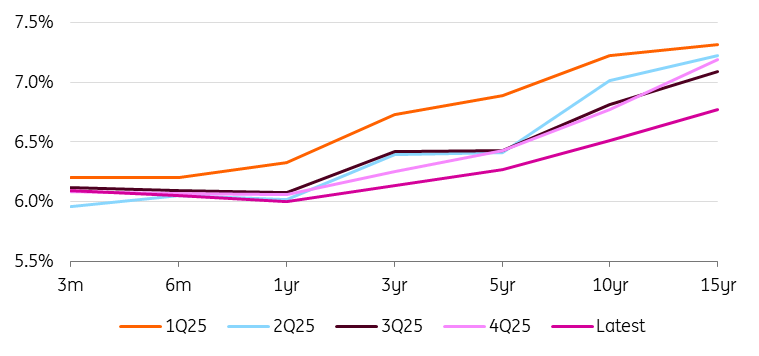

Bonds a good choice for all scenarios

In the rates market, after the higher-than-expected inflation in December, expectations for NBH rate cuts have cooled somewhat and we have seen some normalisation of expectations closer to our forecast. However, the key, similar to elsewhere in the CEE region, is January inflation. The NBH indicated a low bar for a rate cut at its last meeting in January and we believe that inflation below 3% will be a sufficient demand.

The market is currently pricing in a roughly 70% chance of a rate cut in February and roughly four rate cuts in the entire cycle. Compared to our forecast of a rate cut in February and March and a terminal rate of 4.50% at the end of next year, this suggests more downside for the front of the curve if January inflation confirms soft pricing.

But more dovish market expectations are also supported by a strong forint and a weak economy, where together we see more story in the priced terminal rate and lower belly of the curve than the specific timing of rate cuts this year.

Hungarian sovereign yield curve (end of period)

Hungarian government bonds (HGBs) see favourable conditions in the overall setup despite the April general election. It seems that the market has priced in all the fiscal premium after the budget revision in November, and in our view HGBs offer attractive levels and risk-reward within CEE.

In case of a government victory in the elections, some degree of fiscal consolidation can be expected in the coming years. In case of a change of government, on the contrary, a restart of relations with the EU and an inflow of some EU funds can be expected, which would help with financing.

At the same time, HGBs are still trading close to Romanian government bonds with significantly better fiscal metrics vs Romania and a restart of the NBH cutting cycle around the corner. Positive market sentiment is also indicated by the latest results of primary auctions, where the debt agency is meeting with significantly high demand. The main risk remains the political gridlock and the unclear outcome of the elections.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more