Monitoring Bulgaria: Euro adoption enters the final stretch

- 3 July 2025

- Bulgaria

Bulgaria's economy is showing quiet resilience in 2025, with strong consumption and wage growth masking industrial and trade weaknesses. Inflation risks persist, but euro adoption is nearly secured, marking a major milestone for the country

Bulgaria at a glance

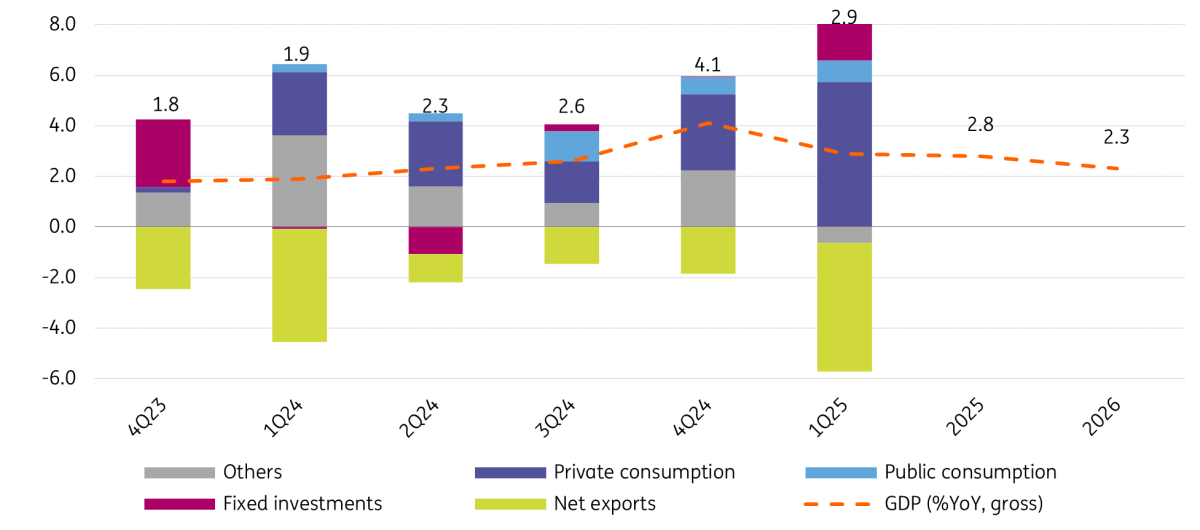

- GDP growth: Consumption continued to keep the lion's share in terms of positive contributions to growth, with investments yet to prove themselves. For 2025, we estimate similar growth to last year, at 2.8%, followed by a moderation to 2.3% in 2026.

- Industrial activity: A worsening dynamic in manufacturing activity took the sector’s output back to below its pre-pandemic levels. The fiscal stimulus across Europe, especially Germany, should add some tailwinds ahead, although productive investments remain equally important.

- Balance of Payments: The trade deficit worsened by 75% in January-April 2025 in annual terms. Visibly stronger deficits with China and Turkey, as well as a lower surplus with Germany, have dominated the picture. Potentially healthier surpluses on services stemming from tourism inflows should add a helping hand to the current account in 2025.

- Inflation and fiscal policy: We see the 2025 year-end CPI inflation at 3.9% and 2026 at 3.0%. In the short run, there are some upside risks at play, fuelled mainly by wages.

- Bulgaria's 2025 budget projects a deficit of 3.0% of GDP, which we continue to see as our base case too.

- Eurozone entry looks set for 1 January 2026, pending the Econfin’s adoption of the final legislative acts on 8 July. Ultimately, we expect all the remaining steps to follow as planned in the coming months.

GDP growth – not shining, but not out of shape either

After picking up some speed in 2024 versus 2023, annual growth in Bulgaria remained close to last year’s average in the first quarter of 2025, coming in at 2.9%. Private consumption and investments are on a visible upward momentum, counterbalanced by contractionary exports and a stronger pick-up of goods imports. Strong growth rates of private and public wages provided the tailwind.

On the supply side of the economy, wholesale and retail trade, as well as the financial services sector, continued to perform well through the first quarter. Meanwhile, the mining and utilities sectors fell again into contractionary territory.

On the outlook, we think that GDP growth will remain at a constant 2.8% in 2025. Wages should continue to find support in the tight labour market, benefiting private consumption to an extent. That said, net exports could remain a burden for growth in the coming quarters, especially in the short run, as the consumption momentum continues. Concerning the export-oriented industry, growth numbers could look better next year on the back of more stimulative fiscal policy across Europe (particularly in Germany), the positive combination of euro adoption and Schengen membership, and under the umbrella of base effects. At a more structural level, the recent lag in investments and EU-fund absorption adds headwinds to the country’s productive potential through the medium to long run. Still, broader infrastructure upgrades at a regional level with both military and civil utility should, to some extent, provide marginal offsetting benefits.

GDP and components

Industry – continuing to struggle

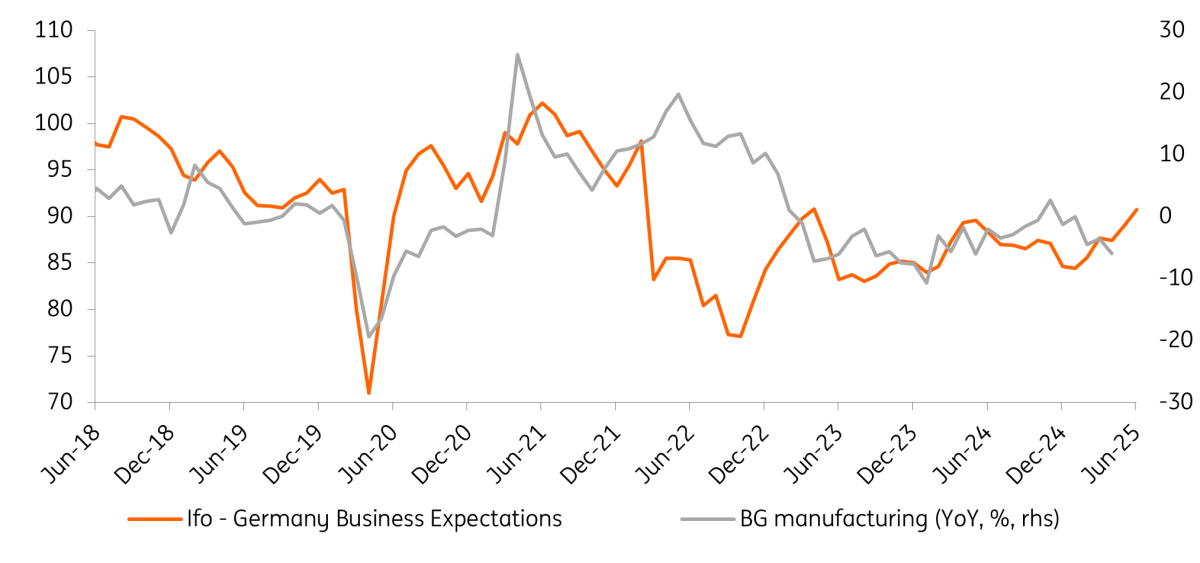

Industrial activity remained in negative territory, sitting at 6.0% below its pre-pandemic levels at the latest reading. The ongoing weakness of industrial activity in key trading partners – Germany and Romania – contributed here, to an extent. In manufacturing, year-to-date data shows an overall worsening situation culminating with a contraction in April and levels of output that have fallen yet again, slightly below their pre-pandemic levels for the first time since July 2021. As for other key components, both mining and quarrying, as well as energy production, remain more visibly below their pre-pandemic levels.

In certain subsectors, though, there have been improvements this year, particularly in the manufacturing of machinery and equipment, alongside leather, furniture and tobacco products. That said, the situation in sectors such as energy, pharma or basic metals production continued to weaken.

With the new fiscal stimulus in Germany underway, there are prospects of some tailwinds for the Bulgarian export-oriented industry in the medium term. In the short run, however, some small palpable gains could be more visible from the Schengen ascension, the euro adoption and regional infrastructure developments more broadly.

Industrial production

Trade and the balance of payments

The trade deficit worsened significantly through the four months of 2025, rising by a whopping 75% in annual terms. Rising non-EU imports – coupled with declines in both EU and non-EU exports – were at play, stemming from visibly higher trade deficits with China and Turkey, as well as a smaller surplus with Germany. Notably, there were also visible trade surpluses with Romania over the first quarter of the period.

On the services front, the country should continue to benefit from another year of healthy tourism inflows. Bulgaria’s resorts (both seaside and mountain) continue to remain a good value-for-money travel destination for both neighbouring countries and Europe more broadly, especially at a time when the European economy remains in a relatively weak state. This should continue to at least partially offset the growing deficits on the goods front this year.

Concerning other BoP categories, the capital account and secondary income accounts could benefit from new EU funds inflows in the second half of this year, on the back of both cohesion funds and two Recovery and Resilience Facility (RRF) payment requests intended to be sent this year, first one in July 2025 and another one later on in autumn.

On foreign investments, political stability would need to remain in place for some time before it drops down foreign investors’ risk heatmaps – although the euro adoption story, coupled with the country's competitive tax regime, could encourage new activity in the short run. The relocation of some firms from neighbouring countries is key to watch moving forward. There should also continue to be tailwinds from some NATO-led investments and regional projects like the Vertical Corridor.

Inflation: A somewhat elevated trajectory ahead

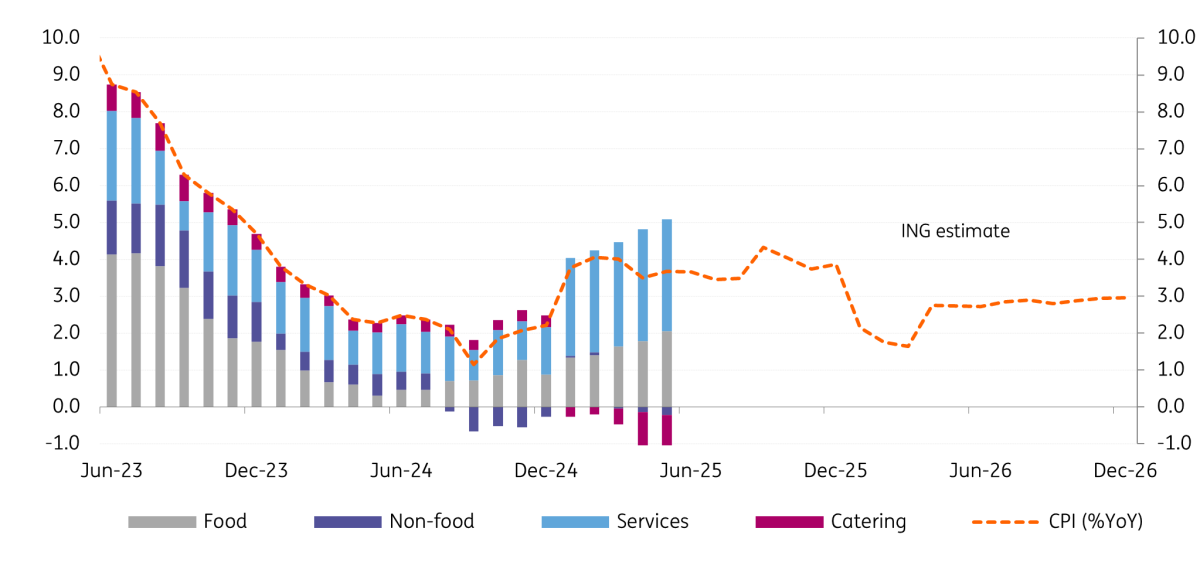

Inflation picked up quite visibly over the first quarter of the year and only moderated slightly through the second quarter, printing at 3.7%. The key drivers at play were the restored VAT rates on categories like restaurants and bread, higher utility prices and higher tobacco excise duties. Food price pressures and rising wages have also contributed. The liberalisation of the energy market for households no longer brings upside risks in the short run, as it has been postponed with an unclear timeline ahead.

That said, price gouging amid the upcoming euro adoption is reportedly an important factor to watch at this stage. Some upside pressures across the country stemming from the currency switch have been making the headlines recently, but various penalties, public awareness campaigns and even boycotts in some cases should, in principle, help the situation gradually cool off. The switch from lev to euro at a time when wage growth is on a rather strong momentum also partially adds to upside pressure..

Overall, we expect CPI inflation to end this year at 3.9% and next year at 3.0%.

Fiscal – an important consumption driver these days

Throughout the first five months of 2025, fiscal policy has continued to steer towards consumption-stimulating areas. Compensation for employees and social expenditures were 3.7 and 6.2 times larger than capital expenditures, visibly more as a proportion than in 2024, when these ratios stood at 3.0 and 5.1, respectively. These trends have recently grown in importance in the public debate surrounding the sustainability of the public wages trajectory and even some early considerations around competitiveness.

While fiscal discipline has been a key factor in Bulgaria’s public policies for some time, and the country’s public debt is not a concern right now, growing fiscal uncertainty fuelling potential consumption-driven activity dynamics ahead is a factor to monitor.

All in all, our base case remains for a 3.0% budget deficit in 2025.

Euro adoption set for next year

It has been our long-held view that Bulgaria's euro adoption process is more likely to align with the January 2026 timeline, rather than occurring earlier. With the European Central Bank and the EU Commission’s positive assessments of Bulgaria’s progress in June, the final step of the process at an external level is now the adoption of the final legislative acts by Ecofin at the 8 July meeting.

From there onwards, developments in the second half of the year should focus more on remaining technical and administrative fine-tuning. Mixed opinions across society on the euro project do increase governance difficulties in the near term, but our base case remains that the situation will remain manageable enough for the country to finalise its euro adoption and keep its fiscal stance in line with EU rules through the medium term.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more