Mixed US jobs data signals September pause

The US economy added fewer jobs than hoped in July, yet the unemployment rate fell and wage growth was stronger. A mixed outcome, which doesn't rule out further rate hikes from the Federal Reserve, but doesn't give the central bank the all clear on inflation risks either. Tighter monetary conditions will increasingly weigh on job creation though

| 187,000 |

Number of jobs added by the US economy in July |

Jobs disappoint, wages rise, unemployment falls

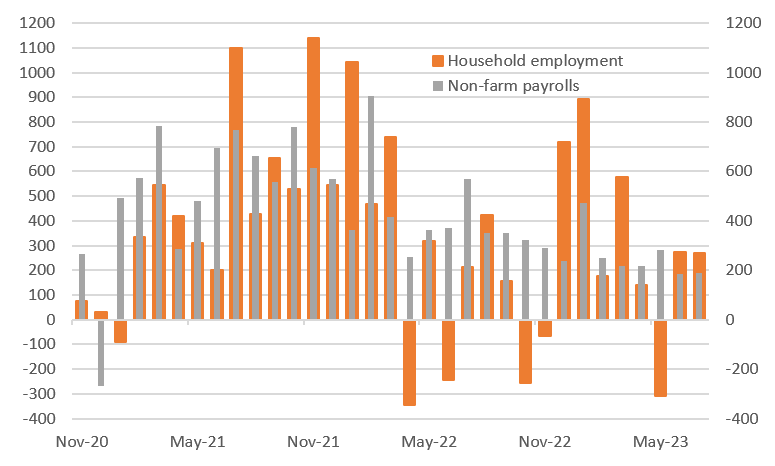

We have a very mixed US jobs report for July. US non-farm payrolls rose 187k versus the 200k consensus prediction and there were 49k of downward revisions. Manufacturing employment fell 2k with private sector employment rising 172k in total, a third of which came from healthcare. This is all from the establishment survey, which questions employers. The household survey is stronger, seeing the unemployment rate drop to 3.5% from 3.6% with employment rising 268k and unemployment falling 116k.

Employment change according to businesses and according to households (000s)

Fed to remain wary of a tight jobs market

Meanwhile, average hourly earnings rose 0.4% month-on-month/4.4% year-on-year, not 0.3%/4.2% as hoped. The participation rate held steady at 62.6%. The market is seemingly putting more emphasis on the wage and unemployment number rather than jobs, which is fair. Stickier wages and a tight jobs market will make their job of returning inflation to the 2% target more challenging. Nonetheless, this does contradict some of the evidence within the Fed's own Beige Book report that stated "contacts in multiple Districts reported that wage increases were returning to or nearing pre-pandemic levels". The Employment Cost Index, which is a broader measure of labour costs was also lower last Friday so any market moves should be fairly small, especially with CPI and PPI out next week.

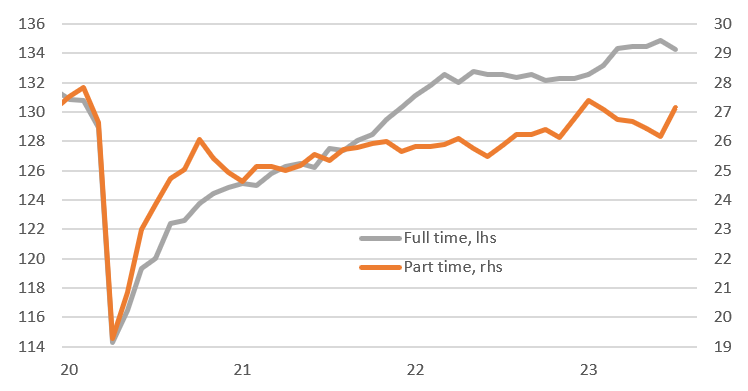

One area of disappointment within the household employment survey is that the strength was driven by part-time jobs. The household survey shows part-time employment rose just under 1mn last month while full-time employment fell nearly 600k. So while wage growth apparently remained robust, swapping full-time workers for part-time workers is in aggregate going to lower household incomes.

Full-time versus part-time employment (mn)

September Fed pause set to continue

On balance this report doesn’t suggest any need for renewed impetus for the Fed hiking interest rates again in September. The Fed have signalled a desire to tighten policy more slowly and the report appears consistent with the gradual cooling of the labour market. As mentioned, all eyes will now switch to CPI and PPI and a couple more 0.2% MoM prints as we and the market expect should further dampen talk of a potential September hike, of which only 4bp or 5bp is currently priced.

Furthermore, the move higher in Treasury yields and the dollar in the wake of the Fitch downgrade and the US Treasury funding announcement only adds to our conviction that the Fed won’t need to hike interest rates further. These market moves in combination with higher volatility are tightening monetary conditions and will also put up mortgage rates and corporate borrowing costs. With the Federal Reserve Senior Loan Officer Opinion survey showing a further tightening of lending conditions with the prospect of more to come in 3Q, lending growth looks set to turn negative. This combination of higher borrowing costs and reduced credit availability is going to be a major headwind for economic activity that will help to get inflation down to 2% next year and keep it there.

Download

Download articleThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more