Mexico: Calibrating the “pause”

- 16 December 2020

- Mexico

Mexico stands alone among LATAM majors as a country with additional material scope for monetary policy easing, through rate cuts. And since last month’s policy meeting, when Banxico paused the cycle, policy drivers have turned more dovish, but we think it’s too soon for monetary authorities to abandon the new neutral guidance and cut again

We expect another pause this week

Mexico’s central bank (Banxico) surprised most investors in its last monetary policy meeting, on 12 November, by holding the policy rate steady at 4.25%. The pause did not signal the end of the easing cycle, which has accumulated 400bp in rate cuts. But, in our view, the pause suggested that some months would be needed for policymakers to reassess the economic outlook before adjusting the policy rate once again, if needed.

We expect the central bank to keep the policy rate unchanged at 4.25%

Consequently, even though since the November meeting inflation and FX dynamics have been more benign than expected, we agree with the majority of analysts that expect the bank to keep the policy rate unchanged at 4.25% tomorrow. Specifically, the bank may want to wait a bit longer to assess if recent CPI prints were not affected by temporary distortions related to year-end promotions.

A secondary reason for the central bank not to diverge from the guidance would be the impending change in its board composition. President Lopez Obrador’s (AMLO) third appointment for the five-member board, Galia Borja, takes office in January, after well-known hawk Javier Guzmán steps down.

AMLO’s two previous appointments added a marked dovish tilt to the board’s policy discussions and this third pick could be even more consequential, as it creates the possibility of a new dovish majority emerging in 2021.

Risk of rate cuts should intensify in 2021

As seen in the chart below, real rates remain unusually high in Mexico, when compared to its regional peers. This suggests that Banxico will likely be under pressure to consider additional rate cuts throughout 2021.

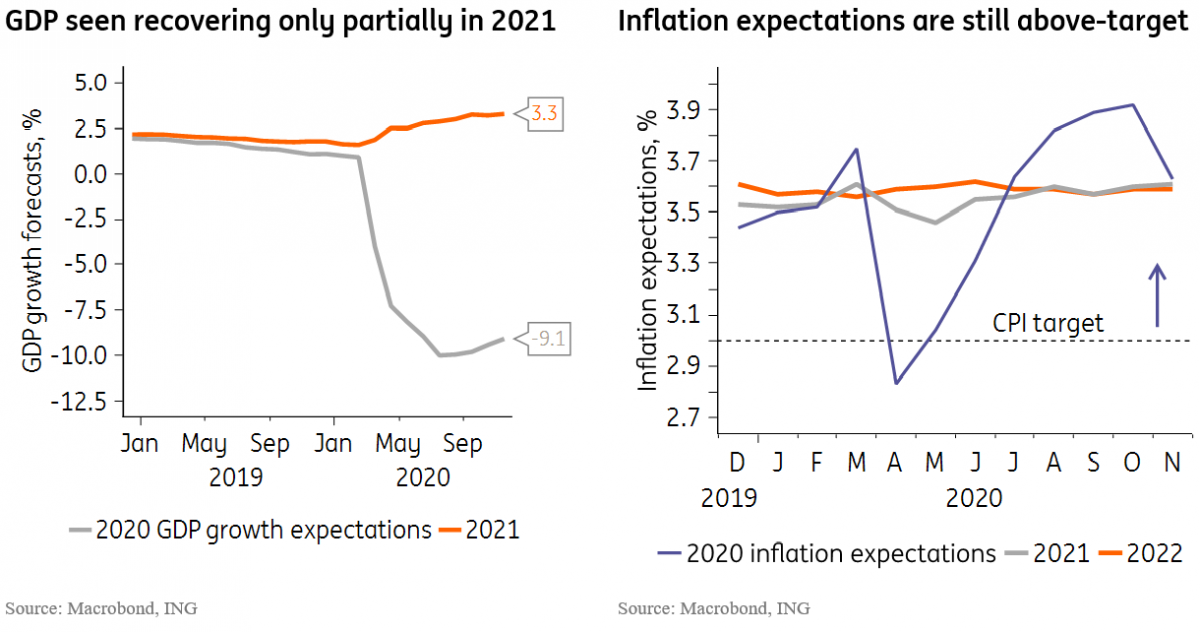

Much of the concern should focus on the poor economic growth prospects. Mexico will suffer one of the deepest recessions in LATAM this year and prospects for recovery are seen as more limited than elsewhere in the region, thanks in part to the unusually modest monetary and fiscal policy stimulus measures implemented to mitigate the Covid-19 pandemic.

In fact, judging by market expectations for GDP growth in the 2020-21 period, as seen in the chart below, GDP activity should recover just about one-third of the 2020 drop in 2021.

This wide output gap should act as a powerful argument for policymakers ease monetary conditions further in 2021.

The inflation outlook presents a more difficult balancing act for Banxico. Near-term dynamics have surprised to the downside and created a major correction in 2020 inflation expectations, as seen in the chart above. That correction did not spill-over into expectations for 2021-22 however, which have not fallen and remained materially above the 3% target.

This may reflect the fact that the inflation drop seen now is considered temporary, i.e. it is essentially the impact of the year-end discounts, which were more pronounced this year than in the past. Alternatively, and more concerning, it may reflect a lack of market credibility on the central bank’s commitment to the inflation target mandate.

Whatever the reason, the fact that inflation expectations have remained above the target has typically helped support a more cautious/hawkish policy stance. This hawkish bias may lose dominance in 2021, especially in our baseline scenario of weak economic activity and a relatively strong Mexican peso.

How low can the policy rate go?

Overall, it’s still too soon to determine where the new center-of-gravity will lie, in a hawkish-to-dovish spectrum, within Banxico’s board. The risk of a dovish shift has clearly increased, but we suspect the board will refrain from replicating the aggressive rate-cutting cycles seen throughout LATAM in recent quarters. This reflects the fact that we expect inflation dynamics to remain relatively sticky and higher than the 3% target.

In addition, Banxico’s preoccupation with local market stability also suggests that the bank will aim to keep a large Mexico/US interest rate differential to prevent FX outflows, as non-residents remain a large contingent of the local bond-holding universe.

As seen in the chart above, that differential has already dropped to 4.0%, or 175bp below the level prevailing in the recent 2017-20 period, which was marked by broad stability in non-resident holdings in the local government debt market. This is also still 125bp higher than the rate differential seen in 2014-16, which coincided with a wave of outflows. That level, equivalent to an overnight rate of 3.0% in Mexico today, should likely be seen, in our view, as the “effective lower bound” for policymakers.

There is room for additional cuts in 2021 from 4.25% to 3.5%

Ultimately, Banxico’s enduring concerns regarding a surge in capital outflows suggest that tolerance for additional cuts is likely to remain small, with the room for additional cuts in 2021 likely constrained to about 75bp, from 4.25% to 3.5%.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more