Mexico: A “perfect storm” scenario sets in

- 27 March 2020

- Mexico

Mexico may witness the largest economic contraction among its LATAM peers in 2020. A large GDP contraction, together with the financial difficulties faced by the state-owned oil company, PEMEX, would both elevate the risk of adverse credit rating actions, as already seen last night with S&P, and narrow the scope for counter-cyclical policies

Recession should deepen given the narrow scope for policy stimulus

Mexico stands out for its relatively mild policy response to the virus outbreak seen so far, which contrasts with our assessment that the Mexican economy is among the LATAM economies likely to be most affected by the ongoing crisis.

A high degree of uncertainty prevails, and much should depend on the duration of the crisis and how broadly the virus will spread and trigger lockdowns in the local economy. But judging by the contraction seen elsewhere, unless the coronavirus-related disruption in domestic activity is substantially lower in Mexico, the GDP contraction should draw parallels to the 5.3% drop seen in 2009, after the global financial crisis.

Among the factors that should contribute to a deeper contraction in Mexico are:

- The weaker starting point, with GDP in broad stagnation for almost two years now (see chart below),

- The most integrated manufacturing supply chain in LATAM, with the largest share of imports from China, and the stronger dependence on manufacturing exports, heavily concentrated on the US, implies greater vulnerability amid trade flow disruptions and a US recession. The rise in unemployment in the US is also contributing to lower income in Mexico as it reduces workers’ remittances, while travel restrictions could cause considerable damage to the service sector, especially tourism

- A relatively narrower scope to implement fiscal stimulus was made worse by the collapse in oil prices, which, despite the existing oil hedges, should place further stress on fiscal accounts and call into question the government’s PEMEX-centered growth strategy

- The tighter financial conditions and resistance of monetary authorities to shift monetary policy towards an expansionary stance

- As seen in the just-announced cancellation of a partly-built brewery, following another poorly-attended “public consultation”, the government continues to undermine business confidence and is being seen as adopting an adversarial attitude towards the private sector, adding further downside to capital investment that has already collapsed since it took office (see chart)

GDP growth and investment

Risk of further credit rating downgrades has increased sharply

All these factors add to a “perfect storm”-type scenario that is still hard to quantify, but that should have deep implications for Mexico’s macro outlook. Uncertainties involving eventual domestic policy responses to the crisis remain especially acute, but if recent signalling is any indication, Mexico’s policy stance should continue to stand out for being especially contractionary, when compared to its EM peers.

Overall, assuming that economic activity should be severely affected over the next two months, Mexico’s GDP should drop by 3-4% of GDP in 2020, down from -0.1% last year. Such a contraction, together with the financial difficulties faced by oil company PEMEX, would both elevate the risk of adverse credit rating actions and narrow the scope for counter-cyclical policies.

This reflects the fact that any effort to “rescue” PEMEX through tax cuts or cash injections would reduce the scope for other types of fiscal transfers. In addition, a credit rating downgrade would increase the risk of financial instability and increase the reluctance by monetary authorities to lower the policy rate, which is seen as an anchor for steady FX flows.

A downgrade by Moody’s seems like just a matter of time

Citing the twin shocks represented by the impact of the coronavirus on economic activity both in Mexico and in the US, and the collapse in oil prices, S&P already downgraded the sovereign and PEMEX yesterday, by one notch to BBB. S&P also maintained the negative outlook, citing economic policy uncertainty and the potential for PEMEX-related contingent liabilities.

A downgrade by Moody’s seems like just a matter of time and that would be especially consequential. Given that Fitch already ranks PEMEX below investment grade, in contrast to S&P's BBB, PEMEX would lose its investment-grade if Moody's announces a one-notch downgrade. This would inevitably add to the company’s financing difficulties and trigger some forced selling by investors who cannot hold junk-rated assets.

Risk of FX outflows to limit room for monetary stimulus

The Mexican central bank (Banxico) advanced its policy meeting by one week and cut the policy rate by 50bp last Friday, to 6.5%. Despite the ahead-of-schedule announcement, the decision was broadly in line with expectations.

Still, the decision and the policy statement that followed can easily be characterized as hesitant when compared to the stance adopted by other central banks in the region, especially given that one of the five board members voted for a smaller 25bp cut. The notably cautious monetary policy guidance contrasts with Mexico’s relatively high level of interest rates (see chart below), the sharp deterioration in the outlook for economic activity and the fact that the US Fed, which is an important reference point for Banxico, was considerably more aggressive by cutting the overnight rate by 150bp in March (see chart).

Mexico's high rates

Banxico Governor Alejandro Diaz de Leon was quoted justifying the caution by citing financial stability considerations, stating that Mexico was experiencing a currency shock and that the country is especially vulnerable to FX outflows. As seen in the chart above, non-resident holdings have been largely stable in Mexico over the past couple of years, which likely reflects the attractive rate differential offered by local bonds.

In our view, even if the currency’s performance improves in the near future, Banxico should stick to its play-it-safe strategy. In practice, we believe the bank should be a follower, and not attempt to surprise the market in its rate decisions.

In our view, market consensus should gradually consolidate around a terminal level for the policy rate in the 5-5.5% range, implying at least 100bp in additional rate cuts, that could be implemented in a relatively front-loaded fashion (i.e. starting with a 50bp cut in May, followed by 2-to-4 25bp adjustments in subsequent meetings).

Assuming that the US Fed keeps its overnight rate stable in the foreseeable future, this would imply a rate differential relative to the US in the 4.75-5.25% range, which lower than the 5.75% that prevailed in recent years but still high, especially when compared to its LATAM peers.

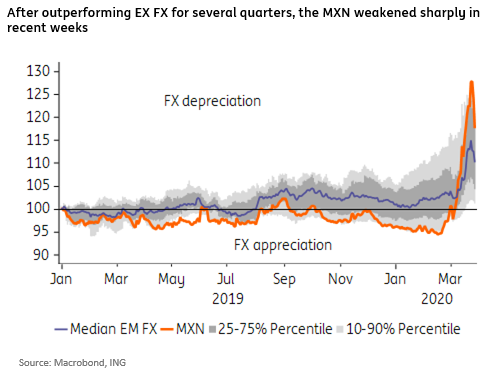

Weakness in Mexican peso

Monetary policy caution suggests that the MXN could, once again, outperform when risk appetite stabilises

We continue to be less sanguine about the peso’s medium-term outlook, given the ongoing deterioration in the macro outlook. But high rates could, once again, become an effective short-term anchor for the currency,

Overweight portfolio positioning was likely the chief factor behind the MXN's extreme sell-off seen in recent weeks. And given that investor positioning is probably much better adjusted by now, we do not discard a relatively quick reversal of the flight-to-quality shift that roiled the currency in recent weeks. That, of course, would depend on how fast global risk aversion abates.

In that case, the MXN could experience a relatively quick rally towards the 21-22 range.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Covid-19 crisis: What you need to know

- This bundle contains 14 Articles