Metals’ mettle

- 25 July 2017

Strength in copper and nickel has pushed the LME metals index to a three month high. Are aluminium cuts coming?

| 2,881 |

LME metals indexA three-month high |

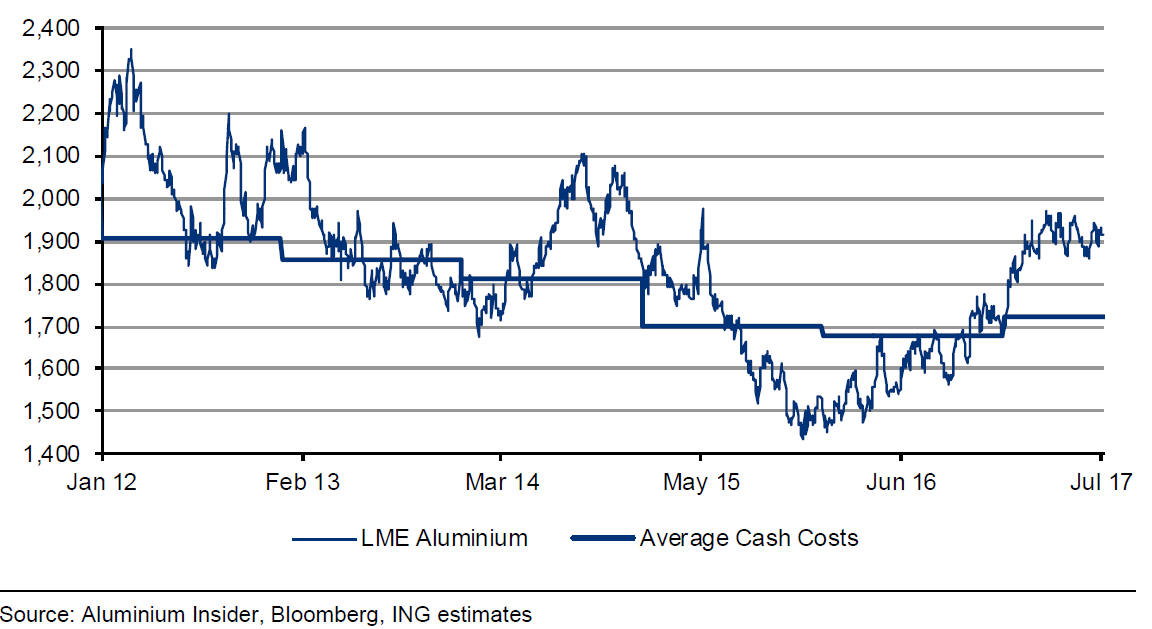

Aluminium output reaches record levels

LME aluminium has traded fairly sideways over the past few weeks, with talk of reducing Chinese smelting capacity offset by higher production. The generally stronger price environment has seen others planning to bring back idle capacity. There has been a lot of noise around Chinese capacity cuts but production data tells a different story. Figures from the International Aluminium Institute shows that Chinese aluminium output increased 9.1% YoY to a record high of 97.7kt/d in June 2017. This saw global aluminium production also reach a record 173kt/d, up 5.7% year-on-year. Cumulative global production over the first half of the year increased 6% YoY to 30.3mt, and given current prices, the trend is unlikely to be very different from the rest of the year.

Global aluminium profitability (USD/t)

The return of smelting capacity

Stronger aluminium prices have been enough of an incentive for producers to increase CapEx and restart idle capacity. Recently, Alcoa announced it would restart three of five pot-lines at its Warrick smelter in the US by the second quarter of next year.

Strengthening prices, stricter controls on aluminium imports and growing demand from industry have all supported the restart.

The Russian producer, Rusal, is also increasing capacity. With an average profit margin of above US$200/t, and a widening global deficit, there is enough incentive for producers to bring back capacity or resume previously shelved projects, something the Chinese producer Honqqiau is also now doing.

A tight market for zinc and lead

After strong gains in May to June, LME zinc has been trading flat at around USD 2,750/t over the past few weeks, while lead has fallen 2% MtD to USD 2,240/t. An early end to a strike at a mine in Peru along with producer pricing appears to have capped the market for the moment. China's refined zinc output increased by more than 13% MoM, just short of a record high of 562kt in November 2016.

Higher levels of producer pricing suggest there'll be less selling pressure coming from producers.

On 6 July, major zinc producer, Nyrstar indicated it had hedged nearly 70% of its zinc production for the first half of 2018. LME exchange data show that the gross short position of producers, merchants, processors and users in LME zinc increased to more than a two year high of 157,038 lots on 13 July 2017. That highlights the large amount of producer pricing that we have seen in the market as a result of stronger prices. A widening zinc deficit remains supportive for the market, however, and we continue to believe the stronger price environment should lead to mine capacity returning.

LME nickel prices (USD/t)

Nickel and tin extend gains

LME nickel has rallied around 9% from levels seen in early July, with improving demand from the steel sector. Tin prices have also extended gains on the back of low LME inventory. Indonesia is moving to boost nickel supply, not least by issuing an export permit to one company, Ceria Nugraha Indotoma. There are also increasing prospects of more supply from the Philippines.

Growing nickel supply from Indonesia and the Philippines is likely to keep a lid on nickel prices.

Increased exports from China could help refill LM tin warehouses, where inventories have been at their lowest levels since 1989. So, low tin stocks offer support in the short term but watch out for potentially higher Chinese output in the future. China has recently removed a 10% export duty on Chinese tin exports and those exports are now picking up.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more