Brexit: Five charts show the impact on the UK economy this year

- 8 March 2021

- United Kingdom

Expect a 3-4% hit to UK manufacturing output in January, though the jury's out on how much was solely down to Brexit-related disruption. The pandemic, stockpiling, and December's Covid-related port chaos will also have played their part. Still, data suggests the new trade frictions are still weighing on exporters and that's unlikely to change fast

GDP data will give a more concrete sense of Brexit-related strains

Friday’s UK GDP data is unlikely to be pretty. The imposition of a new strict nationwide lockdown at the start of January will inevitably see a sharp fall in monthly output as a range of consumer services sectors were shuttered. Meanwhile, higher Covid-19 prevalence and school closures meant staff shortages became more of an issue for businesses. All in, we think we’re looking at a 5% fall in January GDP.

None of that, admittedly, will come as much of a surprise. But Friday’s data is arguably still relevant because it will give us the first, concrete sense of the damage from the switch to new EU-UK trade terms at the start of the year. Despite a deluge of news reports detailing the difficulties faced by businesses, the data we’ve had so far has sent mixed signals on how bad it’s been on aggregate.

Here’s a brief look at what we know so far…

Traffic between the UK and EU was noticeably lower

Firstly, we know that the number of shipments moving across the UK-EU border fell sharply in January. That’s evident in lorry traffic data from Dover, obtained by the BBC, which shows it was considerably lower than normal through the first few weeks of the year. Anecdotal evidence also suggests many lorries heading back to the continent were empty (worth remembering here that around 85% of hauliers on the Dover-Calais route are EU-based).

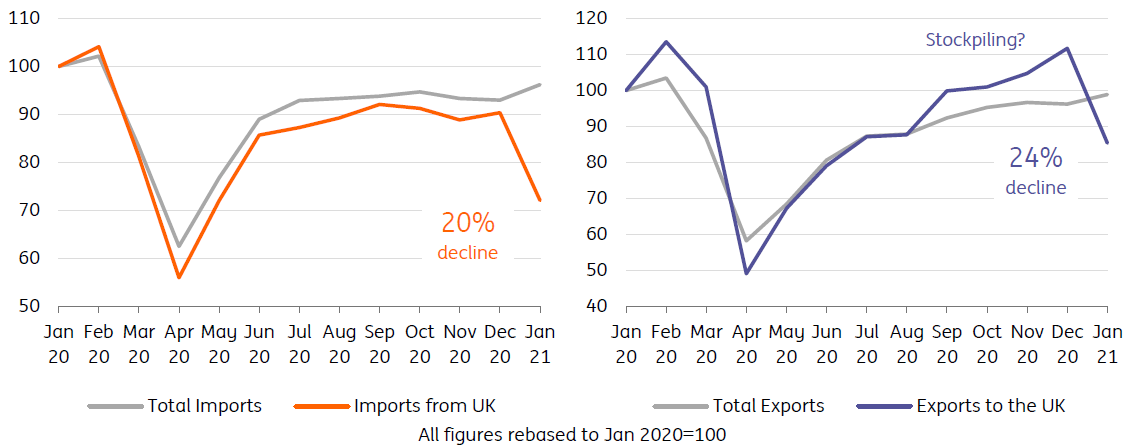

All of this tallies with trade data that has begun to emerge from Europe. French data shows a 20% decline in imports from the UK in January as trade frictions were introduced, while imports from the rest of the world increased. Data from the German and Italian statistics agencies suggest similarly dramatic falls.

French trade data shows a clear 'Brexit effect' in January

Manufacturing data shows less of an impact

However, the picture appears slightly less dramatic when looking at UK manufacturing indicators, which alongside agriculture, is arguably where much of the initial sector-specific impact would likely show.

The only real ‘hard’ data we’ve had so far is car production, which fell on a year-on-year basis, albeit perhaps not as sharply as might have been expected. When we seasonally-adjust monthly data from the Society of Motor Manufacturers and Traders (SMMT), we see around an 8% fall in car production from December to January. In the context of what is a fairly volatile dataset, this isn’t massive.

That sentiment is also reflected in the purchasing managers indices (PMIs) in both January and February. Both pointed to a sharp rise in supplier delivery times, but the impact on output was more limited. Indeed new orders have been fairly stable, all things considered.

Recent ONS business surveys also show no discernible deterioration in turnover in the manufacturing sector since the start of the year.

No discernible hit to manufacturing revenues in January

Brexit wasn't the only story affecting UK trade in January

Wrapping all of that together, what should we conclude?

Firstly, we think this implies we could see a 3-4% fall in January’s UK manufacturing output, though in practice this may prove to be an overestimate. Unfortunately we won't be able to gauge the impact on exports so clearly; the way the ONS measures these will change, which it says means the pre-2021 figures won’t be fully comparable with January’s data.

Secondly, all of the above emphasises that there was a lot going on besides Brexit in January. Data on French exports to the UK displays very clear signs of stockpiling during the latter months of 2020. That probably also explains the noticeable fall in cargo ship visits to UK ports, which came too early in January to be a reaction to disruption, and instead is probably indicative of firms taking a ‘wait and see’ approach given the long-telegraphed risk of border disruption.

Thirdly, the disruption at Dover/Calais ports in December, when French authorities effectively closed the border due to fears of the new Covid-19 variant, probably also had ripple effects into January. Car manufacturers were forced to pause production in mid-late December and that may be a relevant factor behind the January fall in production. Vehicle production is heavily reliant on ‘just in time’ deliveries across the channel.

Cargo/tanker visits to UK ports sank at the start of January compared to usual levels

Firms were less prepared than they'd have hoped

Nevertheless, there clearly was a 'Brexit effect', and the question is how much of this is temporary teething issues, and how much is going to prove longer lasting?

In practice, a bit of both. Firms were undoubtedly less prepared than they’d have wanted to be, not helped of course by the pandemic. Only around 1 in 10 manufacturers thought they were fully prepared back in mid-December, according to the ONS bi-weekly business survey.

Meanwhile, 31% of manufacturers and 40% of wholesalers/retailers said the changes weren’t relevant for their business. Partly this is because not all firms export/import, but we suspect this figure also includes firms who weren’t fully aware of the forthcoming challenges.

Retailers in particular may have been caught out by new rules of origin requirements, which govern whether a good has sufficient domestically-produced content to be eligible for tariff-free entry. Elsewhere, the problems were more acute for agriculture, where new veterinary hurdles and barriers to entry for certain produce caused significant issues.

1 in 10 manufacturers said they were prepared for the end of the transition period

Since early January though, some of the early sticking points appear to have been worked through. For instance, major hauliers have resumed UK-EU deliveries, having in some cases paused services in response to a significant percentage of consignments arriving without the correct paperwork.

That said, it's striking that roughly 10-20% of ‘exporting manufacturers’ have still been consistently reporting that they haven’t been able to export, according to the ONS (see chart below). That suggests that 'teething issues' only tell part of the story, and many firms are still grappling with the new (permanent) changes that have arisen as a result of the Trade and Cooperation Agreement (TCA).

In the short-term, things are, if anything, likely to get trickier. The UK will shortly begin phasing in full customs processes between April and July, potentially posing some additional challenges for UK imports. Meanwhile the political situation between the UK and EU remains fairly febrile. The UK’s unilateral decision to extend a grace period on export health certificates on goods destined for Northern Ireland has further eroded trust between governments.

While it’s not yet clear where the disagreement over the Northern Ireland protocol will take us, it’s a reminder that UK-EU relations are likely to remain tense, and in turn there’s a residual risk of parts of the TCA being suspended (eg via tariffs). If nothing else, it's hard to see the UK and EU agreeing to steps that would reduce some of the bureaucratic burden on firms in the longer-term.

10-20% of 'exporting manufacturers' haven't been able to export

Manufacturing should gradually recover through 2021, helped by new tax incentives

All of this will put pressure on the UK economy during the post-Covid recovery, and some firms will be forced to reorganise parts of their businesses to adapt to new changes. For some that will mean setting up European operations (eg warehousing), while others may be forced to make cuts to hiring and investment in response to higher costs (both the ONS and PMI surveys show a clear rise in input costs since the start of the year).

That said, we suspect manufacturing production will gradually recover through the next few months, helped along by new tax incentives. The government included a so-called 'superdeduction' in the latest budget, which allows businesses to offset 130% of the cost of new machinery/equipment against their tax bill. This offers a pretty big incentive to bring forward investment.

While the recovery in overall CapEx will still be fairly gradual, this measure should help inject a bit of life into investment after a very lacklustre period since the 2016 referendum.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Who wants to be a trillionaire?

- This bundle contains 6 Articles