Malaysia’s exports beat expectations, again

- 4 July 2019

- Malaysia

The second quarter of 2019 has shaped to be a better one for GDP growth than the first when growth bottomed in our view. Our baseline view is that growth remains firm and monetary policy will remain stable over the rest of the year

| 2.5% YoY |

Export growth in MaySecond consecutive gain |

| Better than expected | |

Electronics exports continue to outperform

Malaysia’s export growth not only remained in positive territory for a second consecutive month in May, but it was also better than consensus. Reported in local currency (Malaysian ringgit, or MYR) terms exports grew by 2.5% year-on-year in May, surpassing the consensus median of 2.2% growth and up from 1.1% growth in April.

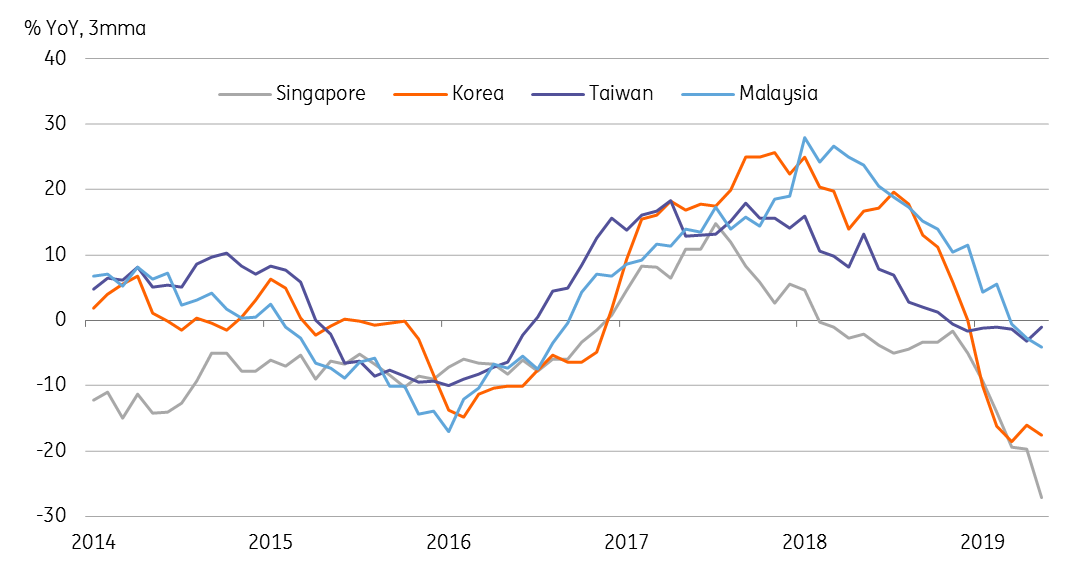

Electronics and electrical exports with a 38% weight in total exports, remained a key growth driver despite some slowdown in their rate of growth to 0.5% in May from 3.9% in April. This still represents a significant outperformance in the face of the ongoing electronics export weakness observed elsewhere in the region reflecting the global tech slump. This is also in stark contrast with Singapore, which is leading the global tech slump with a negative electronics export trend since end-2017. This could reflect Malaysia taking market share from Singapore. Even so, it’s hard to see Malaysia’s electronics exports continuing to buck the global downturn.

Malaysia outperforms in tech slump

Machinery and chemicals add to strength

Among other sectors that have been adding to overall export strength recently are machinery and appliances, and chemicals. Both posted strong growth of 15% and 8% respectively in May. Are these sectors also undergoing a structural shift in production to Malaysia from other parts of Asia, for example, Singapore, which is also strong in these sectors? Possibly. But the oil cluster (crude petroleum, liquefied natural gas, and petroleum products), another key export segment, has been weak and posted a sharp negative swing in growth in May (-13% from +8% in April).

Imports also grew in May albeit at less than half the pace (1.4%) of the 3.2% consensus estimate. The trade surplus narrowed to MYR 9.1bn from MYR 10.9bn in April. This puts the year-to-date surplus at MYR 56.8 billion, which is MYR 2.3bn more than in the same period of 2018.

Firmer growth warrants stable BNM policy

Based on this trade and also manufacturing data, we believe the second quarter has shaped up to deliver a better quarter for GDP growth than the first. Both exports and imports posted negative annual growth in the first quarter. Judging from April and May data, a return to positive trade growth looks more likely than not. And this will be reflected in firmer GDP growth through a better net trade contribution.

While we continue to believe that Malaysia’s GDP growth touched the cycle low at 4.5%YoY in 1Q19, we consider our 4.6% YoY growth forecast for 2Q at risk of more upside than downside surprise. We also believe that Malaysia's central bank (Bank Negara Malaysia - BNM) will assess economic risks as fairly balanced between growth and inflation and leave the overnight policy rate unchanged at 3.0% at the meeting next week (9 July).

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 5 July 2019

- This bundle contains 3 Articles