Malaysia: So far, so good

- 15 May 2018

- Malaysia

But it depends on what turn economic policies take in the first 100 days of the Mahathir administration

Although the muted market reaction to last week’s unexpected election outcome lessens our confidence in our forecast that the Malaysian ringgit (MYR) will breach through the 4.00 level against the US dollar in the near term, we are not rushing to revise it just yet.

| 5.6% |

Consensus forecast for 1Q18 GDP growthSlower than 5.9% in 4Q18 |

Steady GDP growth

Malaysia’s first key economic data under the new government- GDP for the first quarter of 2018- is due on Thursday, 17 May. Our forecast is 5.6% year-on-year growth, in line with the consensus. A modest slowdown from 5.9% in the previous quarter is largely due to the high base effect rather than any underlying economic weakness.

Malaysia’s exports outperformed the rest of Asia’s with 20% YoY growth in USD-terms in 1Q18. Industrial production growth, which is closely correlated with GDP growth, accelerated, too. We also think that elections spending supported the strength of domestic demand coming into 2018. The consumer-friendly policies under the new government should keep domestic demand supportive of GDP growth in the period ahead, even if the global trade war threatens exports.

We forecast full-year 2018 GDP growth of 5.5%, the low end of the official 5.5-6.0%.

Critical 100 days

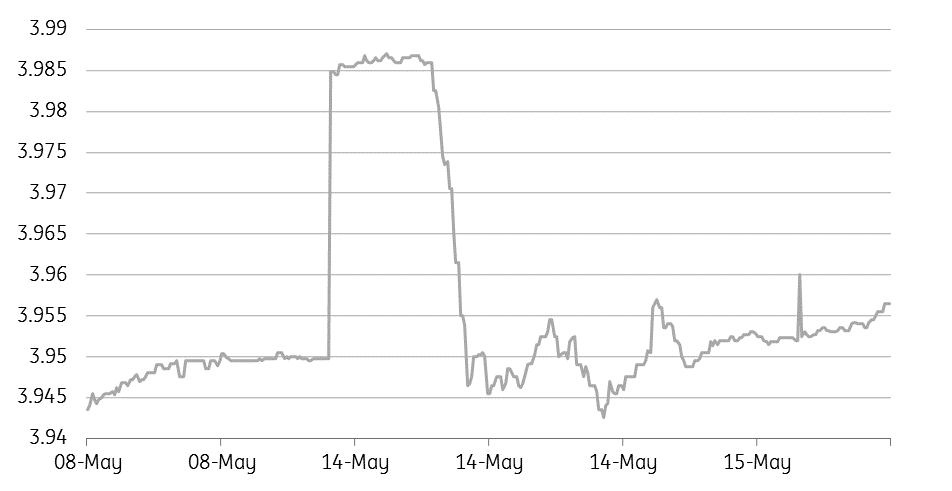

The markets outperformed expectations in the first two days of trading after the election holiday, although there was some weakness of the MYR (see figure) which can be attributed to broad USD strength.

The election holiday allowed market players time to digest the election surprise and adjust expectations of policies under the new administration. A smooth transition of power to Mahathir Bin Mohamad and his swift move to spearhead policy initiatives by getting his economic team (the “Council of Eminent People”) in place, deserve some credit for an almost unshattered market confidence. But at the same time, some differences with the coalition partners on initial cabinet appointments cannot be fully ignored.

The fundamentals are still there. When the fiscal conditions improve, this will be the final factor to have our ratings improved. – Zeti Akhtar Aziz, former central bank governor and a member of Mahathir’s economic team

The resilient markets, by no means, suggest there is no further uncertainty ahead. The big issue for the markets, however, is Mahathir’s plan to eliminate the Goods and Services Tax within the first 100 days of his rule. So far, there are no signs of Mahathir backtracking on this promise. Mahathir's economic team, which is comprised of people from a former finance minister and central banker to corporate leaders, is confident that scrapping the GST will not dent government revenues.

However, backtracking on economic reforms will certainly dent investor confidence, in our view. The current strong growth may help the economy absorb any GST revenue loss now, but that won't be the situation forever.

MYR per USD: A short-lived post-election spike

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 16 May 2018

- This bundle contains 5 Articles