Dutch retail sales growth will be more muted in 2023

- 9 December 2022

- Manufacturing, Construction and Retail The Netherlands

The pressure on consumer spending in early 2023 will lead to a further volume contraction in Dutch retail sales. But price increases will be lower next year (+3.5%), resulting in a turnover growth of about 2.5%

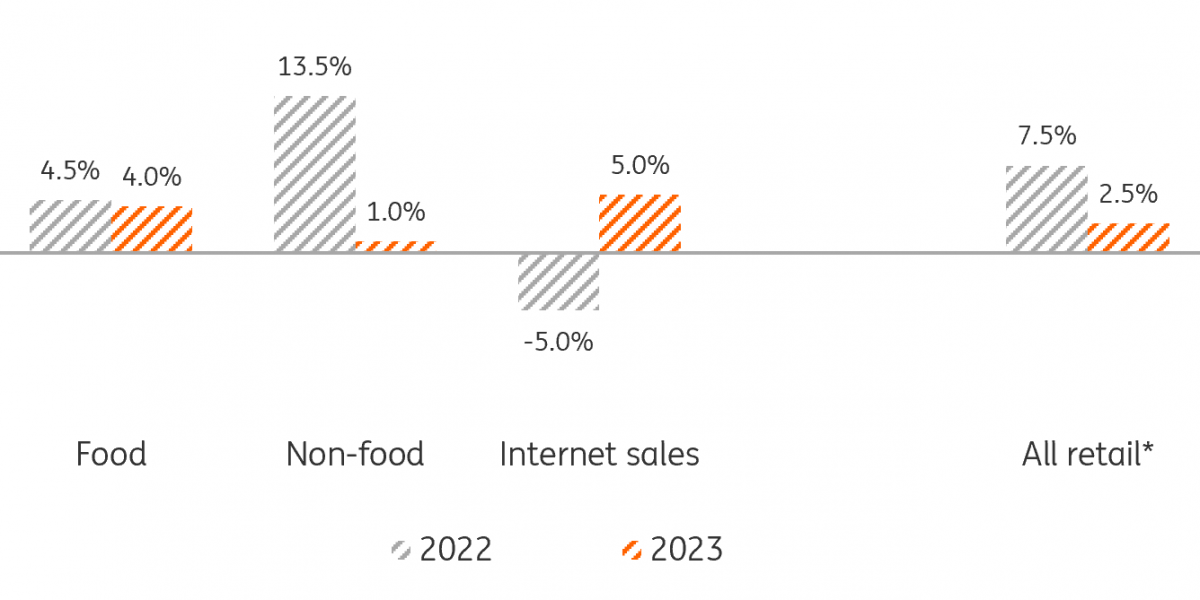

Lower turnover growth in the retail sector in 2023

Estimated sales growth in %, year-on-year

Consumer willingness to buy at rock bottom

Consumer confidence indicators have been in freefall since the last quarter of 2021, reaching the lowest levels since the start of these statistics in October 1986. Pessimism eased somewhat in November, but when it comes to making large purchases, consumers were as negative as they were in October. The decline in willingness to purchase since the fourth quarter of 2021 can be put down to the uptick in Covid-19 cases in the autumn of 2021, the subsequent reintroduction of restrictions, the war in Ukraine, and persistently high inflation (particularly in energy and food) this year.

Consumer confidence plummeted in 2022

Indicator of consumer willingness to buy, seasonally adjusted

Drop in the value of debit card transactions

ING's debit card data shows that the total value of transactions (debit card, ATM and iDEAL) have fallen since June 2022. The value of transactions was 1.5% lower in the third quarter than in the second. Price increases have prevented a further fall. The year-on-year decline in retail sales volumes was more than 3% in both the second and third quarters. Further contraction is expected in the fourth quarter. Positive market signals of Black Friday sales are hopeful, but may also be the result of pre-emptive Christmas and “Saint Nicholas” purchases, facilitated by the €190 energy compensation paid to many Dutch households. Rising energy bills are expected to dampen purchases in early 2023, despite the energy price cap.

Value of transactions in 3Q are 1.5% lower than in 2Q

Total value of domestic debit card payments, money withdrawals and iDEAL-payments as index (2Q22 = 100), seasonally adjusted

Limited growth recovery in online revenue in 2023

The lockdowns in 2020 and 2021 gave a huge boost to online sales, with high growth rates. Since Covid-19 restrictions eased in early 2022, some of those online purchases moved to shopping centres and high streets. This resulted in sales growth for physical stores in the first half of 2022 but a sales decrease in the online segment.

In the second half of 2022, there was a (limited) increase in turnover in both online shops and multichannel retailers. However, this is mainly due to price increases. On balance, the revenue reduction will be about 3% overall in 2022. In 2023, online revenue may continue to grow (by 5-10%), helped by sustained inflation. Thanks to investments in logistics and data analysis, a significant part of retail turnover has been transferred to the online channel. Only online-only stores are estimated to have an estimated €6bn higher turnover in 2022 than in 2019. A further shift to online seems feasible, as consumers increasingly value the convenience of online shopping and stock levels in stores are increasingly too low.

Decline in online sales in 2022 after high growth during lockdown years 2020/21 and a normalisation of sales growth in 2023

Growth in retail sales in %, year-on-year

Shop viability under increasing pressure

Prime locations in large cities were especially vulnerable during the Covid-19 lockdowns due to the loss of window shopping and the absence of (foreign) tourists. Some retailers managed to maintain profits through government support packages, tax deferrals and rental and banking arrangements. This minimised the number of bankruptcies. However, the difference between retail sectors is considerable. Food retail, drugstores and DIY stores performed better than clothing, footwear and electronics stores. Although the number of bankruptcies is still lower than pre-Covid, the number is increasing. The pressure on consumer spending and further cost increases, plus aid repayment obligations, will put pressure on the viability of an increasing number of shops compared to the period 2020-22.

More online shops than non-food stores

One in six physical Dutch stores disappeared in the period 2010-21, which is 14,000 stores. In 2021, the number of non-food shops remained stable thanks to Covid-19 support measures, but this is likely to be a one-off. In the last decade, for example, about 4,000 fashion and 1,500 shoe shops disappeared, half of toy stores (from 1,400 to 700) and a quarter of electronic stores (from 4,200 to 3,100). The number of supermarkets increased (+10%), particularly in 2021 (from 6,100 to 6,400). Since 2010, the number of online retailers has increased from 12,500 to more than 80,000. A large proportion of online retailers have minimal sales, but of course there are also some very large online businesses. In both 2020 and 2021, the number of online shops increased by almost 30%. In early 2022, for the first time, there were more online shops than physical non-food stores (22% more).

There are now more online stores than physical non-food shops

Number of non-food shops and online stores on 1 January 2022

Further volume contraction in food segment

The turnover of food retail is estimated to be 12.5% higher in 2022 than in 2019, an increase of around €5.5bn. More than €3bn of revenue growth was in the Covid-19 year of 2020 and €2bn in 2022 due to high inflation. However, since mid-2021 there has been a downward trend in volume development. Part of consumer spending has moved back from food retail to the hotel and catering industry, events and holidays. However, consumer prices in food retail substantially increased (+10% in the third quarter of 2022) to compensate for increased energy, procurement, transport and personnel costs. These cost items are also under upward pressure in 2023, while overall retail turnover will be dampened as consumers opt to shop in discount supermarkets. As a result, supermarkets, particularly smaller food specialists, will see their already-tight margins fall. A volume contraction of 1% is projected for 2023, resulting in an estimated 5% higher output prices leading to about 4% sales growth.

Growth in food retail sales in 2022/23 due to price increases

Turnover development in %, year-on-year

High turnover growth in non-food retail in 2022

The turnover trend in the non-food segment in the Covid-19 period 2020/21 was strongly determined by the restrictive measures for non-essential stores. For 2022, although an average of 7.5% growth in volume and 13.5% growth in turnover is expected for non-food retail, the difference between the first and second half of the year is huge. In the first quarter, there was a 40% increase in turnover for total non-food, rising to 70% for footwear and 90% for clothing stores. Growth rates normalised in the second quarter and shows lower volumes and sales in euros in the DIY and electronics segments compared to the same period in 2021. In the second half of the year, sales continued to be under pressure, as shown by ING debit card data.

Decrease mainly for non-essential consumer purchases

Change in transaction value, 3Q towards 2Q, seasonally adjusted

Downturn is already underway and will continue in 2023

In the third quarter, the transaction value in the fashion, furnishings and electronics retail segments was lower than in the second quarter, ranging from -1% for electronics stores to -6% for fashion (ING payments data via iDEAL). On the other hand, there are also increases, namely for spending in the food retail sector and in drugstores. The latter segment was identified as essential stores during lockdowns but continue to do well, thanks in part to the high sales of self-testing. CBS figures also show that non-food retail is struggling. In the second half of 2022, volume and turnover growth is expected to be significantly lower than in the first half of the year. In furniture and electronics segments, there is even a contraction. Thanks to widespread price increases, there is still some growth in turnover in the second half of the year, except for furniture and DIY shops. A further but lower price increase is also expected in 2023. However, the (mild) recession threatens to reduce volume, despite energy compensation schemes already in place. This is expected to result in minimal revenue growth for non-food retail (+1%).

Much lower sales growth in 2023 for non-food shops

Turnover development per sector, year-on-year

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more