Life after TLTROs: Bank liquidity and funding will be tested in 2024

- 18 October 2023

- Credit Financial Institutions

The final tranches of the European Central Bank’s targeted longer-term refinancing operations (TLTRO-III) will mature in the course of 2024. The existing liquidity buffers will likely be used to absorb part of the further LTRO runoff. We see a higher risk for increased bank bond issuance in particular for Italian and German banks

Eurozone banks see their liquidity coverage ratios drop in 2Q

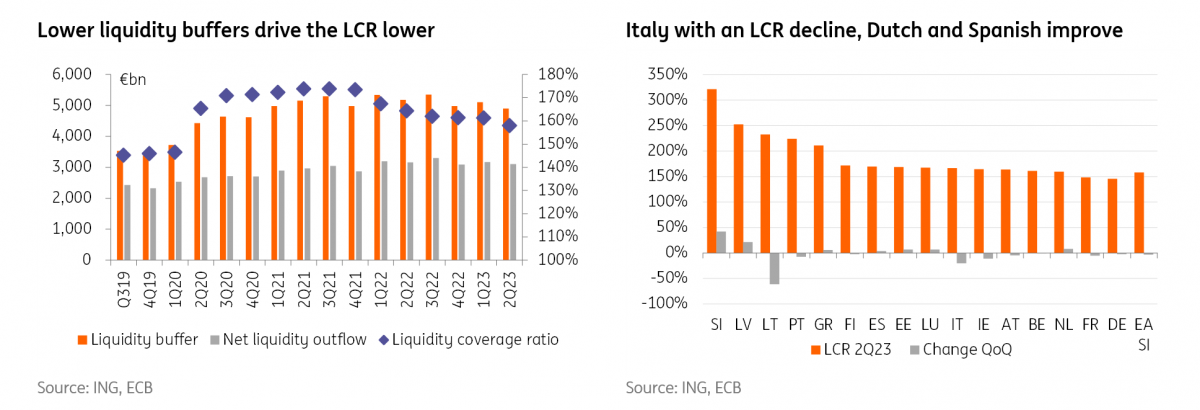

The liquidity position of eurozone banks weakened in the second quarter. The liquidity coverage ratio (LCR) of banks declined by 3ppt to 158% in 2Q, down from 161% in 1Q. The minimum requirement is set at 100%. The numbers are based on the ECB’s supervisory banking statistics for the second quarter, covering 110 significant institutions in the eurozone that are supervised by the ECB.

The LCR decline is mainly driven by the significantly lower Level 1 assets, forming the bulk of the €4.9tn aggregated liquidity buffer of banks. Banks have driven down their (adjusted) Level 1 assets by €235bn quarter-on-quarter. To offset just a small fraction of the reduction in (we think) cash and central bank deposits, banks have increased both their extremely high-quality Level 1 covered bond holdings (+€31bn QoQ) and Level 2 assets by +€30bn QoQ. However, both expected inflows and outflows fell, leading to a net reduction of €61bn for the net liquidity outflows over the quarter.

Based on bank balance sheet data, cash, cash balances at central banks and other demand deposits declined over the quarter by €303bn QoQ, while government bond holds increased by €34bn QoQ for the significant institutions. While these cash balances do include minimum required reserves held at the central bank, which are not eligible for Level 1 assets for the LCR purposes, the change in minimum reserve requirements has been very limited during this time period.

The decline in LCRs does not come as a surprise. The largest tranche of the TLTRO-III operation matured on 28 June. The outstanding LTROs halved in 2Q23 QoQ as banks paid back €503bn of funding to the ECB. We consider these repayments to be the major driver behind the lower liquidity buffers in 2Q as not all funds were refinanced.

The LCR remains well above the levels seen in 3Q19, i.e. prior to the allotment of the bulk of the TLTRO-III programme, when the LCR was 145% for eurozone banks.

Liquidity coverage ratios have turned lower

Country differences are substantial; Italy leads the decline

Country differences in the development of LCRs are considerable and mixed.

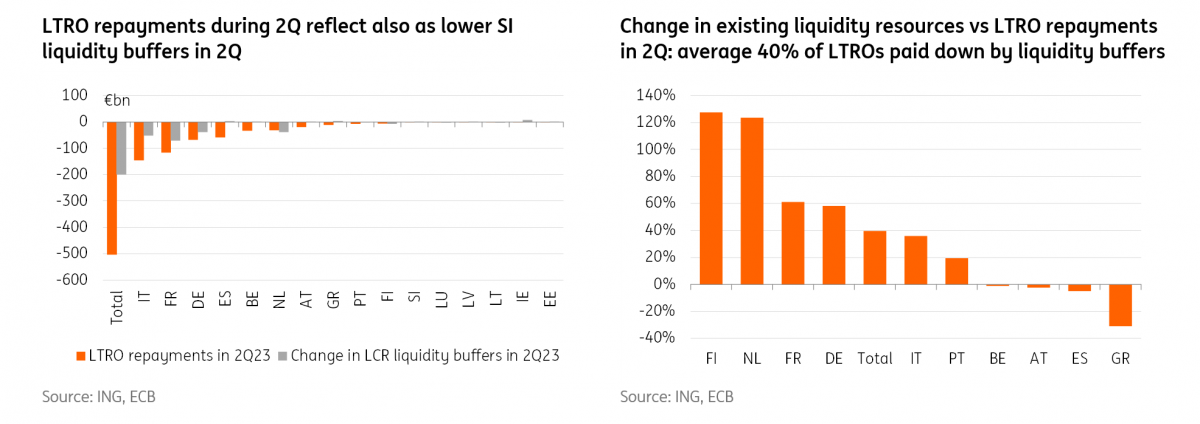

Among the larger countries, in particular, Italy shows a substantial LCR decline of 20ppt to 166% from 187%. The largest LTRO repayments in 2Q23 were made by banks in Italy (€146bn), a likely driver for the lower LCR of Italy's significant institutions. The impact on liquidity buffers though is perhaps less negative than it could have been. For the significant institutions, the aggregated liquidity buffers declined only by €52bn during the same time period.

We show a ratio of the change in liquidity buffers against the change in LTROs for selected countries in the chart below. For Italy, this share was 36%, not far off the eurozone average of 40%. This means that instead of driving down their liquidity buffers, Italian banks have sourced liquidity elsewhere, as their net outflows were more or less stable. It is good to note that as we do not yet have data for the less significant institutions for 2Q, this analysis includes only the larger banks for the liquidity buffers while the LTRO numbers include the whole banking system of the country.

Other countries that show a larger LCR decline include Ireland, with a decline of 11ppt to 164%. Irish banks largely paid down their LTROs already in 2022. The lower LCR ratio was instead driven by an increase in net outflows.

Portuguese, French and Austrian banks show an LCR decline in the range of 5-8%, while German, Finnish and Belgian banks reported more limited declines in their LCR ratios.

French banks paid back €117bn in LTROs in 2Q, while their liquidity buffers declined by €71bn with a ratio of the two just above 60%. The share of liquidity decline vs repayments for German banks is closely aligned with the French banks at 58%. French and German banks have thus perhaps utilised a larger share of their existing liquidity resources to pay back the ECB than their Italian counterparts, for example.

In the case of Austria, the aggregate liquidity buffers remained more or less unchanged, while the net outflows were somewhat higher, resulting in a lower LCR.

Not all LCR ratios declined, however. Dutch banks actually increased their LCR ratio by 8% QoQ to 160%. While the €39bn decline in liquidity buffers of large Dutch banks outpaced the repayments (€31bn) in LTROs in 2Q, the net LCR outflows declined by €41bn over the quarter, explaining the LCR improvement.

Also, Greek and Spanish banks have strengthened their LCR ratios over the quarter (by +6ppt to 211%, and +4ppt to 170%, respectively). Both reported higher liquidity buffers despite LTRO repayments, while for Spain the impact was further supported by lower net outflows.

The LTRO runoff has driven down liquidity buffers

Will the LTRO repayment activity continue to push bank liquidity lower or will banks replace the funds?

European banks still had some €598bn in longer-term refinancing operations outstanding as of 2Q23. The LTROs slightly increased (+€4bn) from end-June until end-August, as banks increased their drawings from the shorter-term LTROs.

Since then, the September 2023 TLTRO-III tranche has matured with €67bn in balances, on top of which banks have paid back early €34bn across the other tranches. This leaves outstanding drawings for TLTRO-III operations of €491bn maturing between December 2023 and December 2024 (see chart below). A large part of the funds redeem in March next year.

The largest users of the ECB funding operations are banks in Italy, France and Germany with outstanding LTRO drawings of €175bn, €146bn and €132bn, respectively, as of end-August.

The TLTRO-III programme matures in the course of 2024

Choosing between existing liquidity buffers and refinancing

The TLTRO refinancing choices of banks will continue to drive both the development of liquidity buffers and the euro-denominated bank bond supply in the course of 2024. The differences between countries and between banks are likely to remain substantial.

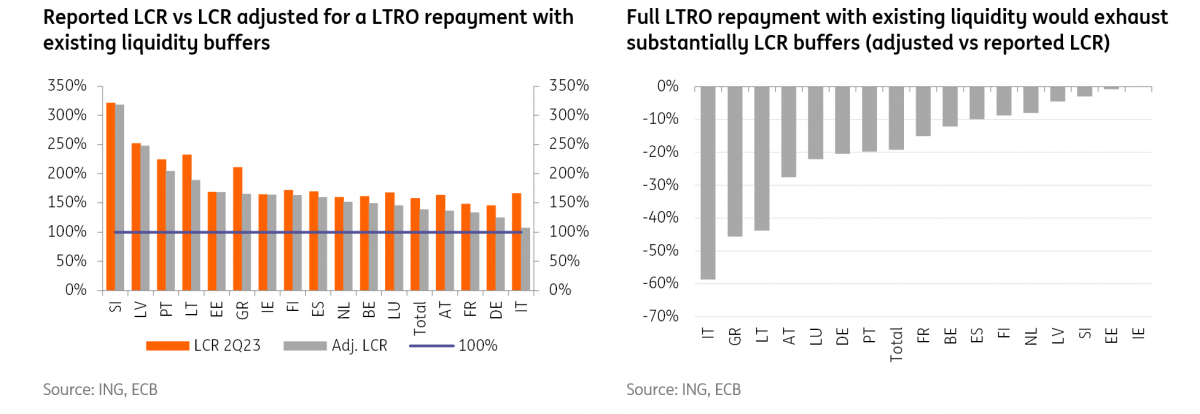

Alternative 1. Repayment of outstanding LTROs fully with existing liquidity buffers.

If banks were to fully repay all their LTRO drawings with their existing liquidity buffers, based on the aggregated numbers, the combined liquidity buffers would drop to €4.3tn and, assuming no change in net outflows, the LCR would adjust to a 19ppt lower level of 139%.

The LCR impact would be larger for banks in countries with larger LTRO drawings as shown in the charts below. Italian banks, in particular, would see a substantial impact on their liquidity buffers and on their LCR ratios due to their large share of existing LTRO funding, with the adjusted LCR dropping below 110% (see charts below).

A large negative impact would also be seen for Greece, Austria and Germany, among others. The German LCR would drop towards 125%. While being substantially lower than the 2Q23 level, this would still retain some headroom over the requirements. French, Spanish and Benelux banks would see a smaller negative impact. In the case of Greek banks, the LCR would remain at relatively high levels even adjusted for the repayments.

While we argue that most banks could pay down their LTROs with the existing buffers, the impact on LCR ratios would be too large for this to be a likely scenario in our view. We believe a strong enough buffer over minimum LCR requirements is extremely important for retaining trust in financial markets.

If banks were to pay back the LTROs with existing liquidity resources, the impact on liquidity coverage ratios would be substantial

Alternative 2. Depleting liquidity buffers towards the levels seen before the TLTRO-III was allocated.

LCR ratios have increased substantially, supported by the TLTRO-III programme. Banks could decide to lower their LCRs towards more normalised levels and use the slack for the LTRO runoff.

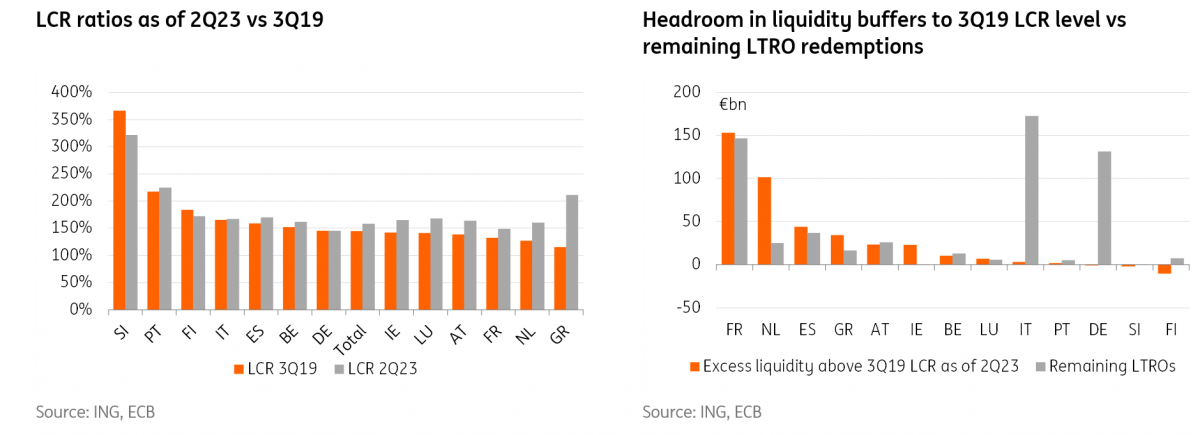

The very first tranche of TLTRO-III in September 2019 saw very limited demand of only €3bn. The second one, which settled in December 2019, was larger (€98bn). Since then, the LCR of eurozone banks has trended higher in tandem with the size of the TLTRO-III programme. We use the quarter before the first larger settlement as guidance for the more normal or desired LCR level. In 3Q19, systemic institutions had an LCR of 145%.

If you assume this 145% is a more normal level for the LCR, banks could lower their LCR ratios by some 13ppt. This would translate in the eurozone's larger banks having some €400bn in excess LCR liquidity buffers. Comparing this to the c.€600bn in LTROs that were outstanding at end-2Q would leave €200bn to be refinanced to retain their 3Q19 LCR levels.

As often is the case, the country differences are substantial. The chart below shows that not all banks have actually increased their LCR ratios despite their higher TLTRO drawings. In Finland and Slovenia, banks were running with lower LCR ratios in 2Q23 than in 3Q19. As Finland runs with lower LCR ratios as compared with the 3Q19 level, there is no “excess” above these 2019 levels to refinance the maturing LTROs of €8bn. We show the excess liquidity buffers ahead of 3Q19 levels against outstanding LTROs by country in the chart below.

In Germany, the LCR of significant institutions in 2Q23 was closely aligned with that in 3Q19. Therefore if banks in Germany wanted to retain their current 3Q19 LCR levels, they would need to refinance their €130bn outstanding LTROs to a large extent.

At the other end, in Greece, the LCR ratio of significant institutions in 2Q23 was almost double the level in 3Q19. If Greek banks were to return their LCR level to that in 3Q19, the banks could release up to €35bn in liquidity to fully redeem their €17bn LTROs. Therefore they could continue running with higher LCRs than they did in 2019 despite the LTRO runoff.

Banks in the Netherlands, Austria, Ireland and France have LCR ratios that are 15-30ppt higher than in 3Q19. Dutch banks would be able to comfortably redeem the remaining LTROs with existing liquidity buffers and remain ahead of 3Q19 LCR levels. Also, French banks would have room in their existing liquidity buffers to pay down LTROs and still just remain ahead of their LCR levels in 3Q19. In Austria, meanwhile, the outstanding LTROs would be a limited €2bn higher than the “excess above 3Q19” LCR buffers. Irish banks have already more or less fully repaid their LTROs.

In Italy, the LCR for significant institutions was some 1ppt higher in 2Q23 than in 3Q19. If these banks wanted to closely align their LCR ratios with 3Q19 levels, they would need to refinance the bulk of their outstanding €170bn LTROs to support their liquidity buffers. The gap would be the largest among countries. Portugal (€3bn), Belgium (€3bn) and Austria (€2bn) would also need to refinance part of their LTROs to keep their LCR at similar levels to 3Q19.

The TLTRO-III programme has inflated bank liquidity buffers

The potential impact from less significant institutions

The numbers above do not give a full picture of the existing liquidity buffers of the banking system, as they include only the largest banks in the area and exclude the less significant institutions. The LTRO data instead is for the total system.

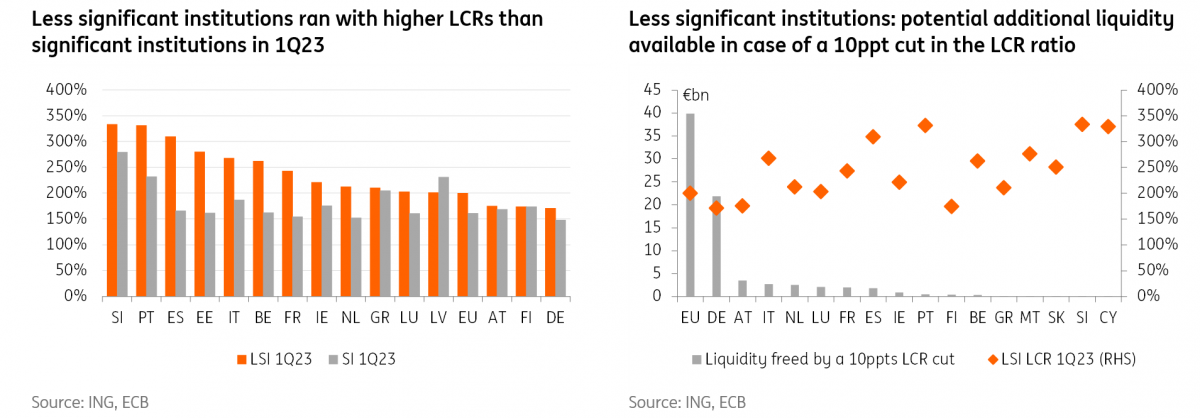

We would generally expect smaller banks to run with larger LCR ratios than larger banks due to, among others, weaker market access, less diversification and lower bond ratings.

The ECB is yet to publish the liquidity data for the less significant institutions for 2Q23. In 1Q23, these smaller banks carried LCR liquidity buffers of €800bn with an average LCR of 200%. This is a substantially higher LCR level than the average 161% for the larger banks in 1Q as shown in the chart below.

If these less significant banks were to lower their LCR ratios by 10ppt-20ppt, this would correspond to €40bn-€80bn in liquid assets that could be used to offset part of the LTRO runoff. The chart below shows that the country differences are very large, and around half of these funds would actually be in Germany. This data set is not available for the times before the TLTRO-III was allotted and as such we don’t include a comparison to the 3Q19 LCR levels for the smaller names.

Less significant institutions tend to run with higher liquidity buffers than significant institutions

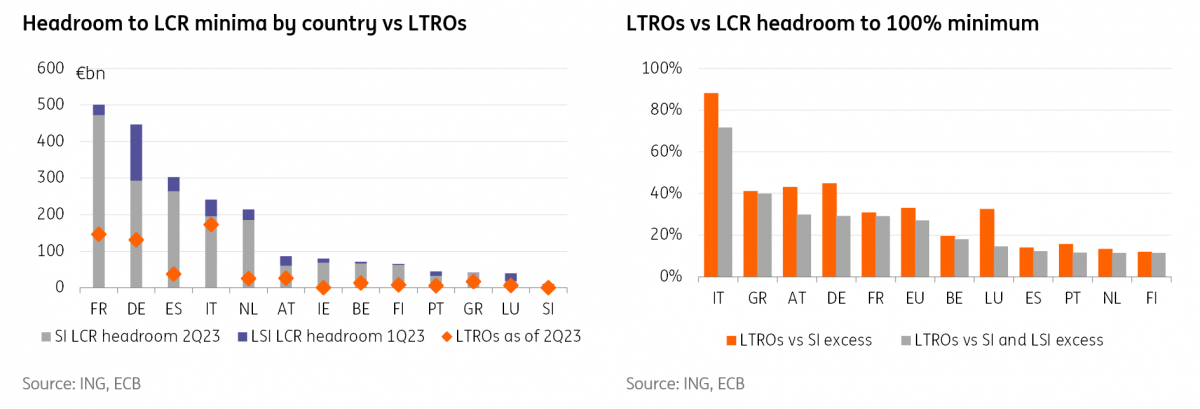

Banks have to meet an LCR level of 100%. The chart below shows the combined LCR liquidity headroom to this minimum LCR requirement for both significant institutions (as of 2Q) and less significant institutions (as of 1Q). In particular, in the case of German banks, smaller banks’ excess LCR liquidity buffers make a considerable difference to the country comparison. For other countries, the impact of adding smaller institutions makes less of a difference.

In Italy, paying back the LTROs with the existing buffers would absorb the highest share of excess liquidity buffers above the 100% LCR ratio when including the buffers in the less significant institutions, followed by Greece, Austria and Germany.

It is good to note that while these charts show the headroom to the minimum requirement of 100%, we don’t consider that any bank would actually want to see its liquidity buffers drop to a level that is very close to it. Instead, we would expect banks generally to target much higher levels and include a management buffer over the minimum requirement to retain market and client confidence.

Banks have substantial headroom above minimum LCR requirements

They may have enough to pay down the LTROs but keeping a strong enough management buffer is essential

So what's in store for 2024?

We expect banks to continue to partially deplete their still large liquidity buffers to redeem their outstanding LTRO drawings. Part of the drawings will likely be refinanced via bond markets to allow for longer maturity funding.

We think that banks with a higher LTRO-adjusted LCR ratio would be less likely to refinance their redeeming LTROs via other channels, including bond markets. Portuguese, Greek and Finnish banks would likely be among those that could retain relatively strong LCR levels despite their LTRO runoffs, and thus see less pressure to refinance their LTROs. The adjusted LCR in these countries would remain closer to, or above, 160% based on our analysis, leaving a relatively strong buffer above requirements. Nonetheless, Greek banks would see a substantial negative impact on their LCRs from paying down their LTROs with existing liquidity buffers. In these countries, bond supply will likely be driven by other factors such as bond redemptions, balance sheet development and the stage in loss absorption buffer build-up.

Lowering their LCR ratios towards levels seen prior to the TLTRO-III programme would allow many banks to absorb a substantial part but not all of their TLTRO maturities with existing resources. We believe that banks in France, Benelux, Austria and Spain could use a combination of drawing from existing liquidity resources and refinancing part of their LTROs via other sources including bond markets for the LTRO redemptions.

In Italy, existing liquidity resources would be severely hit if the LTROs were to run-off without refinancing. Italian LCR levels would drop to levels with a relatively tight margin above the minimum requirements and also clearly below the levels seen prior to the TLTRO-III allotment. Adding the liquidity buffers of the less significant institutions would only make a small difference.

Large German banks have not increased their LCR ratios during the TLTRO-III programme like banks in some other countries. While large German banks could absorb the LTRO impact with their existing buffers in our view, the headroom above minimum LCR requirements would drop substantially. Including the liquidity buffers in Germany's less significant institutions would change this picture a bit due to their more considerable size than in other jurisdictions.

As we think banks would rather exhibit stronger liquidity buffers, we would expect the bulk of the LTRO redemptions to be refinanced in Italy and also to an extent in Germany. Therefore we expect banks in these countries to be more likely to remain active in the bond markets to prepare for the expiry of the LTROs.

Alongside printing bonds, banks are likely to utilise other funding channels such as repos. In some cases, we may see a higher take-up in other central bank funding alternatives such as in the shorter LTROs or even MROs, in particular in an environment of more volatile market conditions. We see a risk that some stigma may be attached to increasing drawing funds from the central bank's shorter operations.

In light of the sluggish economic environment, tuning down lending also remains among the likely alternatives to offset part of the funding needs.

Several ECB speakers in the past couple of weeks have commented on the level of minimum reserve requirements (MRR). Increasing the MRR from the current 1% to a higher level such as 2% would depress banks’ Level 1 LCR liquidity buffers by a similar amount. In combination with the LTRO run-off, this would have a substantial impact on bank liquidity buffers, and we see a risk of unintended consequences in particular with a larger MRR increase. We wrote about the potential consequences earlier here. That being said, the ECB is still reviewing its monetary policy operations framework and the results of this are expected to be presented only in the spring of 2024. Any additional and more structural changes are unlikely to come before that.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Banks Outlook 2024: A world of higher for longer

- This bundle contains 7 Articles