Libor: Sonia, proceed as planned

- 25 February 2021

- Rates

The sterling market is making the most progress in weaning itself off Libor. Transitioning loans is a particular challenge and approaching target dates make it an important case study for other jurisdictions. Term Sonia rates are now live but the jury’s still out on which one will become market standard

Sterling markets showing the way

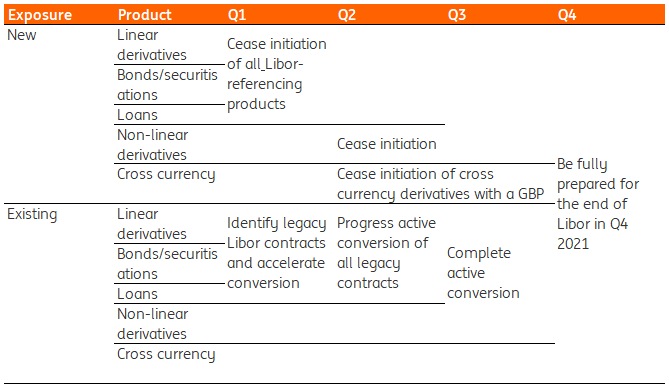

2021 is shaping up to be a decisive year in the Libor transition. Sterling markets are no exception. The working group (WG) on sterling risk-free reference rates has maintained a number of targets this year for linear and non-linear products, which you can see in the table below, They should all but seal the fate of most GBP Libor-referencing products.

2021 sterling Libor product targets

Tight deadlines on loans

One key challenge in the libor transition has been the speed at which the loan market can switch to using the new alternative Risk-FreeRates. With its near-term deadlines, the sterling loan market will no doubt be closely watched by market participants across multiple jurisdictions.

By the end of Q1 2021, the issuance of Libor-linked loans expiring after end-2021 must cease

In accordance with the WG’s roadmap, lenders should be in a position to offer non-Libor alternatives from the beginning of Q4 2020 and to include contractual conversion mechanisms to alternative RFRs in any new Libor-referencing loans. By the end of Q1 2021, the issuance of GBP Libor-linked loans expiring after the end of 2021 must cease. An important milestone has been reached since Q3 2020 and the publication of exposure drafts by the Loan Market Association (LMA), allowing for a more standardised approach.

After that date, the Bank of England’s schedule of haircuts on Libor-linked collateral start to apply: 10% from 1st April 1st 2021, rising to 40% on 1st September 2021, and to 100% on the final day of the year. This, however, is only directly relevant for firms participating in the BOE’s monetary operations.

According to the indicative timeline published by the WG’s loan enablers taskforce, the final stretch to the Q1 2021 deadline should be dedicated to system readiness to cope with the new conventions. And indeed, the minutes of the December 2020 WG meeting stress that the lack of system readiness is one factor holding back syndicated deals. As a result, and as international lenders are more focused on the transition in the USD market, according to the UK Finance Lender Readiness Survey, more progress was noted in the bilateral loan market.

Loan conventions

The Working Group has repeated that it expects Sonia compounded in arrears to become the standard for wholesale products, irrespective of a Term Sonia Reference rates (TSRR) being available since early 2021, and we'll look at that in a moment. The convention retained by the WG is for Sonia compounded in arrears with a 5 banking days lookback but without observational shift.

From the details of the transaction reported by the LMA, there appears to be a clear preference for using the WG’s preferred RFR convention, encouragingly.

Of the two methods identified by the WG to calculate credit adjustment spreads (CAS) in converting Libor loans to Sonia, the five-year median approach is the most consistent with the ISDA's methodology for derivative fallbacks. It is also the approach taken in many of the LMA's reported transactions.

Numerous factors are in play

As you'd expect, the majority of the new transactions referencing alternative RFR, containing a switch to alternative RFR or amendment of legacy loans to reference alternative RFR, was in sterling. It is hard to distinguish in the Loan Market Association list of relevant transactions a clear acceleration in the fourth quarter of 2020, however.

There are a number of factors in play here. Firstly, not all transactions are reported by the LMA. Secondly, of the two possible approaches available to counterparties, where either the complete provisions are already included and the switch occurs at the borrower’s request, or a rendezvous clauses where the detailed provisions still have to be agreed closer to the switch-date, and lenders’ consent is also necessary; we think the former is gaining in popularity.

The pipeline suggests a greater number of transactions referencing RFRs in the near future

We cannot exclude a degree of caution from borrowers as well. For instance, on facilities where the main currency of borrowing is EUR, while USD and GBP are optional currencies, it is sometimes simpler for the borrower to drop the optional currencies. Nevertheless, we see reasons for optimism. These transactions can have a long lead time and the pipeline suggests a greater number of transactions referencing RFRs in the near future.

Term Sonia: and the winner is…still unknown

Another milestone is the publication of the forward-looking term Sonia (TSRR) by two index providers, IBA and Refinitiv. These were approved for use on January 11th 2021. The conceptual differences between TSRR methodologies (summarised here) are limited in our opinion. Broadly, all rely on a myriad of contributions using primarily interdealer broker overnight index swaps (OIS) quotes and then relying on other data such as dealer to client quotes, and/or futures.

The conceptual differences between TSRR methodologies are limited

The WG has repeatedly said that the preferred alternative to Libor for wholesale markets is the backwards-looking Sonia compounded in arrears, so the introduction of Term Sonia should be a development mostly relevant for smaller types of borrowers in the loan markets, such as SME, retail, and wealth clients as well as for products that are offered on a discount basis (such as discounted trade finance products). A transparency draft of the proposed market standard for limited use of TSRR is due to be published in Q1 2021 by the FICC Market Standards Board, taking into account financial stability and conduct risk considerations.

TSRR: comparison of two contenders

We do see a benefit in the market building a critical mass in one TSRR

The question of which one of the above term Sonia becomes market standard remains open. We do however see the benefit in the market of building critical mass in one of them, rather than remaining fragmented between TSRR alternatives. One reason is that it would benefit the emergence of a basis market to hedge backwards-looking and forward-looking (TSRR) risks. But, in light of the limited differences between them, we suspect the Term Sonia benchmark which gathers the most interest at the start will stand the best chance.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Libor Transition: No please I insist, you go first

- This bundle contains 3 Articles