Latam FX Talking: The irrepressible Mexican peso

- 16 May 2023

- FX Talking

The Mexican peso continues to go from strength to strength. Banxico's policy of matching the Fed hiking cycle is really paying dividends. And the peso stands to be the prime beneficiary of 'nearshoring' trends. Elsewhere, investors are giving the new Brazilian administration the benefit of the doubt - but Brazilian real gains may prove temporary

Source: Shutterstock

USD/BRL: Investors give Lula the benefit of the doubt

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/BRL

4.904

|

Mildly Bullish | 5.10 | 5.20 | 5.20 | 5.20 |

- USD/BRL is starting to break under 5.00 – a move being accompanied by lower traded FX volatility and lower local sovereign yields. It seems that investors are giving the Lula administration the benefit of the doubt in that fiscal reforms can lead to lower sovereign risk and eventually rate cuts.

- So far, the central bank is pushing back against political pressure for rate cuts – still concerned by rising inflation expectations. Two new government nominations for positions on the central bank board could raise fears over political pressure to cut rates.

- We fear the pressure for slippage on the fiscal side is high and those looking for 12% implied yields should focus on MXN not BRL.

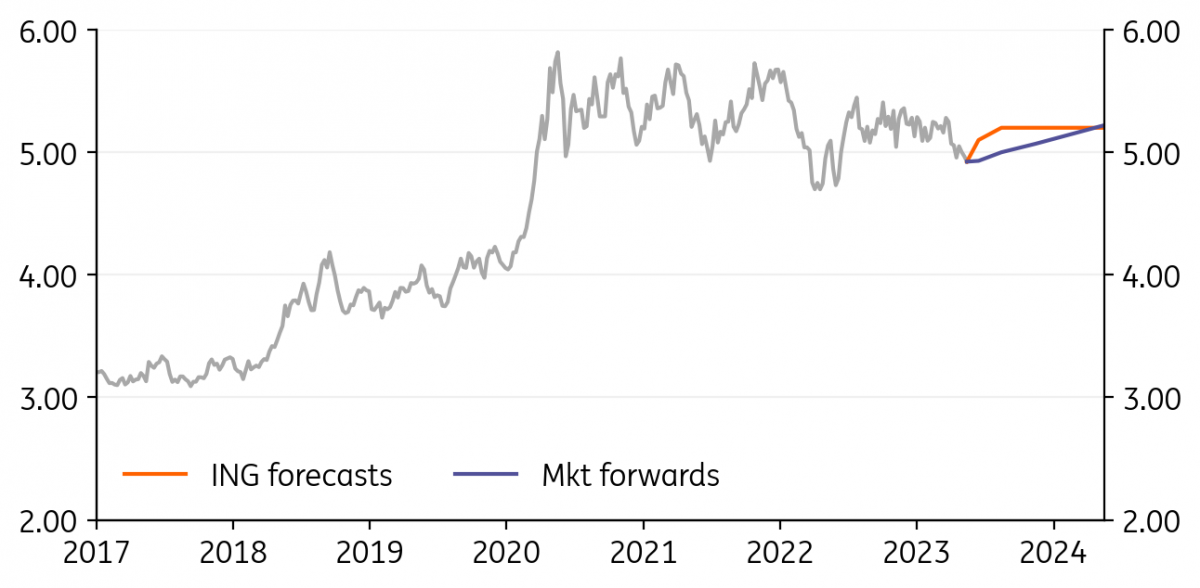

USD/MXN: Mexico’s peso the standout performer

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/MXN

17.576

|

Mildly Bullish | 18.00 | 17.75 | 17.75 | 17.00 |

- The Mexican peso is now pulling away as the best performing EMFX currency of 2023. Banxico’s maintenance of a 600-650bp spread above Fed rates has helped USD/MXN volatility levels fall and the peso stand out as the world’s preferred carry trade currency. Banxico meets 18 May and may deliver one last hike (to 11.50%) before pausing/stopping the tightening cycle.

- Remittances back to Mexico remain high at $5bn per month, but this year’s hot topic will remain ‘nearshoring’ and the promise of large FDI inflows into Mexico.

- Pressure is building for a USD/MXN to break below the 17.45 low of 2017 - and only long MXN positioning stands in the way.

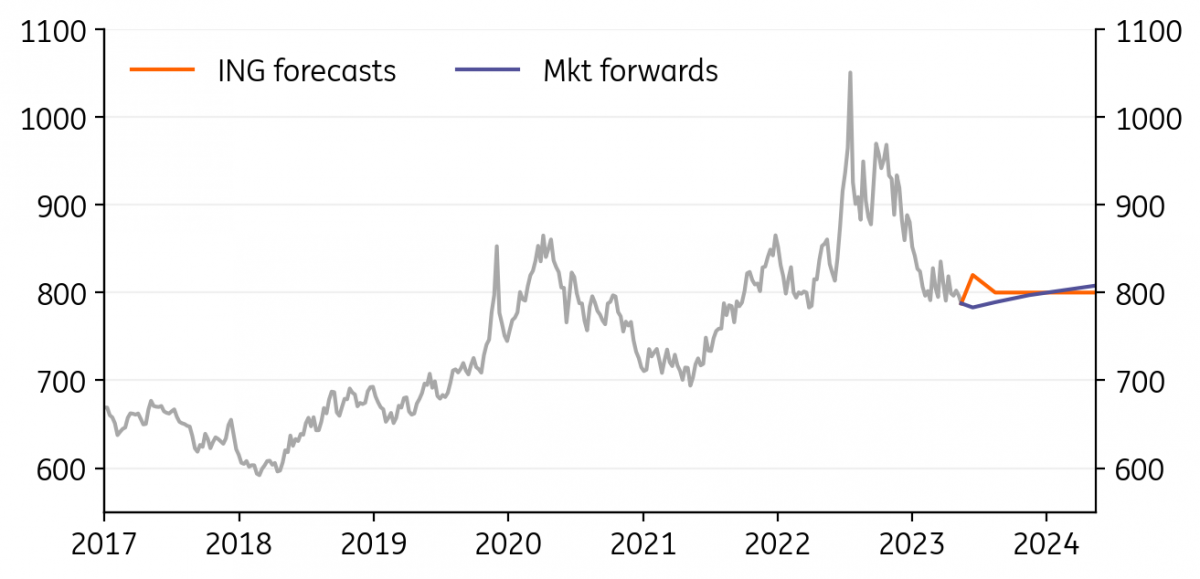

USD/CLP: Chilean peso will struggle to hold gains

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/CLP

779.45

|

Mildly Bullish | 820.00 | 800.00 | 800.00 | 800.00 |

- Institutional investors have made their minds up that rates have peaked and are now looking to receive rates around the world. Chile is no exception, where the market now prices 150bp of rate cuts over the next six months. Any interest to buy local currency bonds is likely to be unhedged because of high hedging costs.

- Yet we are not big fans of the CLP. The commodity environment looks mixed at best and we think investors will be wary that the government once again allows residents to raid pension pots – as they did during the pandemic. That didn’t end well for the CLP.

- We favour USD/CLP trading back over 800. FX reserve restocking may play a role here after Chile lost half of its reserves last year.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Bundle

15 May 2023

FX Talking: The rocky path to a weaker dollar

- This bundle contains 5 Articles

tba