Latam FX Talking: The beneficiary of emerging market portfolio flows

- 14 July 2023

- FX Talking

If this is the turn in the dollar cycle, it could mark the sweet spot for flows into emerging market asset markets – particularly EM local currency bond markets. Both Brazil and Mexico have relatively large weights in these benchmarks and their currencies could perform well as this asset class comes back into fashion

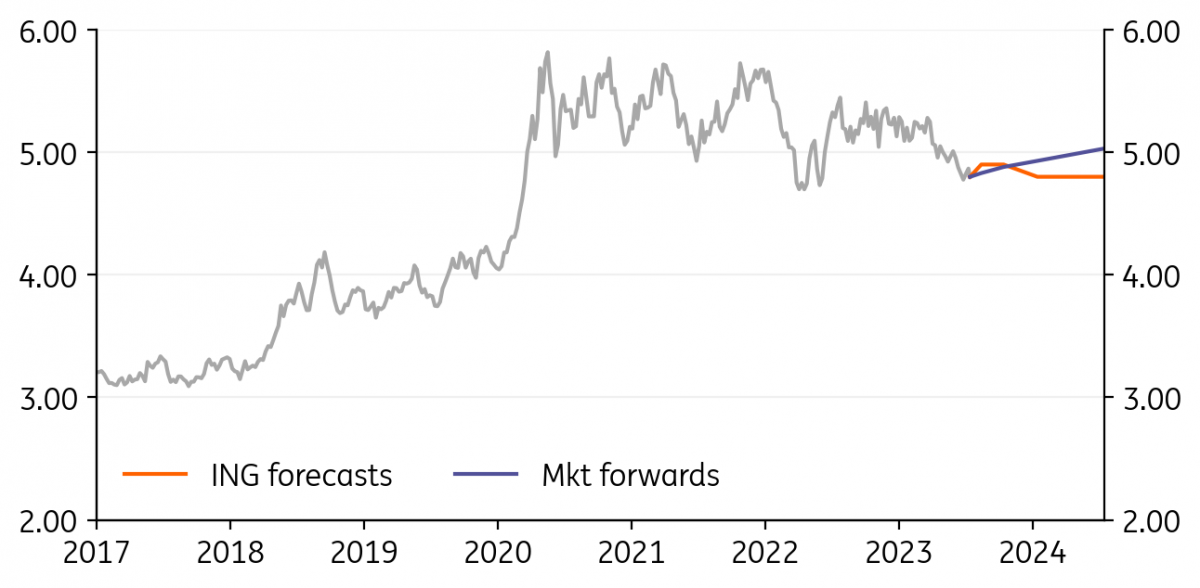

USD/BRL: Preparing for a major easing cycle

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/BRL

4.80

|

Mildly Bullish | 4.90 | 4.90 | 4.80 | 4.80 |

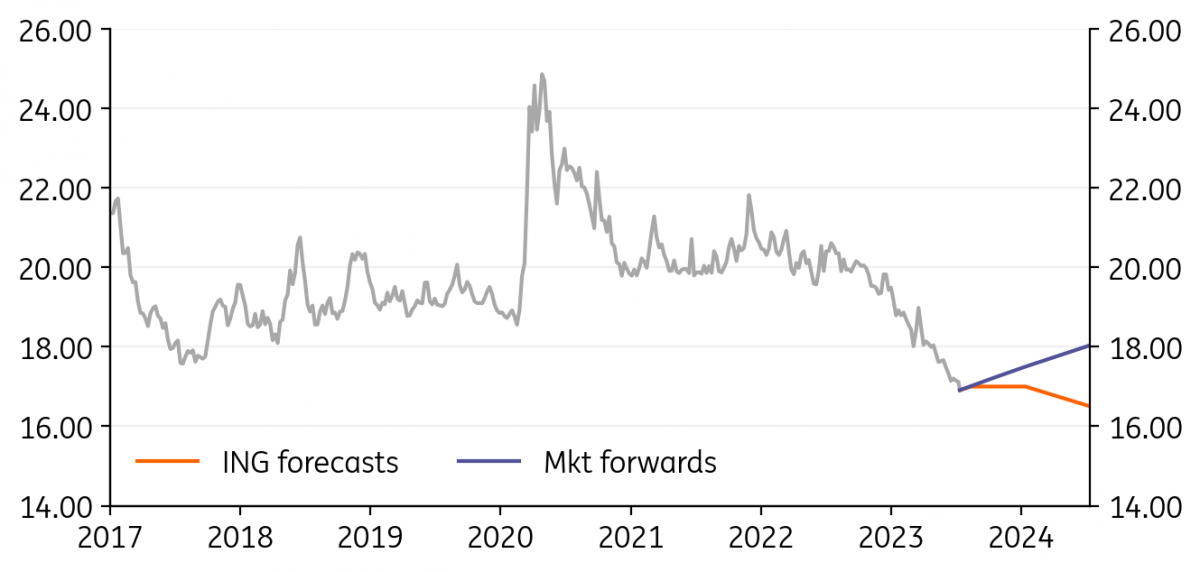

USD/MXN: Peso holds gains, political calendar drifts into view

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/MXN

16.91

|

Neutral | 17.00 | 17.00 | 17.00 | 16.50 |

The Mexican peso remains one of the top FX performers of the year and is only surpassed by the Colombian peso (offering 14.4% implied yields!). Investors like the high carry in Mexico, the well-run economy and the exposure to surprisingly strong US growth so far this year. Indeed, worker remittances back to Mexico hit a record $5.7bn high in May.

Banxico is promising an extended period of high rates (currently 11.25% policy rate), but will probably cut with the Fed in first quarter of 2024.

Politics looks the only shadow over the strong peso story, with Mexican elections next June and US elections next November. For the time being, however, expect MXN to hold gains.

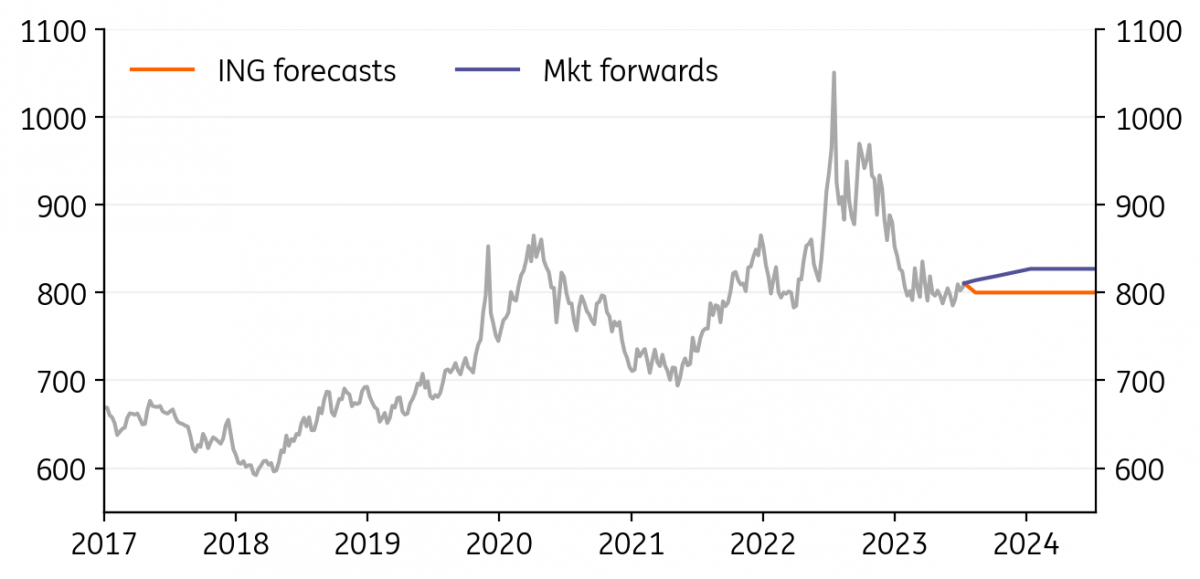

USD/CLP: Peso continues to lag

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/CLP

810.57

|

Neutral | 800.00 | 800.00 | 800.00 | 800.00 |

The Chilean peso is lagging the rally of its Latam peers. The fact that Chile could be the first of the big three in the region to cut rates may be no coincidence. Here June saw the central bank warn that the easing cycle could start in the ‘short term’. A 50-75bp rate cut is now expected at the 28 July rate meeting.

The central bank will cite inflation expectations anchored at 3% as the reason for the cut – even though core inflation is still 9% YoY. Chile may prove a test case for Latam FX and easing cycles.

Regarding Chile’s main export, copper – we see it at neutral $8300-8600/MT this year. And we think $/CLP stays near 800.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

FX Talking: The dollar’s break point

- This bundle contains 6 Articles

This month we are having to acknowledge the better prospects for the Brazilian real, where some welcome reforms and what should be the start of a significant easing cycle are improving the outlook for Brazilian asset markets. On the former, the new fiscal framework and what seems to be consumption tax reforms are supporting the narrowing in Brazil’s sovereign risk premium.

Low inflation, now below the central bank’s 2023 inflation target, is also raising expectations that BACEN can cut the Selic rate aggressively. A first cut in the 13.75% rate is expected in August, with around 400bp of easing expected over the next year.

If we are right with the dollar turning lower later this year, it looks like BRL can outperform the steep forwards curve.