Latam FX Talking: A few clouds on the horizon

- 15 June

- FX Talking Brazil Mexico

Latin America has been viewed as a bastion of FX stability so far this year. Yet a few wrinkles are emerging – from politics in Brazil to a trade re-negotiation in Mexico to the outlook for Chile’s copper industry. Even so, Brazil's status as a high-yielding energy exporter should protect the real, and we remain bullish here

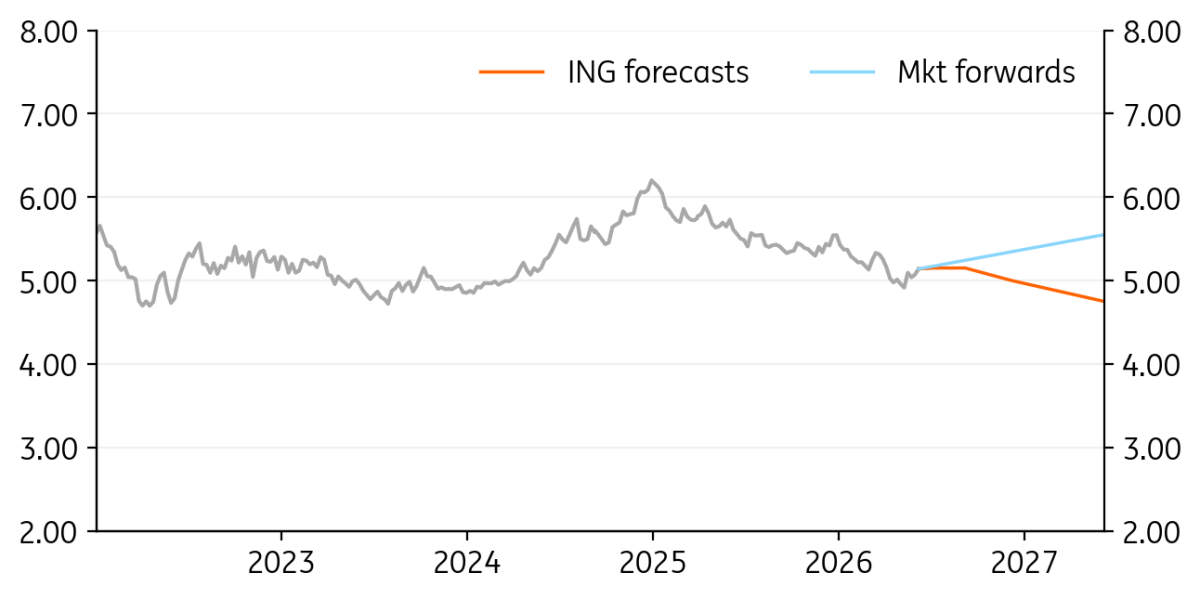

USD/BRL: A little underperformance comes through

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/BRL

5.10

|

Neutral | 5.15 | 5.15 | 5.00 | 4.75 |

- We’ve started to see some underperformance in the real over the last five to 10 days, driven mostly by local interest rates. Markets are now pricing roughly 125bp of tightening over the next year, which looks too aggressive to us.

- Fears of economic overheating — stoked by Brazil’s strong 1.1% quarter-on-quarter GDP print in 1Q and the Lula administration’s loose fiscal stance — helped drive the recent rates‑led sell‑off. Additionally, Lula pulling ahead in presidential polling seems to have weighed on BRL.

- But with 13% implied yields, the BRL remains an expensive sell. And ultimately, high yields, Brazil’s energy exporter status and perhaps high crop yields on El Niño should keep BRL supported.

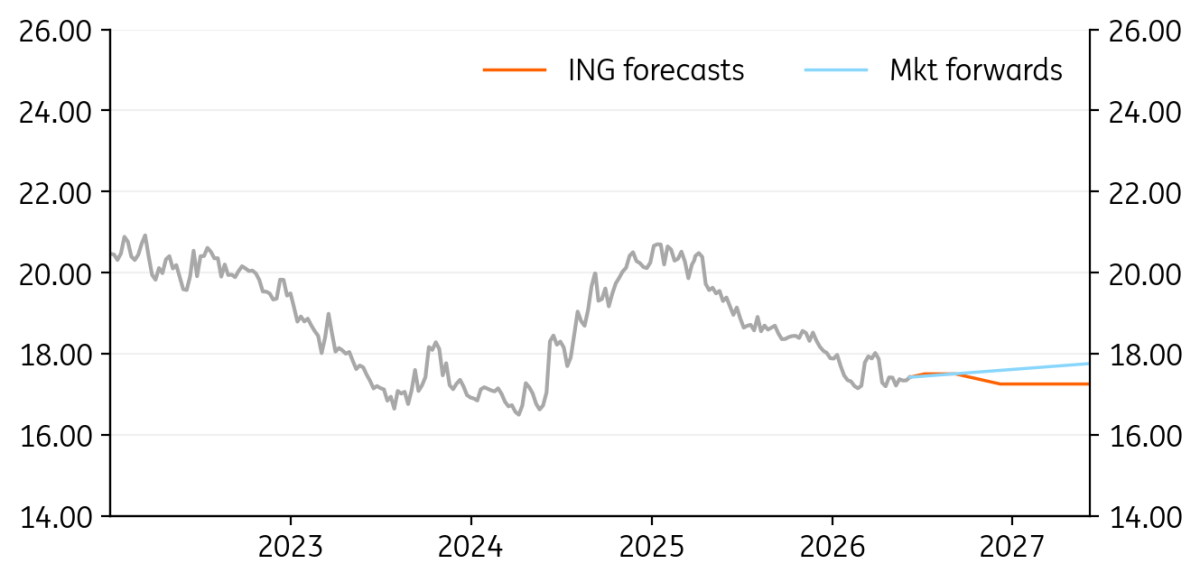

USD/MXN: MXN interest rate protection is a little lean

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/MXN

17.21

|

Mildly Bullish | 17.50 | 17.50 | 17.25 | 17.25 |

- The peso has been performing relatively well during this corrective period in risk assets. A 2.5% correction is not a bad outcome for a high-beta EM currency. The next couple of months could be a difficult period for EM assets; we see potential MXN weakness. And after a two-year, 475bp Banxico easing cycle, the Mexican policy spread over the US is now a lean 275bp. This is close to the lows over the last decade.

- The USMCA re-negotiation looks set to drag on, with the US pushing for stricter rules of origin. This uncertainty can weigh on the market.

- We don’t think Banxico wants USD/MXN to trade too far under 17.00, which in any case looks unlikely this summer.

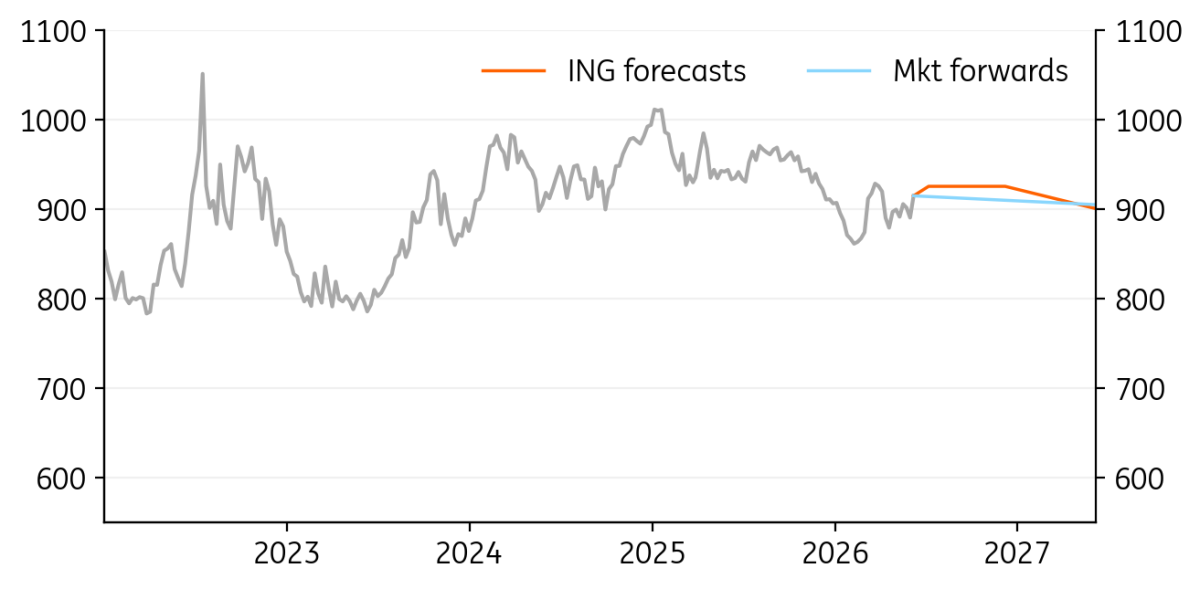

USD/CLP: Copper story could prove problematical

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/CLP

905.03

|

Mildly Bullish | 925.00 | 925.00 | 925.00 | 900.00 |

- Higher US rates have pushed USD/CLP toward the top of its broad 850–950 range. Another sharp rise in energy prices in the coming months would be particularly unwelcome for Chile. We’re a little worried about Chile’s copper production later this year, where more limited access to sulphuric acid, linked to Middle East–related supply disruptions, could hit activity.

- We’re also waiting to hear about US tariffs on refined copper products – a decision is due by the end of June. A delay or a tariff could keep copper prices bid, while no tariffs could see copper prices give back some of their recent gains.

- Expect USD/CLP to continue trading in an 850-950 range, with a top-side bias given the current strengthening dollar story.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Bundle

15 June

FX Talking: Dollar downturn delayed

- This bundle contains 6 Articles