Korea: Riding the crest of wave #2

- 8 September 2020

- South Korea

Relatively speaking, Korea has not had a bad pandemic, but the recent resurgence in cases in Seoul shows that until a vaccine becomes widespread, the threat from Covid-19 will remain an impediment to business as usual, and with Korea’s internationally facing industries, global weakness will remain a drag on growth

Covid-19 - if only every country had been as good as Korea

If every country around the world had been as fast-acting as Korea during the early stages of the Covid-19 pandemic, the whole nature of this health crisis might have looked a lot different. Indeed, it might well not have been a pandemic. Fast and comprehensive test, trace and isolating practices, helped by Korea’s sophisticated and growing bio-medical industry have made a big difference.

But even this has not been enough, and yet another controversial church has been found at the centre of the latest cluster of cases, requiring the government to request exposed individuals to adhere to a quarantine.

South Korea, Covid-19 total cumulative and 7-D average of new cases

For a country with a population of 55 million, the current 7-day moving average of daily cases of a little over 300 and total confirmed cases of just over 20,000, Korea has had fewer confirmed cases than much smaller countries, such as Ireland, Nepal, and Oman.

In spite of the recent setbacks, thanks to its swift and efficient response, Korea has still not needed to impose a mandatory national lockdown, and the domestic economy has certainly benefited from a less restricted environment than most of its neighbours, competitors, and key export markets.

Factors that may have played a role in Korea’s successful approach to Covid-19, and which other countries may wish to emulate, may, in fact, stem from the experience of its disappointing response in 2015 to an outbreak of MErs (Middle East respiratory syndrome), a general willingness to wear masks (in common use thanks to air pollution), and public cooperation with government safe-distancing advice.

For a country with a population of 55 million, the current 7-day moving average of daily cases of a little over 300 and total confirmed cases of just over 20,000, Korea has had fewer confirmed cases than much smaller countries, such as Ireland, Nepal, and Oman

The MErs experience also boosted the expansion of Korea’s biomedical industry, and within two weeks of the first case of Covid-19, thousands of testing kits were being shipped a day up to its peak of 100,000 kits per day. Preparations for large scale testing quickly got off the ground with public-private partnerships quickly scaling up testing capabilities which coupled with 600 screening centres (including drive-through testing), enabled the country to perform more than 300,000 tests by late March, more than 40 times the number the US had performed at the same time.

Another source of success was the support given to Covid-19 patients, creating isolation wards for those experiencing symptoms, while supporting self-isolating individuals with food and toiletries and twice-daily check-ups from health officers.

Epidemic Intelligence Service (EIS) officers were supported with the following information to help contact tracing:

- Facility visits including pharmacies and medical facilities

- GPS data from cell phones

- Credit card transaction logs

- Closed-circuit TV

Not all of this will be replicable for all countries. For example, it helps that South Koreans have been so ready to follow social distancing guidelines, wherein other countries, this has led to protests and civil disobedience. Widespread smartphone use also helps.

Nonetheless, even though providing this information comes at a cost in terms of personal privacy, this is a price Korea has felt worth paying. And given the relative economic performance of Korea compared to other countries in the region, the trade-off seems to have paid off.

Economic growth - could have been a lot worse

In late January, Korea confirmed its first case of Covid-19, making it one of the first countries in Asia to register a case after China.

Consequently, Korea experienced the negative consequences of Covid-19 earlier in 1Q20 than many other countries, for whom the pandemic and the associated lockdowns and other measures were not felt until much later in the quarter. So when comparing the growth performance, we can’t just compare recent growth rates but should look at the cumulative impact on the economy over 1Q20 and 2Q20.

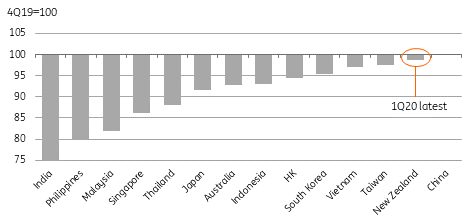

If we look across the whole region, for those economies that have released 2Q20 GDP data, Korea ranks towards the higher end, along with Taiwan, regional darling, Vietnam, and of course China, which has, apparently, recovered all the growth it lost in 1Q20 (which seems a little hard to swallow, but those are the official figures).

Cumulative Asian GDP loss (gain) from Covid-19 (4Q2019 = 100)

After contracting by 1.3%QoQ in 1Q20, and then a further modest decline of 2.7%QoQ in 2Q20, the Korean economy has contracted by less than five percentage points in cumulative terms, which not only compares favourably locally, but also looks good in G-7 terms (on the same basis, Japan’s GDP is down almost 9pp, the US has contracted by more than 10pp, and the Eurozone by more than 15pp). 3Q20 GDP should show some recovery as the second wave is contained and social distancing can be cautiously relaxed again.

The economy has contracted by less than five percentage points in cumulative terms, which not only compares favourably locally, but also looks good in G-7 terms

The Bank of Korea (BoK) monthly surveys of activity showed that the manufacturing sector bottomed in June this year, and has improved in each of the subsequent months, though remains weak overall, and is still operating well below pre-Covid levels, thanks to weak overseas demand and soft export demand.

It is a similar story for the non-manufacturing sector, though it troughed earlier, in May, and has been more robust throughout the pandemic, reflecting the relative outperformance of Korean domestic demand to its key export markets.

On the assumption that we continue to see further, slow improvements, and further incremental easing of restrictions in movement and activity both in Korea and overseas over the coming months and quarters, we expect a further recovery of lost output, though this does not bring GDP back to pre-Covid 4Q19 GDP levels until around or even after 4Q21.

In short, Covid-19 will have wiped off two years of GDP growth.

Impact of Covid-19 on Korean GDP in levels, 4Q 2019 = 100

This is a heavy price to pay for the virus, but it is not as heavy as most of its Asian peers.

Thanks to Korea’s very strong test, trace and isolate procedures, the domestic economy is less restricted than in many nearby economies. But the constraints on further upside improvements are similar – namely the risk of greater and too rapid re-opening, and the ongoing restrictions in less well-managed economies overseas, keeping export demand subdued.

Unfortunately, there is very little that the Korean government can do about the governance of some of its key export markets.

Domestic economy - better than elsewhere

The success of Korea’s pandemic response has spared the labour market from the losses seen in many other economies.

In January 2020, Korea’s unemployment rate was 4.0%, at the higher end of the 3-4% range it had been in through most of 2019. The drop to 3.3% in February looks more like bad seasonal adjustment than any genuine improvement, and by March the rate had shot back up to 3.8%. But even at its worst in May, it reached only 4.5%, and the latest reading for July is now down at 4.2%, having fallen for two consecutive months.

Labour market stability has certainly shielded Korea’s domestic economy from the ravages suffered elsewhere

This labour market stability has certainly shielded Korea’s domestic economy from the ravages suffered elsewhere. At their worst, in March this year, real retail sales were only down a little more than 8% YoY. They recovered to +6.3%YoY in June, before the second wave took them back to +0.5%YoY in July. Much of this is attributable to domestic auto sales. Real domestic auto sales have recovered from a 22% YoY decline in February to show a 66% increase now. Discounting is helping, especially for sales of domestic autos, but there aren’t huge discrepancies between the real and nominal sales series.

Clearly there is no demand for luggage currently, which at about -26%YoY, real or nominal, isn’t likely to pick up until international travel resumes, maybe not until mid-2021. Mask wearing and home working is likely to be a reason for the heavy toll taken on cosmetics, and possibly also clothing and footwear. Like the export series we mention later, computers are selling well, though the same is not true for telecoms equipment, which suggests there is more going on here than simple pent up demand, and the need for upgraded IT equipment to support homeworking seems like a logical explanation, along with games consoles for bored kids (sports and entertainment).

Real retail sales by type YoY%

Housing - on the rise, everywhere!

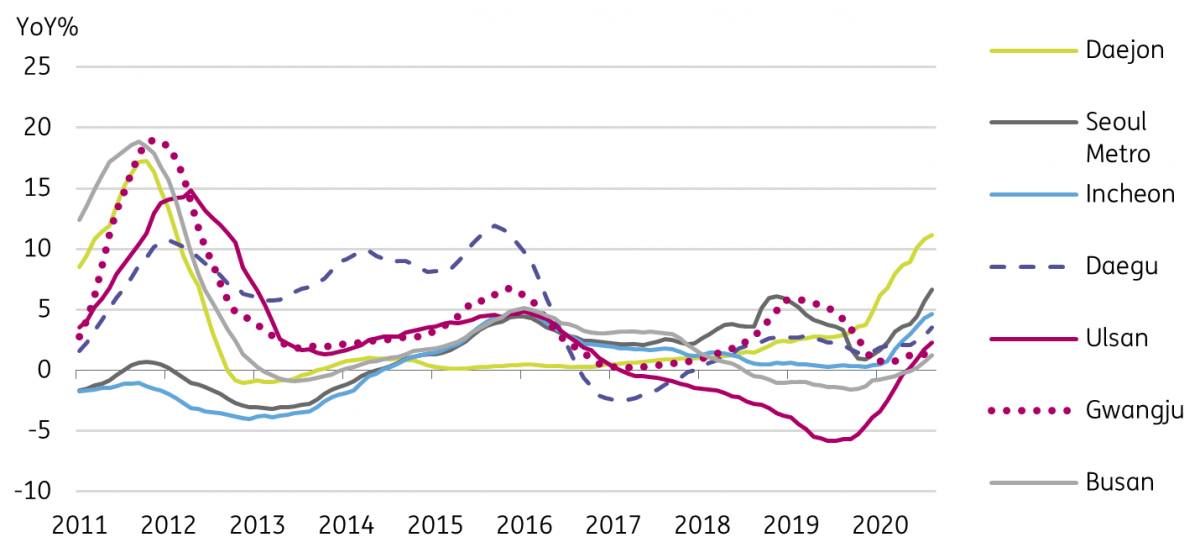

A rather surprising aspect of the Korean macro story is the resilience of the housing market. Where once housing market strength was a metro Seoul story, it is now widespread across the nation, with the central city of Daejeon leading the pack. It may be no coincidence that Daejeon is known as Asia’s silicon valley, given the positive skew that semiconductors are showing in the rest of the economy.

Low interest-rates are clearly a pivotal factor in supporting Korean housing

Low interest-rates are clearly a pivotal factor in supporting Korean housing, and this is one of the reasons why we think it is very unlikely that the central bank cuts the 7-day repo rate again from its current level of 0.5%. Political pressure not to stoke a property bubble is perhaps not as misplaced as it may once have seemed, and household debt levels and debt service ratios remain very high by international standards.

Residential property prices

Inflation - nothing to trouble the BoK for a long while

Despite the resilience of the housing market, consumer price inflation remains on a downward trend.

Headline inflation has been negative several times in recent months, though it is currently holding above zero at about 0.7%YoY with the core rate a little lower at 0.4%. Both series are quite erratic, but neither appears to show any signs of trending higher. And there is a danger of a more protracted period of disinflation.

Headline inflation has been negative several times in recent months, though it is currently holding above zero at about 0.7%YoY with the core rate a little lower at 0.4%

Whether cutting rates any more or embarking on any of the other policies which central banks have embarked on in recent years (genuine quantitative easing, yield curve control, negative rates) would help raise inflation back towards its 2% target is extremely doubtful. Indeed there are powerful arguments that it could make things worse.

But equally, there are few grounds for serious concern. By sub-component, much of the disinflation stems from falling education prices following the government’s exemption of some fees for high school students. And the category recreation and culture may also be affected by the government’s expanded budget to subsidise businesses that encourage employees to go on vacation.

So much of the recent weakness can be attributed to administered prices, and is evidence of fiscal stimulus, and is a response to, rather than a symptom of domestic economic weakness. Until recently, communications (telecoms) were also a big drag on the inflation rate, though that is also beginning to dissipate.

Consequently, and together with the apparently unwelcome resurgence in house prices, we don’t see the central bank cutting rates any further from the current 0.5% 7-day repo (policy) rate.

Headline and core CPI inflation YoY%

Government spending - no end to the support

In our recent report, we outlined the government’s support measures for the economy in the light of the pandemic.

If the early response was a little anaemic, following the landslide victory for President Moon’s DPK in legislative elections in April, fiscal support measures have been extensively ramped up. That said, we see the fiscal deficit rising to only 6.3% in 2020, up from a deficit of 1.9% in 2019. That sounds like a lot, but for a “rich” country like Korea (considering per-capita GDP and low overall debt to GDP levels) it is not by any means excessive, and there is plenty of room for the government to keep spending if this is needed to keep the economy ticking over until a vaccine becomes widely available.

Even by the end of 2022, Korea’s debt to GDP ratio is likely to be only slightly greater than 50%, leaving it with plenty of room for further fiscal support should that become necessary

The nature of the government’s spending has also been encouraging on some levels. With more of a focus on longer-term productivity, Korea’s “New deal” and “Green New Deal” are welcome moves towards embracing technological change, remote working, e-transport, the hydrogen industry and so on. The main complaint in our recent report was that we felt, in many cases, the spending amounts were a bit token, and far more would be required quickly to make a real difference.

But it is still better than most of the countries in the region.

Government debt levels will only rise to 44% of GDP by the end of the year (see forecast table at the end for detail) according to our estimates (a bit more than the MoEF estimates of 43.5%). That is a testament to the prudence of past governments. But in our view, this is not the time to be thinking in terms of “prudence”, but rather if you need a catchphrase, “spending to survive”. The recently passed budget for 2021 keeps fiscal support going, with an increase of KRW8.9tr over the spending totals for 2020 (including the three supplementary budgets) to KRW555.8tr.

Even so, Korea’s debt to GDP ratio by the end of 2022 is likely to be only slightly greater than 50%, leaving it with plenty of room for further fiscal support should that become necessary.

Export markets limp, and not a lot that can be done about it

Recent export data has shown some signs of improvement, with the year on year export decline moderating from its April nadir of -25.6%YoY, to only -9.9% in August. However, the improvement seems quite narrowly based around the semiconductor industry – no change there from other recent business cycles.

This has been the Korean export story since 2015, with occasional but short-lived improvements in other sectors. The best we can say outside semiconductors is that exports of vessels seem to have stabilised. All other major groups, with the possible exception of autos, computers and mobile phone-related items which have all ticked up recently, remain in decline.

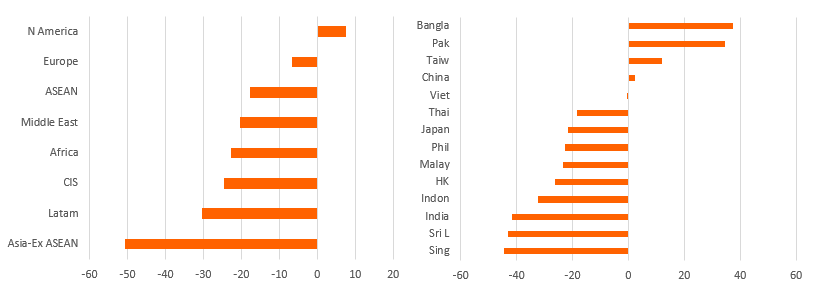

Perhaps the biggest surprise in terms of the geographical destination of Korea’s exports, is how strong exports to North America have been

Overall, exports have only just returned to the bottom of the broad range they have inhabited since 2010. This is likely to see only slow improvements as the rest of the world gradually recovers from the pandemic and economies move forward again. And that is a 2021 story at the earliest. Maybe in 2022.

Korean exports - a two speed story, as usual

Perhaps the biggest surprise in terms of the geographical destination of Korea’s exports, is how strong exports to North America have been. Given the abysmal performance of the US through this pandemic and the weakness of the USD, this is something of a mystery. All the improvement have come since May, when exports to North America, were down 32.5%YoY.

One possible explanation is that this represents pent up demand post-lockdown to upgrade personal IT equipment to cope with the new working from home norms. If so, it may not be too persistent.

Exports to Oceania have also recovered strongly since their 55.2% April low, reflecting the good performance of Australia and New Zealand during the pandemic, until their recent case spikes and regional re-closures. We may also see these figures drift lower in the coming months as a result. Elsewhere, it’s a not terribly surprising picture of declines, with the Middle East and Africa leading the fall, followed shortly behind by the CIS states and Latin America. No further explanation probably needed for them.

Exports by region and Asian country

There is also an interesting and at times equally perplexing mix of export growth across the Asia-Pacific region.

Two countries topping the list, are Bangladesh and Pakistan. As both have had fairly awful pandemics, and neither is known for being integral to Korea’s technology export value chains, this raises more questions than it answers. At the bottom of the pile, Singapore, which for some months now since the end of the extended circuit breaker, has been operating close to a "business as usual" model is another oddity, especially, or perhaps because its own semiconductor exports have been looking a lot healthier in recent months.

Markets - everything hangs on market risk sentiment

The Korean won is one of Asia’s high beta currencies. It does poorly when global risk sentiment is bad, and well when it is good.

America’s S&P500 equity index troughed on 23 March. Since then[1], the Korean won has appreciated by 6.61% against the USD, in the upper half for the region as a whole, though lagging behind the Indonesian rupiah (which had fallen far more heavily on the way down), just behind the MYR (helped by resurgent crude prices) and SGD (+6.85%) and way more than the CNY (+3.63%) which as the region’s biggest currency often sets the tone for how others perform.

From a Korean perspective, we don’t see any further accommodation from the central bank

We anticipate some further appreciation ahead, but there are some increasing headwinds to this as part of the won’s appreciation simply reflects USD weakness. While this trend may continue for some time, the dollar index is already at a two-year low, and a further 3pp decline would take it to five-year lows. While the Fed’s actions are not exactly supportive, they aren’t doing much more than any other central bank to debase their currency, so it is not clear why the USD should be doing so poorly relative to the other majors, or Asian FX like the KRW.

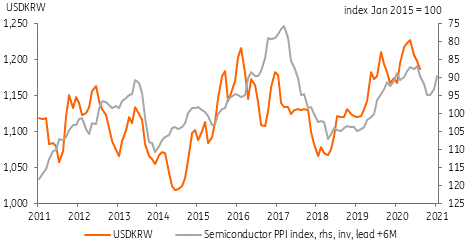

From a Korean perspective, we don’t see any further accommodation from the BoK as mentioned earlier. Terms of trade for Korea will mainly reflect unhelpful swings in imported energy prices (we don’t see crude oil rallying too much more from here) and positive unit prices for Korea’s main export, semiconductors. We can proxy this by PPI output prices for semiconductors, which explain some of the variances in USD/KRW, with about a 6m lead.

Some further appreciation seems probable given that semiconductor prices have only really just started rising, but are at risk of a re-escalation of the US-China tech war.

[1] As of 3 September 2020

Semiconductor prices and USD/KRW

The 10-year Korean Treasury bonds currently yield about 1.50%, a spread of about 84bp over equivalent US Treasuries[1].

Ironically, we feel that the greatest risk to risk sentiment would be for growth prospects in Korea and globally to improve so much that markets began to re-price in monetary tightening in Korea or the US

The inputs into the Treasury yield calculation (US and Korea) are growth, inflation, and risk sentiment (proxied by equity moves). The growth outlook will improve in 2021, but is unlikely to provide any material surprises, and the same can also be said for inflation. Perhaps the main risk to the KTB outlook, which we see staying low with just a slight tendency to rise through the end of the year and into 2021/22, is risk sentiment. Sentiment may remain extremely positive for years, in which case, our forecast for further small yield increases will likely follow. But equally, it could crash without warning.

Ironically, we feel that the greatest risk to risk sentiment would be for growth prospects in Korea and globally to improve so much that markets began to re-price in monetary tightening in Korea or the US. While at this state, that seems a remote prospect, that might begin to look more probable should a safe and effective vaccine start to become widely available sometime in 2021/22.

That would deliver a sharp flattening of the yield curve and might also accompany an equity sell-off.

[1] 3 September, 2020

Forecasts

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 9 September 2020

- This bundle contains 3 Articles