Korea: Central bank policy stalemate

- 31 July 2018

- South Korea

Slower growth and rising inflation put the Bank of Korea's policy in limbo, supporting our forecast of no policy change through mid-2019

Forward-looking Korean confidence indicators paint a picture of dim growth for the coming months, while inflation continues on an uptrend. These developments put the central bank's policy in limbo. We aren’t forecasting any change to the 1.50% BoK policy rate through mid-2019.

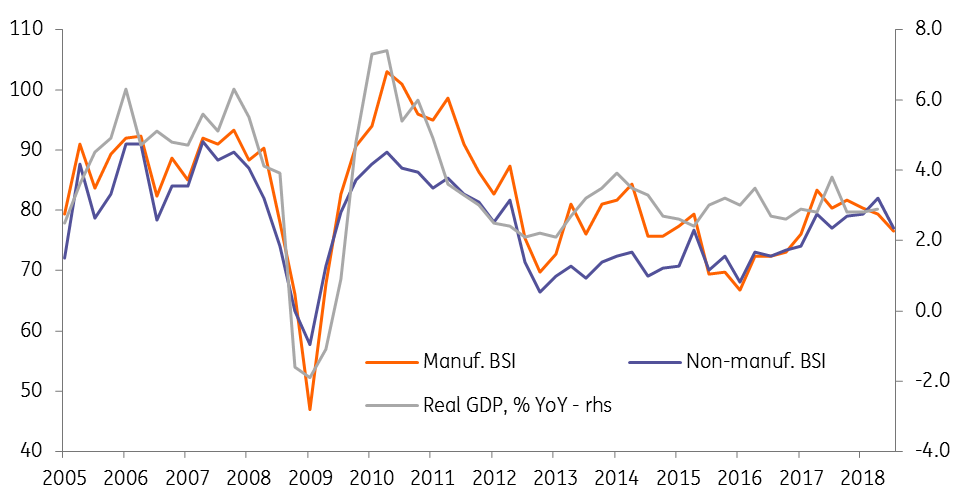

Weakening business confidence

The BoK released its manufacturing and non-manufacturing business survey indexes (BSI) for July. The focus typically is on the forecasts of these indicators for the upcoming month, in this case, August. And they posted their steepest decline in three years, from the point of 80 for both in July to 73 for manufacturing and 74 for non-manufacturing in August. These indexes indicate the continued tapering in GDP growth in the period ahead (see figure).

Weakening business confidence point to slower GDP growth

Evolving growth-inflation dynamics

Besides this, the releases tomorrow of trade and inflation data for July will shed more light on evolving growth-inflation dynamics of the Korean economy. We consider consensus forecasts of 7.4% YoY export growth and 17.0% import growth- implying a significant improvement over -0.1% and 10.7% in June- to be optimistic. We anticipate a contraction on the order of 2.6% YoY in exports and 1.3% in imports, which will be associated with a near-halving of the trade surplus to $3.2 billion in July from $6.2 billion in the previous month.

Our 1.7% YoY July inflation is in line with the consensus. Inflation bottomed at 1% at the start of the year in January and has since accelerated to 1.5% by June as a result of the double-whammy from firmer global oil prices and a weaker Korean won (KRW). While these factors will remain in play through the rest of the year, the higher trade tariffs and the low base effect will also add to the upward inflation pressure.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 1 August 2018

- This bundle contains 5 Articles