Key events in EMEA next week

- 21 April 2023

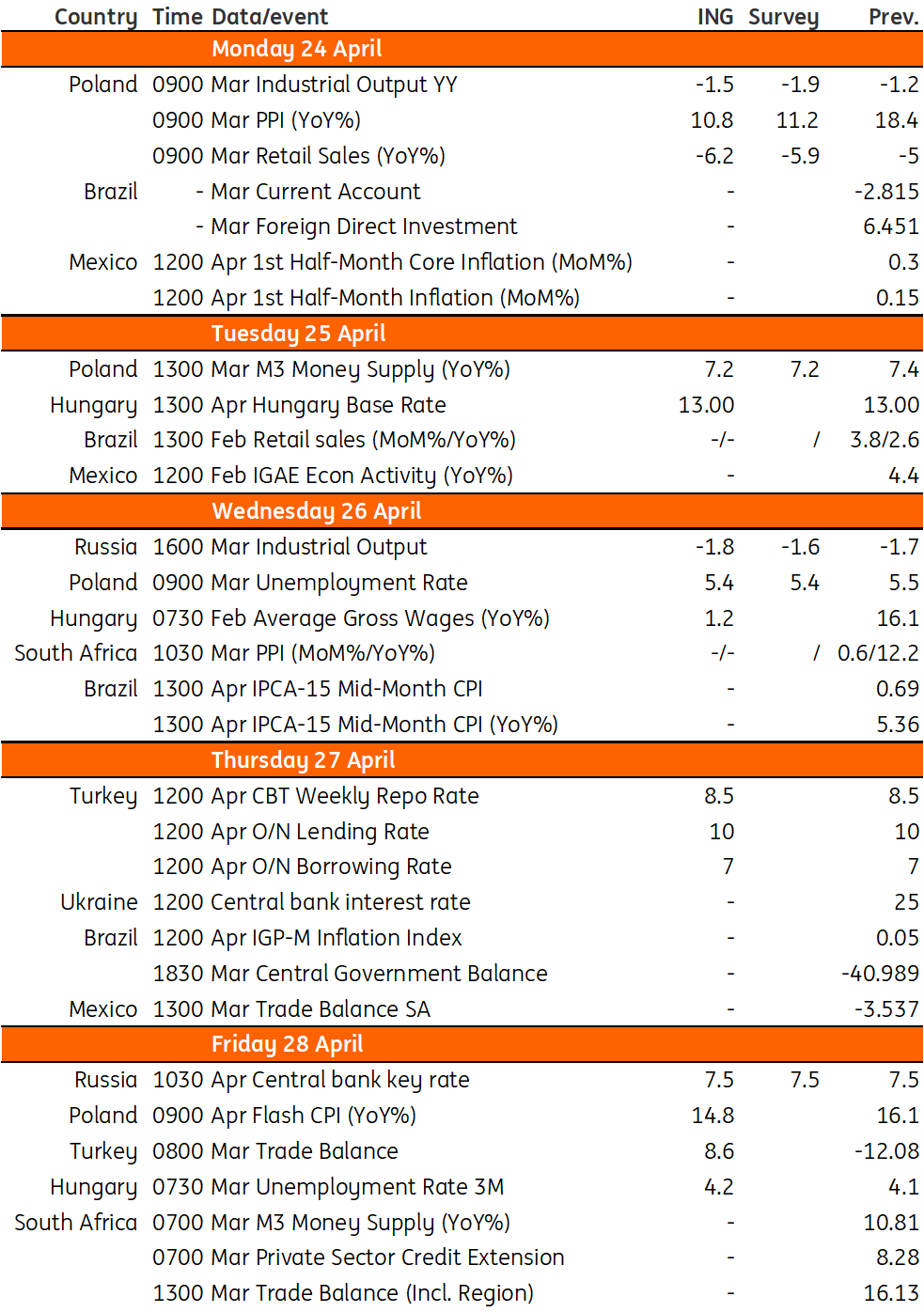

- Key Events

Following the National Bank of Hungary's dovish remarks, we could see a bold 700 basis point cut in the overnight repo rate next week while the base rate will remain at 13%. This is contingent on stability in the forint after a recent sell-off. For Poland, we see an array of activity data, as headline CPI continues to drop given a reversal of the energy shock

Poland: Expect core inflation to remain persistent

Retail sales: -6.2% YoY (March)

After a 5% year-on-year decline in February, the fall in retail sales most likely deepened in March. From a purely statistical point of view, this reflects the high reference base from March 2022, when the first wave of refugees from war-troubled Ukraine boosted purchases of pharmaceuticals, clothing and footwear. The broader economic picture is not pretty either. The drop in purchases of goods in recent months is a result of high inflation that has hit the real disposable incomes of households. The annual drop in household consumption in the first quarter is expected to be even deeper than observed in the fourth quarter of 2022 and consumption is projected to start recovering gradually, but not earlier than in the second half of the year.

Industrial production: -1.5% YoY (March)

Industrial output is also in negative territory as manufacturing activity eased amid softer external demand. Even though the 2022/23 winter energy crisis turned out to be less profound than feared, the turmoil in the US banking sector brought new risks (potential credit crunch) that may weigh on the outlook for global manufacturing. Annual declines in energy production in Poland are also associated with a high reference base as coal-based energy production and exports in Poland soared when natural gas became more expensive due to hostile Russian measures.

PPI inflation: 10.8% YoY (March)

Producers’ inflation peaked in mid-2022, but the pace of PPI disinflation has been relatively moderate so far – from 25.6% YoY in June 2022 to 18.4% YoY in February 2023. The decline in PPI inflation will gain momentum in the near term and already in March, producer price growth is projected to have nose-dived to c.11% YoY amid the strong base effect. In March 2022, the PPI index soared 6.6% month-on-month as a spike in wholesale gasoline prices pushed prices in the manufacture of coke and refined petroleum products up by 31.4% MoM.

Registered unemployment: 5.4% (March)

The slowing economy will eventually make its mark on the labour market, but it remains tight so far. Even though some initial signs of softening emerged recently (decline in enterprise sector employment and increase in the number of unemployed in February 2022), we do not expect any sharp deterioration in the near term. Demographic trends led to a scarcity of workers and the gap has been filled by immigrants so far. We forecast that in March, the unemployment rate inched down to 5.4% from 5.5% in February – in line with seasonal patterns.

CPI (flash): 14.8% (Apr)

Disinflation of headline CPI is expected to continue in April on the back of the reversal in the energy shock but core inflation will likely remain close to the March reading of 12.4% YoY as an upswing in costs is still feeding into a broader array of goods and services prices.

Turkey: Central bank set to keep rates unchanged

At the March Monetary Policy Committee meeting, the forward guidance remained unchanged as the Central Bank of Turkey repeated that the current policy rate is adequate to support the recovery in the wake of recent earthquakes. This implies that it will not make any rate move and remains in a wait-and-see mode in the near term. Given this backdrop, we expect the bank to remain on hold at the April meeting.

Hungary: Possibility of a bold 700bp cut in overnight repo rate

The National Bank of Hungary’s latest remarks made next week’s rate-setting meeting pretty very interesting. We see the central bank cutting the overnight repo rate from 25% in a significant manner. The size of the cut could be dependent on the behaviour of the forint. Should we see stability in the currency after the sell-off ignited by the dovish remarks, we might see a bold move of a 700bp cut. With that, the overnight repo rate would match the 18% effective rate, suggesting that from now on, the only way is down for effective rates. No other rates are expected to be changed; thus the effective rate will remain at 18% at least until the May meeting, while the base rate will remain at 13% for a longer period. With the rate setting behind us, the focus will be on the labour market. The unemployment rate is expected to inch higher, while wage growth could be a shocker. This is due to last year’s one-off wage increase for the armed forces in February, which pushed wages higher by 31.1% YoY.

Key events in EMEA next week

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Our view on next week’s key events

- This bundle contains 3 Articles