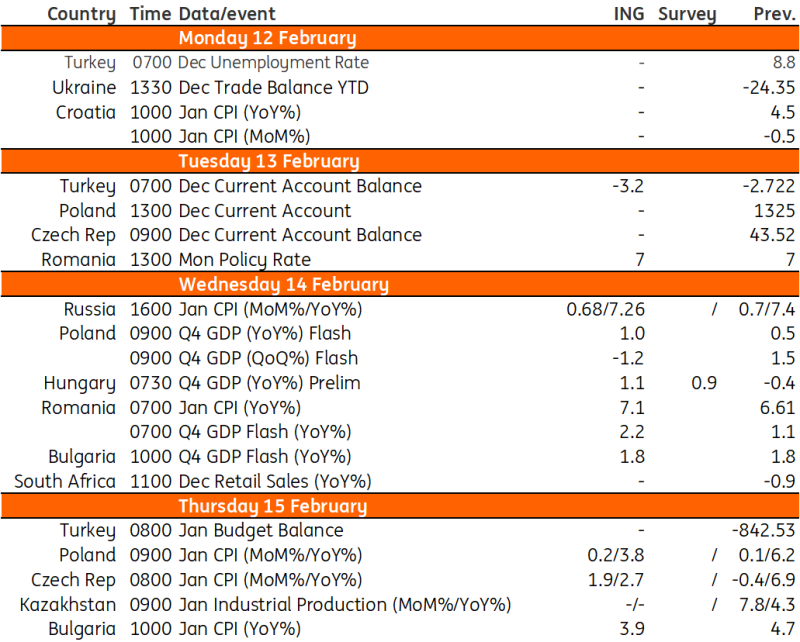

Key events in EMEA next week

In Poland, GDP and CPI releases will be the highlight of next week. Meanwhile, we expect to see headline inflation in the Czech Republic heading closer to the central bank's target, while fourth quarter GDP in Hungary should be positive due to base effects. We forecast the National Bank of Romania will keep rates on hold at its February meeting

Poland: Headline inflation expected to moderate below 4% YoY

GDP (4Q23): 1.0% YoY

Since the StatOffice has already released the preliminary 2023 GDP estimate, the fourth quarter result is less of a mystery now. Economic growth at 0.2% year-on-year in 2023 implies growth of around 1.0% YoY in 4Q23. This is a bit of a disappointing reading, following encouraging signs in 3Q23. Household consumption, in particular, fell short of expectations as it most likely stalled in YoY terms after expanding by 0.8% YoY in 3Q23. Despite the rebound in real disposable income, households remain hesitant and cautious with spending. At the same time, fixed investment continued to rise at a solid pace (7-8% YoY). We estimate that foreign trade contributed positively to 4Q23 GDP growth, while the change in inventories was still a serious drag on growth. We still remain positive on the 2024 outlook and forecast consumption-led growth of 3%.

CPI (January): 3.8% YoY

The January CPI report will be of a preliminary nature as the reading will still be based on the 2023 basket weights and limited in detail (only the main categories will be unveiled). We estimate that food prices changed little vs. December 2023 and headline CPI inflation moderated below 4% YoY amid a high reference base from January 2023, when VAT on energy was restored. The figure will be revised in March along with the update of CPI basket weights. Still, we expect a V-shaped inflation path in 2024, with rapid disinflation in 1Q24 and a bounceback in the second half of 2024 as measures that froze energy prices will expire and authorities introduce new solutions (yet to be decided).

Czech Republic: After more than two years, inflation is finally close to target

For January, we expect the traditional high seasonality in the Czech Republic to push prices up by 1.9% month-on-month. Almost all items in the consumer basket rose, in our view. However, the main issue will be the change in energy prices, which are rising in the regulated component but falling in the market component. Overall, however, we expect housing prices, which include energy prices, to have gone up 0.7% in January. On the other hand, downward pressure on inflation is coming from the volatile components i.e. food and fuel prices. In both cases, we expect a decline of around 1% MoM. The headline YoY number should thus fall to 2.7% due to the large base effect from last year. Core inflation should stagnate around 3.6% YoY. The central bank expects a headline number for January of 3.0% YoY. If January inflation does indeed show levels somewhere below 3%, we believe that other months should be at similar levels comfortable for the central bank.

Hungary: Low base saves the day for 4Q GDP

The only (and really important) data point will be the release of 4Q GDP in Hungary. We expect a significant positive contribution from agriculture thanks to base effects and supportive weather, while industry, construction and services will all contribute negatively to the year-on-year GDP growth index. But once again, the low base will save the day. As the fourth quarter of 2023 had two fewer working days than the last quarter of 2022, we expect significant revisions to previous data points due to seasonal adjustments. In short, we will see an economy in a gentle recovery phase, emerging from a technical recession. Despite the positive momentum in the second half of the year, the full-year performance remains disappointing, with a 0.7% contraction in 2023.

Romania: National Bank of Romania to keep rates on hold

In Romania, we expect the NBR to keep rates on hold at its 13 February meeting and we think it's likely that we will see some mildly dovish signs put forward by officials. On 14 February, we expect to learn that annual growth picked up in the fourth quarter, on the back of accelerating private consumption and still-strong fixed investment. That said, we think that less positive developments are due on the inflation front, as data will likely show that price pressures picked up to 7.1% in January (December: 6.6%) as firms pushed higher taxation costs onto consumers.

Key events in EMEA next week

Download

Download article9 February 2024

Our view on next week’s key events This bundle contains {bundle_entries}{/bundle_entries} articles

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more