Key events in EMEA next week

Poland’s current account surplus and Hungarian and Czech inflation figures are set to be the key highlights in a quieter week ahead in the EMEA region

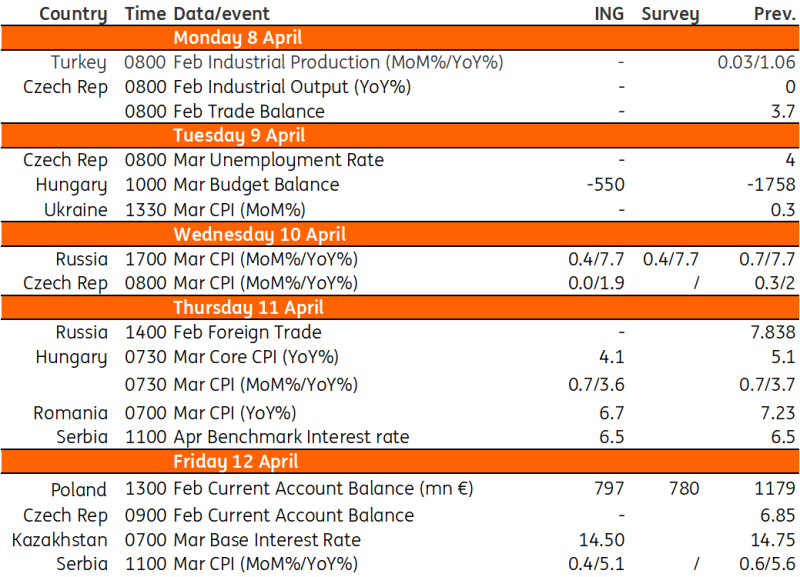

Poland: Current account surplus from strong trade in goods

Current account (Feb): €797m

We forecast a €797m surplus for Poland's current account in February 2024, but it will be smaller than in February 2023 (€147m) amid a deterioration in the foreign income balance. As a result, the cumulative 12-month current account surplus will narrow to 1.3% of GDP, down from 1.4% of GDP after January this year. Still, we expect a solid surplus in trade in goods, and we hope to see positive annual dynamics for both exports and imports.

Nevertheless, net exports are projected to contribute negatively to economic growth in 2024; the anticipated rebound in imports is expected to be stronger than improvements seen in exports. The former will be fuelled by surging domestic demand and buoyant consumption, while the latter is likely to be curbed by weak external demand, particularly from Germany.

Czech Republic: Inflationary pressures continue to fall

Headline inflation fell to 2% in February, hitting the central bank's target. For March, we expect inflationary pressures to weaken further from 0.3% to 0.0% MoM. This should translate into a slight decline from 2.0% to 1.9% YoY. Food prices, energy prices, and – due to seasonality – recreation and culture prices headed lower in March. The latter in particular was the main reason for higher core and service inflation in previous months. We expect the downward movement in this item to outpace the normal seasonal movement and help push service inflation down as well.

Household energy prices have also seen a significant decline, confirmed by energy companies announcing tariff cuts for March and April. However, it is unclear what proportion of households will be affected and we therefore see more downside risks here. On the other hand, fuel, clothing and transport prices rose in March. The government also decided to increase the price of motorway vignettes since March (+0.08pp).

Hungary: March inflation to decelerate to 3.6%

In Hungary, we will see the latest budget figures for March as well as the March inflation print. On the fiscal side, we expect another monthly deficit but a much more consolidated figure than in the previous month. Some one-off burdens on the expenditure side will be taken off the books, and the revenue side is expected to improve as domestic demand slowly but surely strengthens. On the price side, we see another strong monthly repricing, with the third 0.7% print in a row.

Services will remain the main driver of monthly inflation, especially holiday packages and telecommunications services. On top of that, further increases in fuel prices will also add to inflationary pressure. Looking at the year-on-year rate, we see a further slight deceleration to 3.6% due to the still relatively high base. The lion's share of annual price increases (around 70%) will come from services inflation. The slight deceleration is the result of opposing forces, with fuel and household energy prices contributing positively to the change from February to March, while a change in food, alcoholic beverages and tobacco prices will weigh on the year-on-year reading.

Key events in EMEA next week

Download

Download article5 April 2024

Our view on next week’s key events This bundle contains {bundle_entries}{/bundle_entries} articles

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more