Key events in EMEA next week

- 24 March 2023

- Key Events Czech Republic Hungary

We expect both the Czech National Bank and the National Bank of Hungary to keep interest rates unchanged next week, with officials maintaining their hawkish tone

Hungary: No change to the current status quo

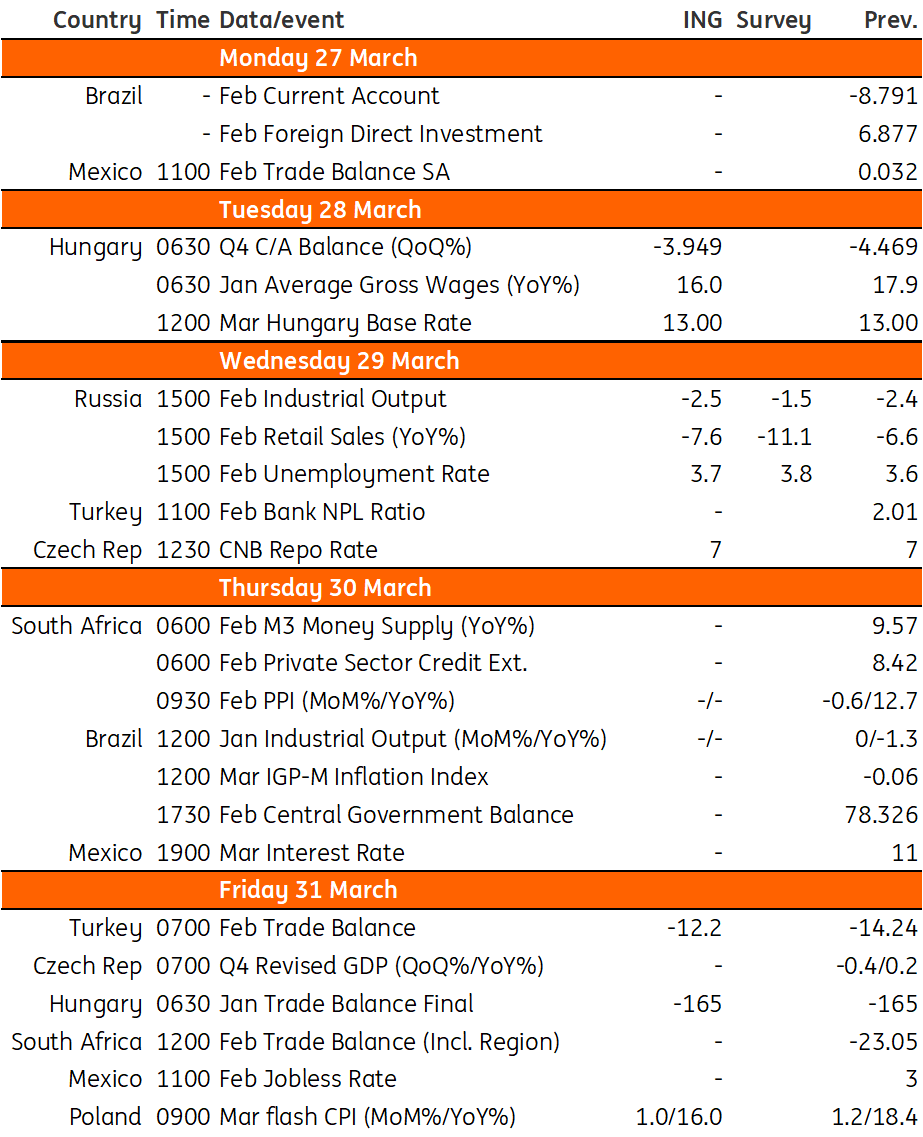

After two relatively quiet weeks as regards to data in Hungary, the upcoming one will be more interesting. Or to be precise: Tuesday is in focus. We are going to see the January wage growth data, which used to be a strong anchor for the full-year average increase in salaries based on the past five years’ data. We see a 16% gross wage increase on a yearly basis due to a combination of a 14-16% minimum wage increase (for unskilled and skilled labour), the labour shortage and the high-flying inflation. We expect a minor improvement in the fourth quarter current account deficit compared to the previous quarter based on high-frequency data. Last but not least, even without the recent market turmoil, we would advertise a no-change scenario in the Hungarian monetary policy, as Tuesday earmarks the date of the March rate-setting meeting. Considering the vulnerability of the forint, a rate cut will be quite premature exposing the local currency to a sell-off. Against this backdrop, we see an all-around status quo at the upcoming meeting: no change in rates, only incremental revisions in the central bank’s forecasts and unchanged (hawkish) tone of the forward guidance.

Czech Republic: Official to keep its hawkish tone, whilst rates remain unchanged

The Czech central bank is likely to keep interest rates unchanged on Wednesday. We expect the official statement will keep its hawkish tone, which means maintaining the current level of interest rates until there are clear signs that inflation is returning to the central bank's 2% target. Even the soft recession has not brought relief to the labour market, which still remains very tight, with the unemployment rate being the lowest in the EU, and poses the risk for inflation expectations.

Key events in EMEA next week

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Our view on next week’s key events

- This bundle contains 3 Articles