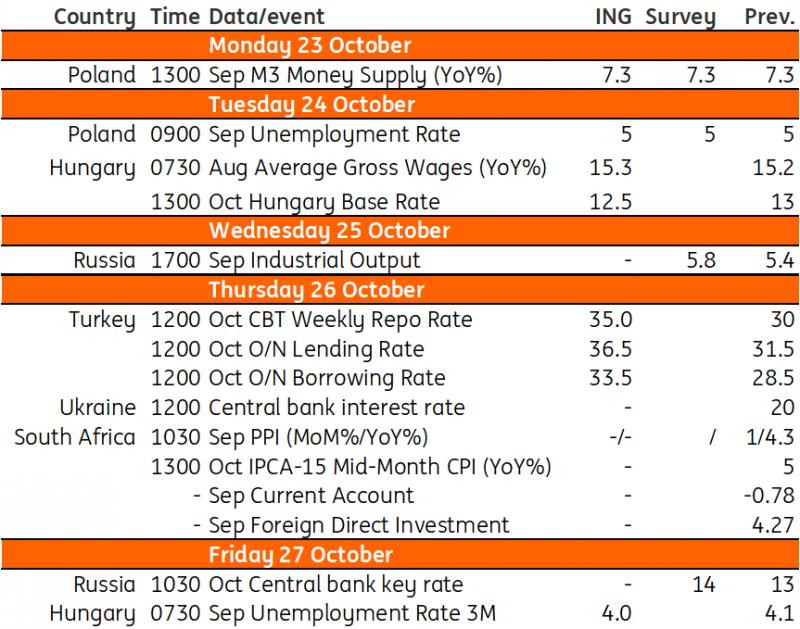

Key events in EMEA next week

We expect the Central Bank of Turkey to hike its policy rate by 5ppt next week to 35%. In Hungary, a marked strengthening of the forint could allow the central bank to make an even bigger cut at its policy meeting than our 50bp base case

Turkey: We project a 5ppt hike

The CBT’s focus has remained on anchoring inflation expectations and achieving disinflation. Following a 12.5ppt hike at each of the last two MPC meetings, we expect the central bank to raise rates by another 5ppt at the October meeting, bringing the policy rate to 35%. This would lead to a positive ex-ante real policy rate based on the 33% inflation forecast for 2024 in the medium-term plan. Macro-prudential tightening should also help disinflation efforts. However, in the rate-setting note released last month, the CBT's assessment of the inflation outlook showed some changes as it saw that i) the adjustments in FX, wages and taxes have now largely passed through to inflation, and ii) the underlying trend in monthly inflation will start to decline. The new reference to the declining monthly inflation trend implies that we should not rule out the possibility that the policy rate this month could be adjusted by less than 5ppt.

Hungary: We expect a 50bp cut in the key rate

In Hungary next week, there will be a spotlight on the labour market and monetary policy. With respect to the former, we have seen some seasonal enhancement in the number of people at work, indicating a slight fall in the unemployment rate in September. Although there was a projected strong year-on-year wage increase in August (15.3%), this wouldn’t bring any significant change in wage growth. As a result, we will have had 12 months of negative real wage growth. Nevertheless, there is a silver lining. This trend likely ended in September, as the inflation rate has already significantly dropped to 12.2%. This leads us to the topic of monetary policy. With a policy rate of 13%, September marks the start of a new era of ex-post positive real interest rates. Due to the recent progress in inflation dynamics and market sentiment, our projection is that the Hungarian central bank will reduce the key rate by 50 basis points at next week's rate-setting meeting. However, given the agility of monetary policy, a marked strengthening of the forint on the back of the expected positive outcome of a deal with the EU could provide an opportunity for the National Bank of Hungary to make an even bigger interest rate cut than our base case.

Key events in EMEA next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

20 October 2023

Our view on next week’s key events This bundle contains 3 Articles