Key events in EMEA next week

- 6 January 2023

- Key Events

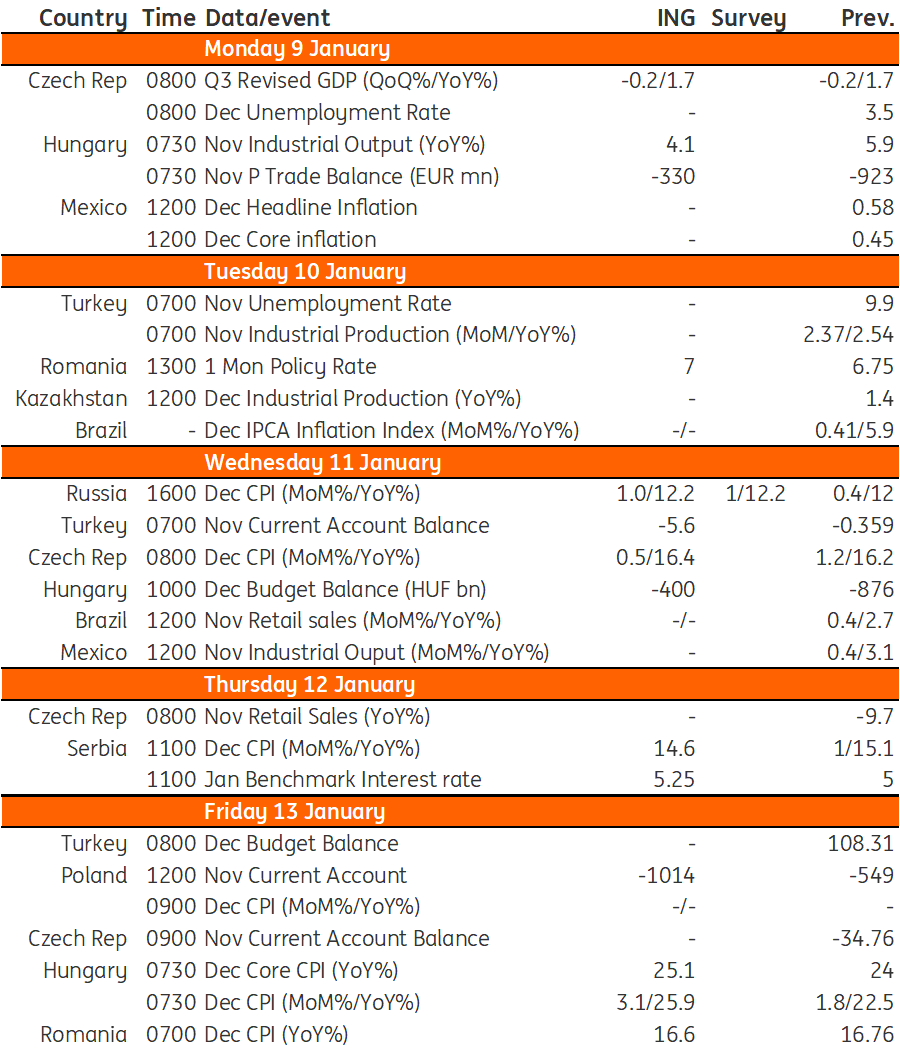

In the Czech Republic, we expect the monthly rate of consumer inflation to slow from 1.2% to 0.5%, while in Hungary, we see headline inflation in December of 3.1%, moving the year-on-year reading close to 26%

Czech Republic: Mixed inflation picture

For December, we expect consumer inflation to slow down from 1.2% to 0.5% month-on-month, which translates into an increase from 16.2% to 16.4% year-on-year. Fuel and energy prices will again be the main questions for this print. We estimate that fuel prices fell 10% in December, the biggest month-on-month move since March this year. On the other hand, housing and energy prices slowed from November but still maintained a strong 2.2% MoM growth rate. Food inflation declined for the third month in a row (1.0% MoM) and we can expect seasonal cheapening of clothing in December.

Hungary: Sudden phase-out of fuel price cap puts pressure on inflation

We expect the Hungarian industry to show mixed performance in November as smaller subsectors will suffer, while car, electronics and electrical equipment manufacturing (including electric vehicle batteries) will keep the year-on-year production growth in positive territory. In line with that, we see a significant improvement in the November trade balance. This is not just a result of a more vivid export sector, but also due to the dropping energy consumption hence the lowering import needs.

We see the budget closing 2022 with yet another monthly deficit, although the strong nominal GDP growth will help to meet the 4.9% deficit-to-GDP target (excluding the 1.3% of GDP extraordinary gas purchase). The highlight of the week comes on 13 January, and it won’t bring too much joy from an inflationary point of view. We expect headline inflation in December to be at a monthly rate of 3.1%, mainly driven by the sudden phase-out of the fuel price cap, complemented by further food price pressure. This would move the year-on-year headline reading close to 26%, while we forecast a 25.1% YoY core inflation print in the last month of 2022.

Romania: Ample liquidity backdrop blurs the relevance of the policy rate

The Romanian National Bank (NBR) will announce its latest policy rate decision on 10 January. We narrowly favour a last 25 basis points hike to 7.00%, against a no-change decision. Either way, markets might be rather indifferent to the decision as the ample liquidity backdrop significantly blurs the relevance of the policy rate. On the CPI front, we expect the 2022 year-end inflation to have reached 16.6%, though downside surprises cannot be excluded.

Key events in EMEA next week

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Our view on next week’s key events

- This bundle contains 3 Articles