Key events in EMEA and Latam next week

- 17 April 2020

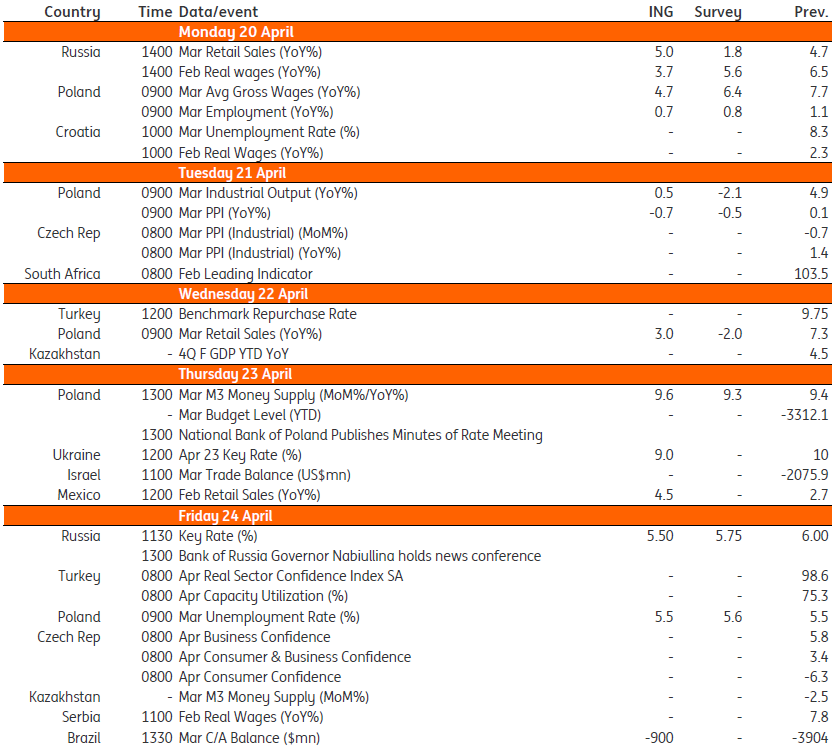

Data across the EMEA region next week should reflect the economic cost of Covid-19. With many central banks having already taken action to mitigate the downside risks to growth, others could follow

Poland

We expect a relatively modest slowdown in the Polish economy in March – both industrial production and retail sales should remain in positive territory owing to calendar effects. The high frequency indicators showed a very decent turnover in ELIXIR payment transfer systems. Also, the loss in energy generation is much lower in Poland compared to eurozone economies. The full blown crisis should be visible in the April figures.

On the labour market front, we expect some stabilisation in the unemployment rate and lower employment dynamics. Labour protection rights should delay the full impact of the pandemic on the labour market to May. Google Trends suggests that the number of queries regarding layoffs is 1.5x higher than during the Global Financial Crisis and the number of queries for temporary forced leave is very high.

Turkey

The Central Bank of Turkey cut the policy rate to single digit figures for the first time since mid-2018 in an unscheduled meeting last month. At the April meeting, we expect the Bank to reduce the policy rate by 75bp to 9%. The Bank seems to be determined to mitigate downside risks to growth while a supportive shift in global policies amid Covid-19 concerns and a widening in the output gap- which is weighing on inflation-should provide room for the CBT to act.

Russia

Russia's central bank is likely to cut the key rate from 6.0% to 5.5% on 24 April. The CBR made a strong dovish shift in its communication on 17 April, strongly suggesting that a cut is not only the primary option but that it may also exceed the standard 25bp. This comes despite the acknowledgment of accelerating CPI and deteriorating inflationary expectations. We believe the shift was triggered by a combination of factors, including:

- Stabilisation on global markets, which helped assure a 2% recovery in USD/RUB and an almost 140bp drop in local 10-year state bonds (OFZ) yields;

- Experience of other emerging market central banks, which have cut policy rates by 25-300 bp in March-April, according to the IIF;

- Deterioration of Russian GDP growth expectations, with the likelihood of the lockdown being extended from April into May potentially costing another 2.5% of annual GDP in addition to the 2.5% YoY drop expected by us earlier;

- Very modest fiscal support in the face of Covid-19 challenges, as the 2.8% of GDP announced by the Russian Ministry of Finance earlier includes 0.5% GDP of state guarantees and a redistribution of previously planned spending of up to 1% of GDP.

Comparing Russia’s real key rate based on 12M expected CPI (currently at 1-2% based on 4-5% CPI consensus range) to its direct EM/commodity peers (ranging from -0.5% in Saudi Arabia and South Africa to +1% in Malaysia and Indonesia), the near-term downside to the nominal key rate is 50-100bp. While a more aggressive cut can not be excluded, the near-term risks to the rouble and deposit outflows we mentioned earlier may limit the CBR’s room for manoeuvre.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Our view on next week’s key events

- This bundle contains 3 Articles