Key events in EMEA and Latam next week

- 15 February 2019

- Key Events

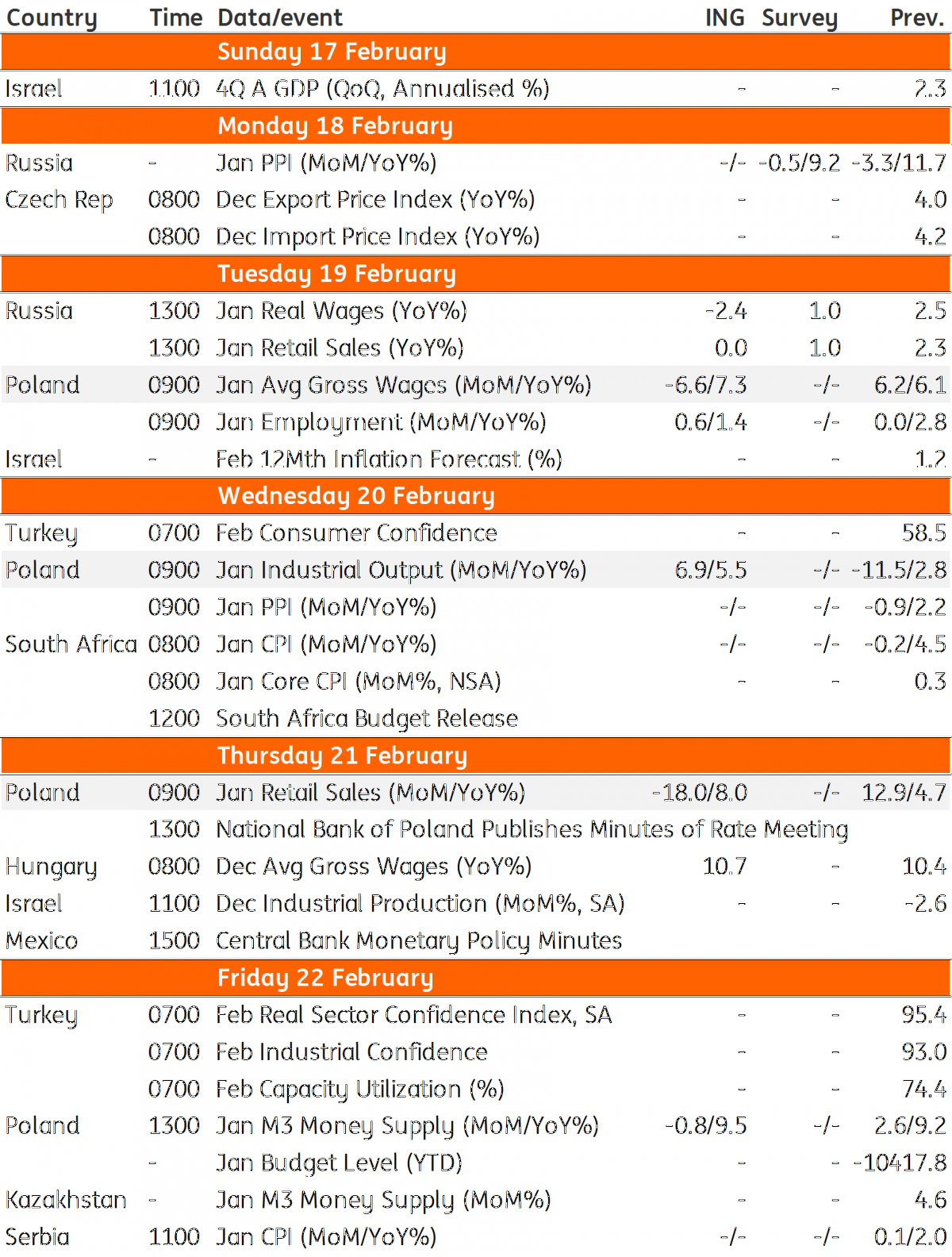

Next week should be relatively subdued on the data front but positive news is expected from Poland. Rebounding retail sales and industrial production, as well as decent labour market fundamentals, point to a pretty solid January

Poland: Solid activity in January

Industrial production should recover from 2.8% in December to 5.5% year-on-year in January; the disappointment in December was largely related to the construction sector, which plays a minor role in both January and February. Exports maintained a decent performance. Retail sales should also rebound from 4.7% to 8.0% YoY; the December reading was dragged down by clothing (due to weather effects) and food sales. Both categories should recover in January while demand for durable goods should remain solid.

Labour market data should also paint a positive picture. We expect an increase in wages from 6.1% to 7.3% YoY; the December reading was reduced due to a smaller contribution from the mining sector. Also, the minimal wage hike in January should add approximately 0.4 percentage points to the headline figure. Enterprise employment is likely to be lower when compared to previous years but a rapid drop reflects a statistical anomaly rather than a structural change. Each year the statistical office rebalances the panel of enterprises adding new companies to the sample. In 2018, such a procedure resulted in an abnormal increase in employment, which likely won't repeat this year.

EMEA and Latam Economic Calendar

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Our view on next week’s key events

- This bundle contains 3 Articles