Key events in EMEA and Latam next week

- 14 June 2019

- Key Events

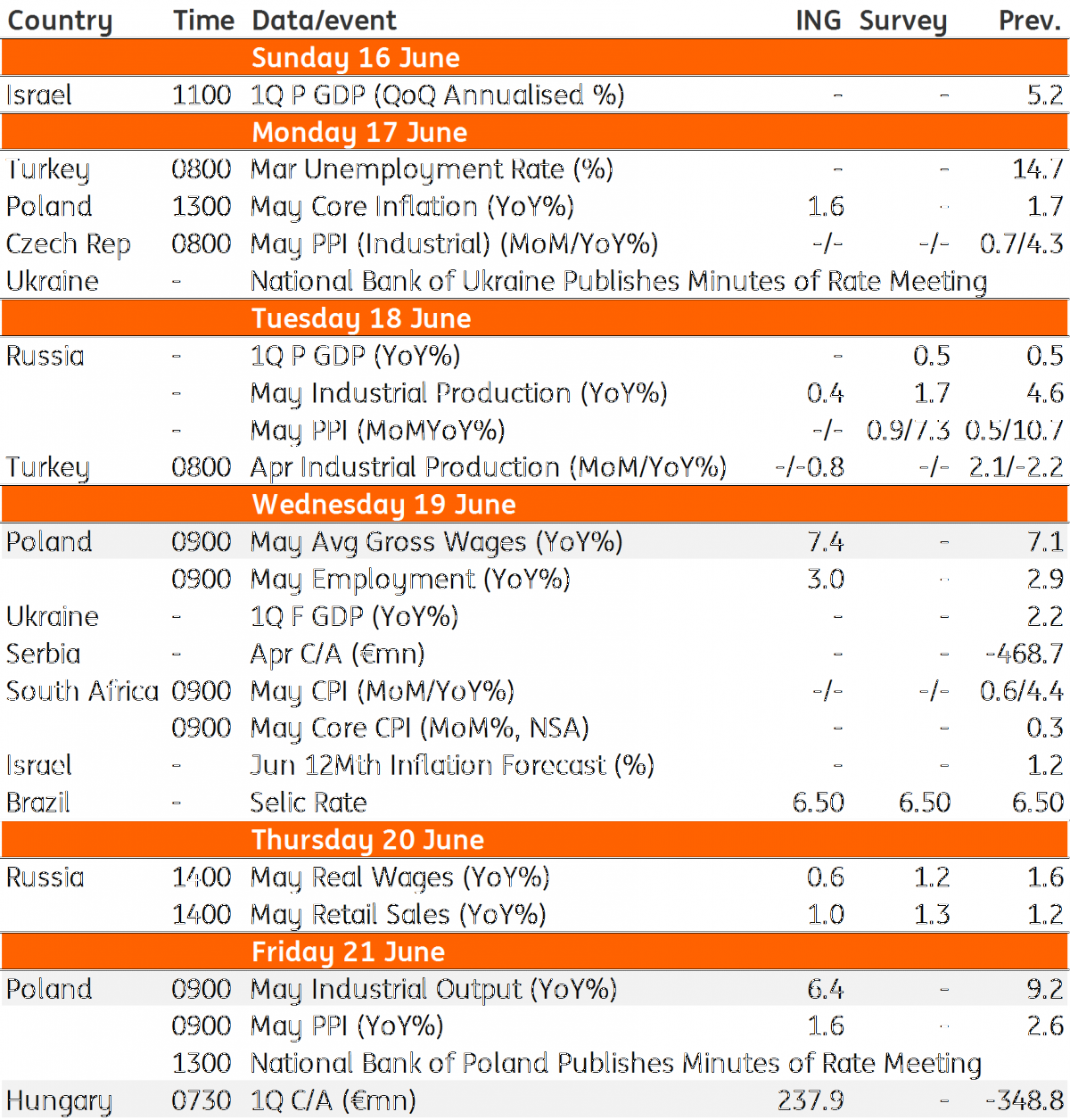

Next week, Polish data should confirm 2Q GDP is likely to be stronger than what we previously thought, despite adverse economic conditions in the external environment. We could also see the current account balance in Hungary finally come out of negative territory

Poland: Strong 2Q GDP on the horizon, despite external headwinds

We expect industrial production to decelerate in May from 9.2% to 6.4% YoY, reflecting mainly a difference in the working days and the structure should present broad-based growth. We forecast that the value added in industry and consumption - in 2Q19 is likely to achieve a similar level as in the 1Q. Therefore, we expect 2Q GDP to be stronger than the 4.7% YoY, which was reported a quarter ago, despite adverse economic conditions in the external environment.

Labour market figures should present a stable, solid expansion. We expect wage to increase in May from 7.1% to 7.4% YoY. Corporate employment growth is likely to remain stable - close to 3% YoY. Overall sentiment remains solid: the number of companies reporting problems with labour shortage is still at a historically high level, which indicates no deterioration in the demand for labour. Similarly, the share of firms mulling over wage increases is relatively high, which suggests that wages should oscillate between 7% and 8% also in the second half of the year.

Hungary: Current account to come out of negative territory?

The only important data regarding Hungary is the current account balance in 1Q19. Based on the monthly data releases, we see the balance to turn into a surplus again after been in negative territory for the past couple of quarters. This is due to the rebound in export-related industrial production, thus trade balance was able to improve significantly.

EMEA and Latam Economic Calendar

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Our view on next week’s key events

- This bundle contains 3 Articles