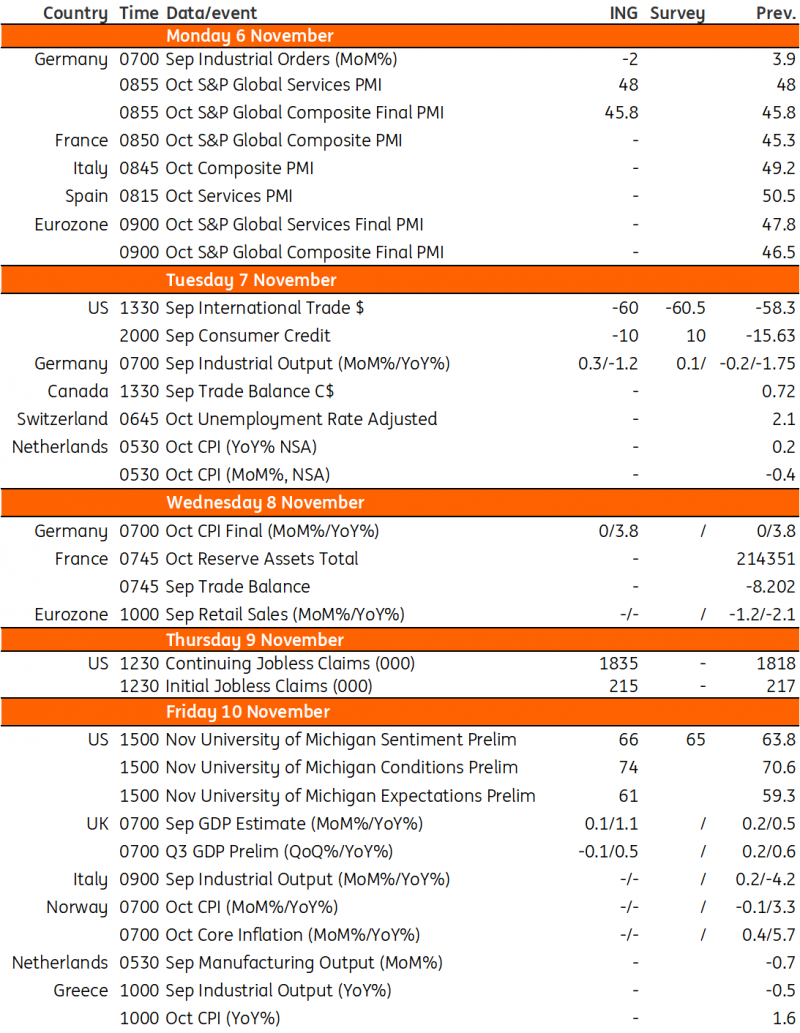

Key events in developed markets next week

Next week will be on the quieter side in the US. The main focus will be on Fed Chair Jerome Powell, who will be appearing on a panel at the upcoming IMF conference. In the UK, all eyes will be on the release of third-quarter GDP data, which we're expecting to come in fractionally negative after a weak July

US: Chair Powell to appear on a panel at the upcoming IMF conference

It is a very quiet week for US data with more interest likely generated by a number of Federal Reserve officials who are scheduled to speak, including Chair Powell, who is appearing on a panel at the upcoming IMF conference. Seven other officials are also speaking and we are likely to hear how much weighting each official puts on the recent tightening of financial conditions brought about by the sharp rise in Treasury yields. In terms of the data we will be looking at the jobless claims numbers, which have been ticking higher latterly. Initial claims remain low, indicating firms are not feeling the pressure to fire people, but with continuing jobless claims now up 160k in the past month and a half it appears that if you do lose your job it is becoming more difficult to find a new one. Meanwhile the hefty falls seen in gasoline prices should prompt a decent bounce in University of Michigan confidence given this measure of sentiment appears to be far more sensitive to cost of living related concerns relative to the Conference Board which appears more influenced by labour market conditions.

UK: third quarter GDP to come in fractionally negative after weak July

July’s monthly GDP came in at -0.6%, and we saw only a partial rebound in August’s figures. Purely mechanically, baring a big rebound in the September growth figures due next week, we suspect that overall third quarter GDP will come in fractionally negative. None of that tells us a huge amount, other than that these figures have been pretty volatile recently. Strike activity seems to offer part of the explanation, but a lot of recent moves in GDP seem to be more noise than signal. Bigger picture, the level of GDP has barely changed since the start of this year and the Bank of England has been clear it expects this stagnation to persist for the next couple of years. While our own forecasts aren’t far off that, and we don’t rule out a recession next year, we’re minded to say the economy is more likely to grow a touch faster over the coming quarters. The average rate on mortgages will climb over coming months as more homeowners refinance. But equally the real wage story is improving, and while the jobs market is cooling, the aggregate impact on consumer spending from what we’ve seen so far is unlikely to be huge. A lot will hinge on whether the deterioration in hiring conditions accelerates over coming months.

Key events in developed markets next week

Download

Download article3 November 2023

Our view on next week’s key events This bundle contains {bundle_entries}{/bundle_entries} articlesThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more