Key events in developed markets next week

- 30 July 2021

- Key Events

Central banks in developed markets are unlikely to shift to a more hawkish stance this week. The US jobs market is still suffering from an insufficient supply of labour, and the Bank of England is waiting of clearer signs of growth

US: No shift in policy stance expected until the jobs market improves

The first week of August sees the release of a couple of key data points that will help to determine whether the Federal Reserve will be pushed into an earlier tapering of its quantitative easing. The Fed persists with its transitory description of inflation pressures and has made it clear we won't see a shift in its policy stance until there is further significant improvement in the jobs market. With six million fewer Americans in work than before the pandemic started, a big rise in non-farm payrolls will go some way to raising expectations of earlier Fed action.

Firms are desperate to hire in order to take advantage of the stimulus-fuelled growth environment, but the issues have been finding suitable staff that are willing and able to do the work. For example, the National Federation of Independent Businesses reports that a record proportion of small businesses have vacancies they cannot fill, and this is stifling the recovery.

Reasons for this include childcare issues, worries about returning to work amid the ongoing pandemic, early retirement and extended and uprated unemployment benefits that may have diminished the financial attractiveness of going to work.

With many states having ceased these extra unemployment benefits, the pool of available workers should in theory be on the rise and we are hopeful that we can see payroll growth around the 900k mark. As schools return to in person tuition in September this pool should increase further, and we expect to see significant jobs growth that will be the catalyst for an eventual December QE taper announcement.

We will also see the ISM manufacturing index which should report strong demand, but again highlight the supply side strains in the economy that are limiting output growth. Extended supplier delivery times, a massive backlog of orders and low customer inventories are all indicative of the supply chain problems bedeviling the US economy. With price rises continuing, companies are able to pass them on to customers given this environment. This is a key factor that leads us to believe inflation pressures will be more persistent than many at the Fed do - hence our expectation of the first interest rate rises coming through in late 2022.

UK: Bank of England unlikely to turn more hawkish, despite recent comments

We expect the Bank of England to strike a cautiously optimistic tone next week – though crucially we’re unlikely to get any fresh hints on the possible timing of future hikes. Nor are we likely to see an early end to the Bank’s QE programme – something that newly-turned BoE hawk Michael Saunders has recently advocated.

While the Bank is likely to raise its inflation forecast for this year, the near-term growth outlook has become clouded by the rise in Covid-19 prevalence. Meanwhile markets are already pricing a modest amount of tightening over the next year or two, and that suggests little need for the Bank to signal a more concrete timeline for rate hikes just yet.

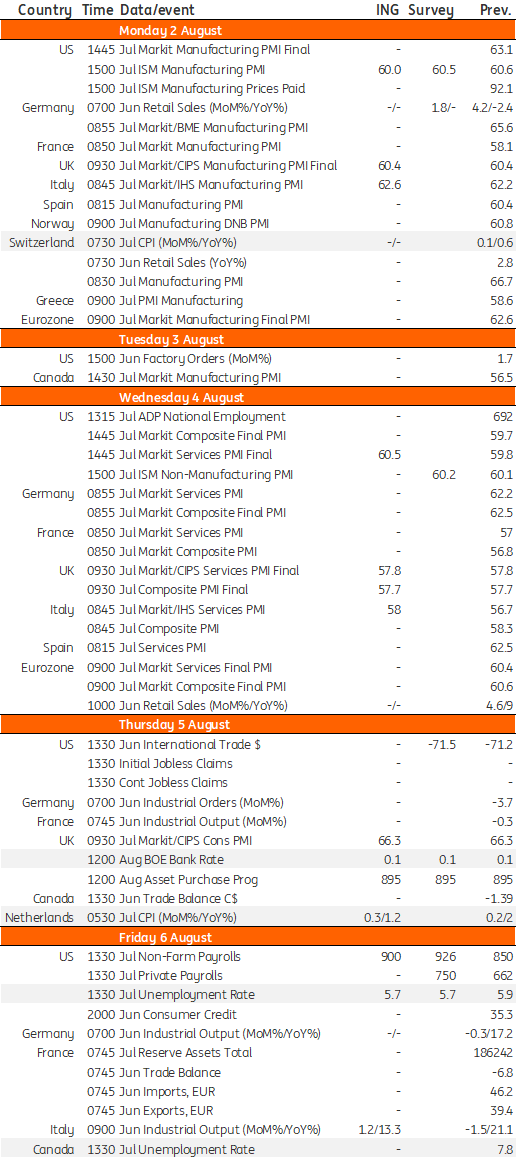

Developed Markets Economic Calendar

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Our view on next week’s key events

- This bundle contains 3 Articles