Key events in developed markets next week

- 20 October 2023

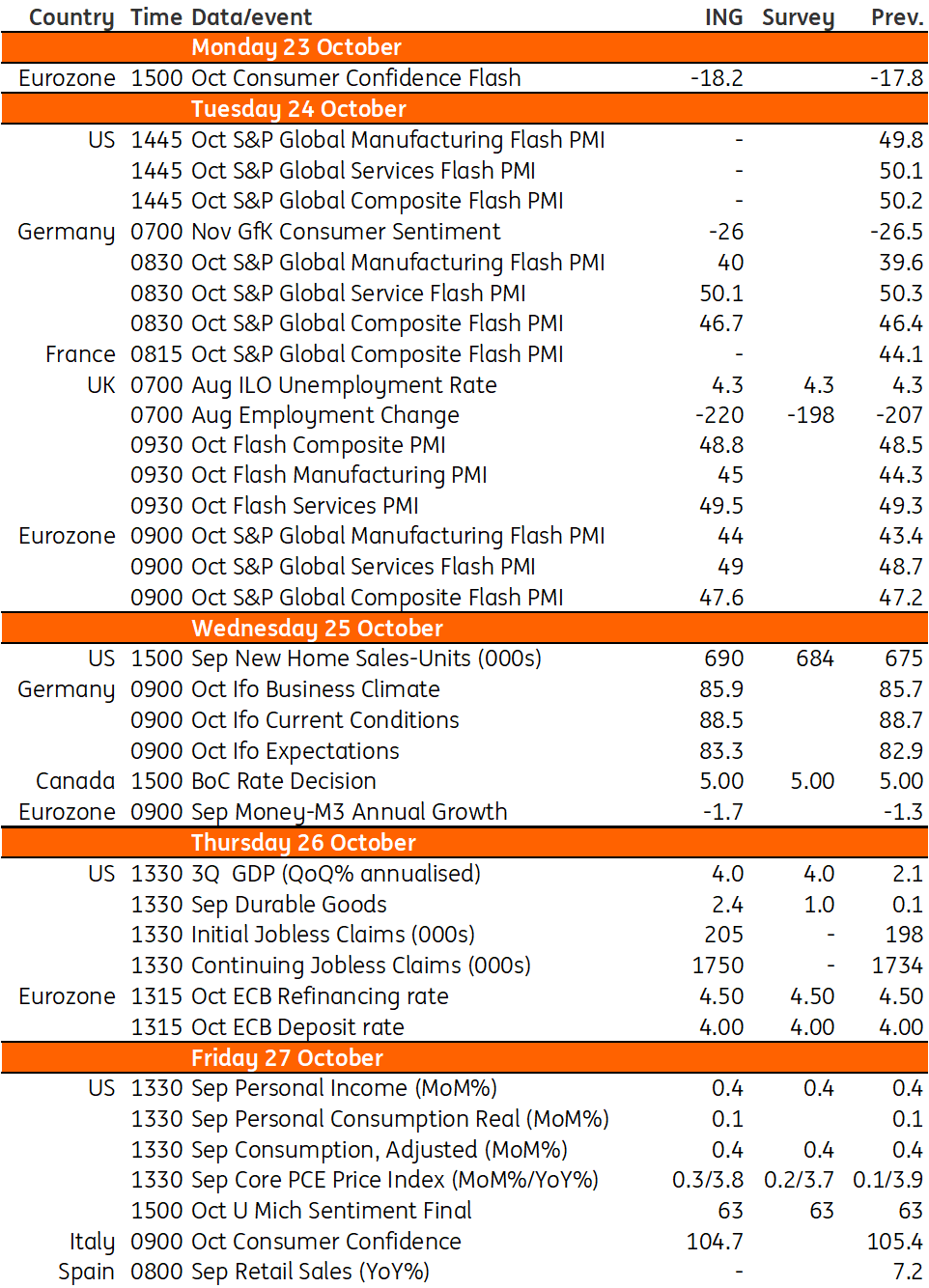

Following the recent strength in activity data in the US, we see third-quarter GDP growth coming in at a robust 4% next week. Elsewhere, all eyes will be on the upcoming European Central Bank meeting, as well as jobs data and PMI releases in the UK ahead of the Bank of England's November meeting. The Bank of Canada is also likely to keep rates on hold

US: Third-quarter GDP growth to come in at around 4%

Federal Reserve officials continue to suggest that they will likely hold rates steady for the second consecutive time at the upcoming FOMC meeting despite US economic activity remaining hot, the jobs market tight, and inflation still well above target. Policymakers continue to talk about long and variable lags when it comes to the economic impact of monetary policy changes, but the bigger factor is the recent sharp run-up in Treasury yields. This is pushing consumer and corporate borrowing costs higher, with mortgage rates fast approaching 8% and credit card borrowing costs at record highs. This significant tightening of lending conditions will increasingly act as a major headwind to economic activity and should lead to a moderation in growth and help dampen inflation pressures more broadly.

For now, however, activity numbers remain strong, with the highlight being third-quarter GDP. We look for it to come in at around 4%, boosted by strong consumer spending. Leisure and tourism spending has been particularly firm, while residential investment should also contribute positively together with government spending. We will also see the Fed’s favoured measure of inflation, the core personal consumer expenditure deflator. Energy prices will lift the headline rate and we are not as optimistic that core inflation will rise just 0.2% month-on-month or 3.7% year-on-year as the market expects. We fear slight upside risks, and this combination of elevated inflation and strong growth could be the catalyst for the 10Y Treasury yield to clearly break above 5%.

Eurozone: Broad consensus is for no hike as the ECB has already reached a record high

Next week’s events will be dominated by the European Central Bank (ECB) rate decision on Thursday. The broad consensus is for no hike as the ECB has already reached a record high, inflation is becoming more benign and the economy is weakening rapidly. Still, higher oil prices and continued labour market strength keep upside risks to inflation alive. Thursday’s meeting will therefore mainly be about whether the ECB gives off any clear messages on a possible final hike in December. We think the chances of another hike are low.

Don’t count out the PMI on Tuesday in terms of market impact. While much less relevant than the ECB meeting, it has caused some movement in recent months as weakening economic data from the eurozone has raised concerns over a possible downturn. A downbeat reading for the PMI would be negative for euro sentiment as it would increase expectations of a recession. We expect that the economic environment is currently broadly stagnant, but a recession is never far away.

UK: Jobs data and PMIs in focus as BoE is set for November pause

With a couple of weeks to go until the next Bank of England meeting, it looks like the stage is set for another on-hold decision. We've already had the all-important services inflation and wage numbers, and while they're too high for policymakers' liking, neither provided a big enough upside surprise to pressure the committee into another rate hike next month.

Next week brings flash PMIs, which might improve fractionally but suggest the dominant UK service sector is under pressure. We'll also get delayed jobs market data, which has been pointing to a rise in unemployment over recent months. But the survey is suffering from dwindling response rates, hence the delay, and there are clear question marks over how much weight we should be ascribing to these figures. The Bank will certainly treat them with a pinch of salt when the committee meets next.

Canada: Focus on the BoC's interest rate decision with no change expected

In Canada, the focus will be on the Bank of Canada's interest rate decision. What was a 50-50 call on a 25bp rate hike four weeks ago has now come down to look much more like a 20-80 chance in favour of no change, thus keeping it at 5%. Economic activity surprisingly contracted in the second quarter and flatlined in July, while the latest inflation numbers were more benign than expected. The jobs market remains strong though, and the BoC will likely keep the option of a future hike on the table, but we believe interest rates have most probably peaked.

Key events in developed markets next week

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Our view on next week’s key events

- This bundle contains 3 Articles