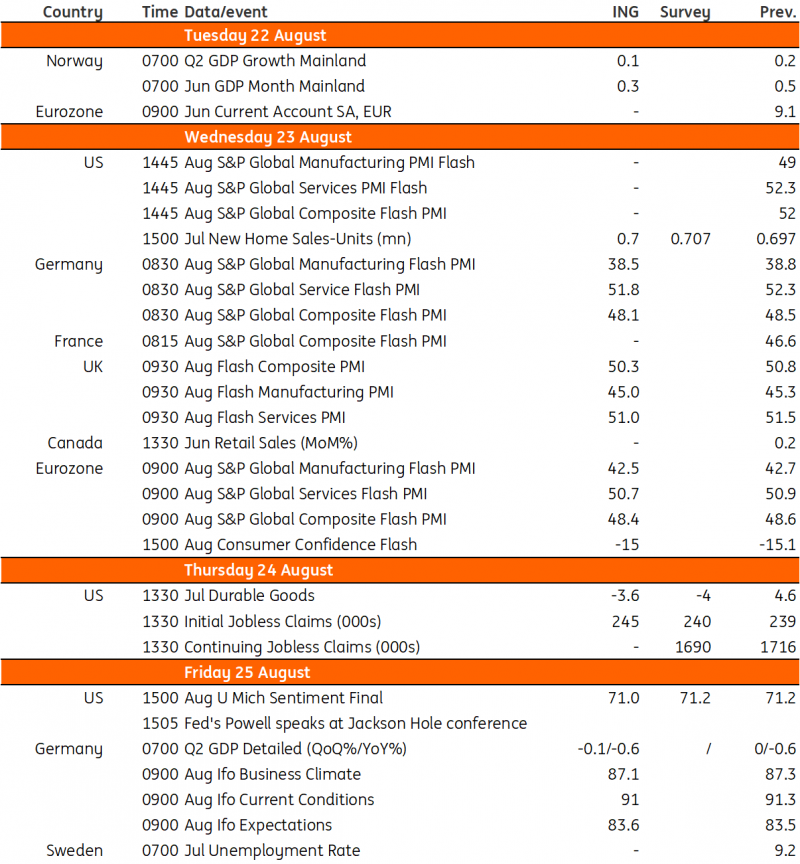

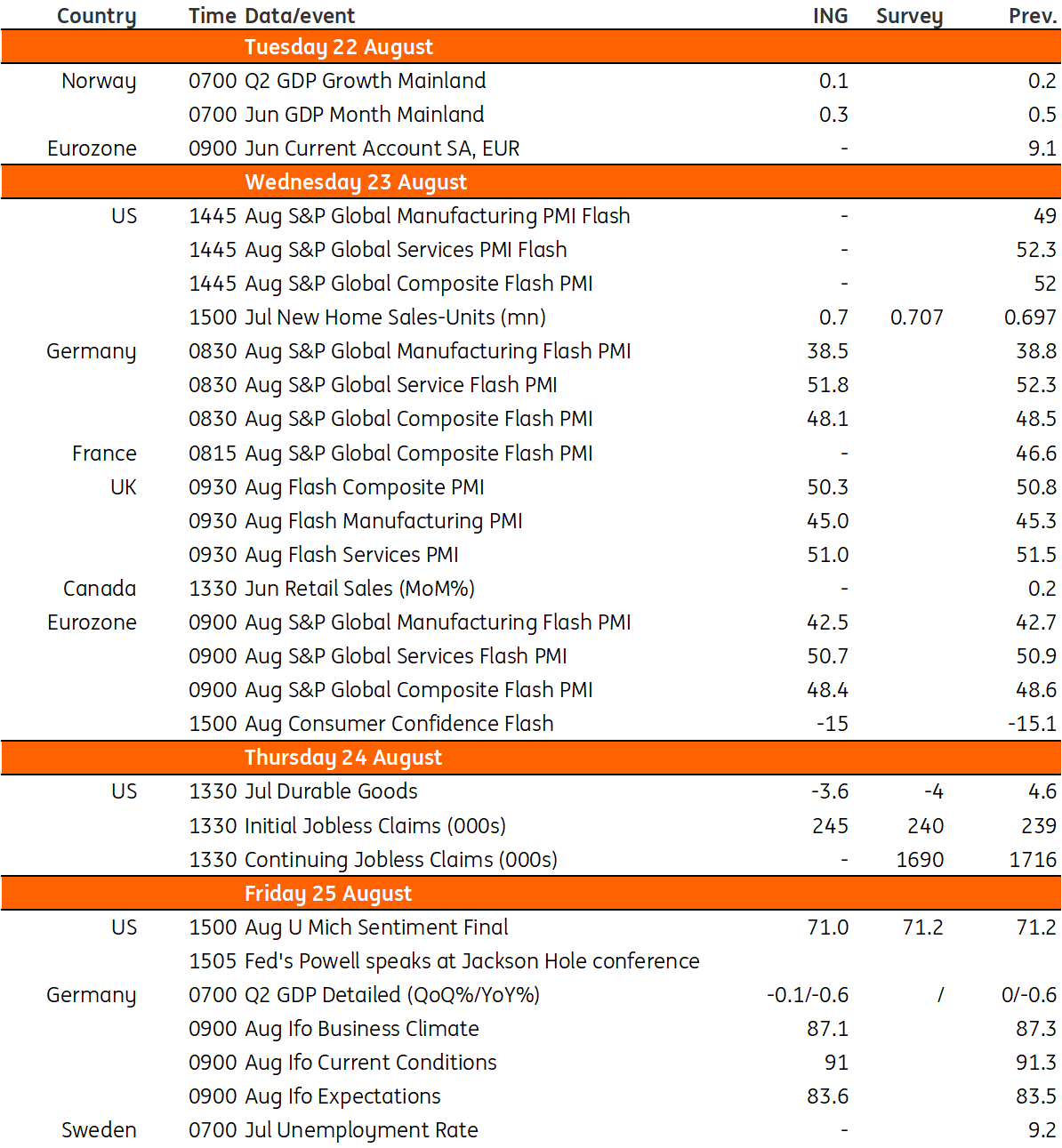

Key events in developed markets next week

The focus in the US next week will be on Fed Chair Jerome Powell's speech on Friday morning. Meanwhile, the eurozone sentiment data releases will give an idea of whether third-quarter performance continues to be bleak. All eyes will be on PMI releases in the UK with policymakers looking for inflation clues

US: The market's focus will be Fed Chair Jerome Powell's speech

Treasury yields have come under significant upward pressure over the past couple of weeks in the wake of the Fitch credit rating downgrade of US government debt and ongoing strong data that has cast doubt on how aggressive eventual Federal Reserve interest rate cuts will be. Interestingly, near-term interest rate expectations for Federal Reserve monetary policy have changed little with just 3bp of tightening priced for the September FOMC meeting and 10bp in total priced for November.

The highlight next week will be the Fed’s Jackson Hole Symposium at which the outlook for monetary policy will be heavily discussed. The market’s focus will be Fed Chair Jerome Powell’s speech on Friday morning. Given slowing inflation, more moderate labour cost developments, and weaker hiring despite strong activity, we think he will back the case for a September pause, but leave the door open to a further possible rate rise in either November or December depending on how the incoming information pans out.

Our view is that the lagged effects of higher interest rates and of rapidly tightening lending conditions will mean that this final hike will not be required, while the exhaustion of pandemic-era savings and the restart of student loan repayments will act as an additional brake on economic activity that will also contribute to ongoing falls in inflation.

Eurozone: PMI tells a story of weakening performance

Next week is about sentiment data for the eurozone. With PMIs steadily sliding in recent months and the composite PMI now well below 50, next week will be all about gauging whether the third quarter continues to look bleak in terms of economic performance. While the second quarter actually turned out better than expected in terms of GDP growth, the PMI tells a story of weakening performance and it will be key to see whether August added to that or nuanced the picture somewhat.

UK PMIs in focus as policymakers look for inflation clues

Like in the eurozone, we'd expect the UK PMIs to highlight mounting stagnation in the service sector, coupled with ongoing problems in manufacturing. On the former, the Bank of England will be most interested in whether the surveys point to improvements in the inflation story, and the anecdotal evidence in the last PMI press release from S&P Global suggests the answer is 'yes'.

It highlighted the fact that lower energy prices are taking the pressure off output price inflation from companies, and we expect this trend to continue. That said, the BoE seems to have limited faith in surveys, which have been pointing to a better inflation story for months, but have thus far failed to translate into improvements in the official data. We continue to expect a September hike, but we're hopeful that some modest improvement in services inflation can enable the committee to pause in November.

Key events in developed markets

Download

Download article18 August 2023

Our view on next week’s key events This bundle contains {bundle_entries}{/bundle_entries} articles

{kind=link}

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more