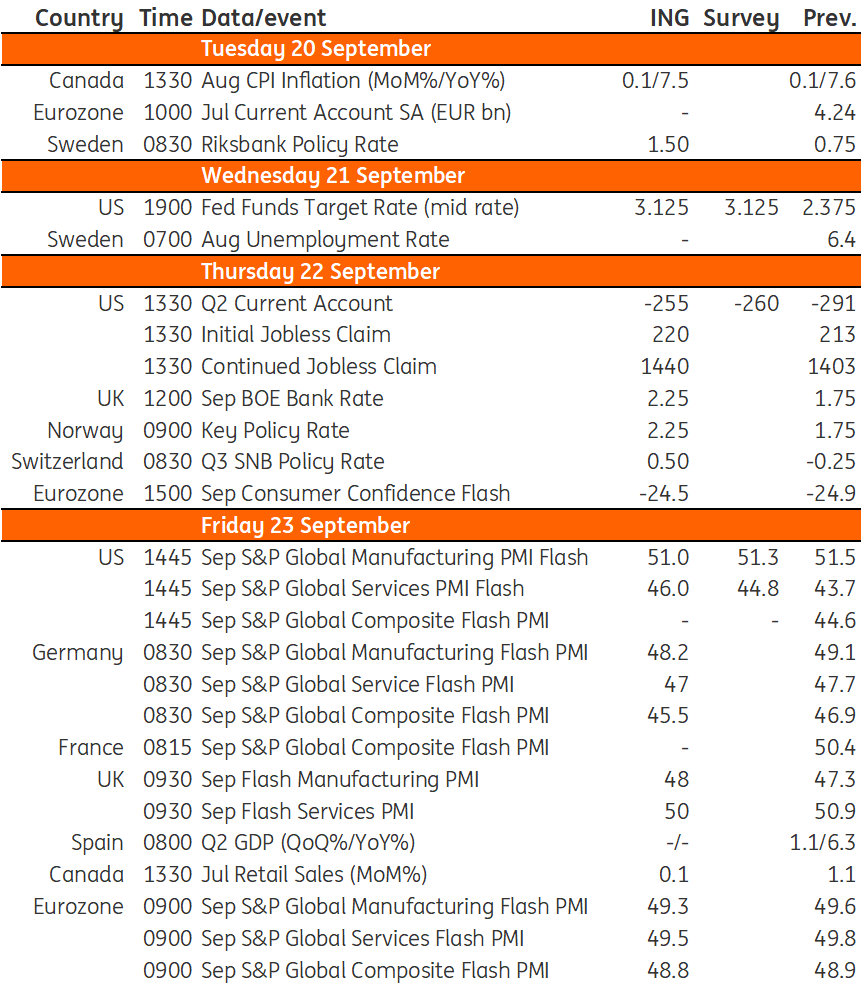

Key events in developed markets next week

- 16 September 2022

- Key Events

Next week is packed with central bank meetings. The Fed is likely to match the European Central Bank in hiking rates by 75bp, while the Bank of England and Norges Bank are expected to make 50bp moves

US: 75bp is our favoured call, however there's a chance for the Fed to go even further

All eyes will be on the Federal Reserve meeting next Wednesday. The market was favouring a 75bp hike ahead of the August CPI report, but the much higher-than-expected inflation print has seen the market price in a 20% chance that the Fed will go over and above that by opting for 100bp. A 75bp hike is still our favoured call, but we acknowledge the risk that with inflation proving to be stickier than we had suspected, the subsequent meetings in November and December could see more aggressive action from the Fed than we are currently pencilling in. While the geopolitical backdrop, the China slowdown story, the potential for energy rationing in Europe, the strong dollar and fragile-looking domestic equity and housing markets argue for a more moderate path of tightening in the coming months, if inflation momentum doesn’t slow the bank will hike by a further 75bp in November and possibly 50bp in December. The message from the Fed next week is likely to emphasise data dependency, but its updated economic forecasts are likely to show the end-2022 Fed funds rate at 4.125% rather than 3.4% (July forecast) and we suspect it will be kept at that for 2023, before dropping back to a long-term average rate of 2.5%.

UK: Bank of England to stick to 50bp rate hike despite Fed and ECB doing more

We narrowly favour a 50bp hike on Thursday, taking the Bank Rate to 2.25%, although 75bp is clearly on the table and we would expect at least a couple of policymakers to vote for it. The announcement of an energy price cap from the government will drastically lower near-term CPI, reducing concerns about consumer inflation expectations becoming de-anchored and reducing the urgency to act even more aggressively. However, the hawks will be worried about the recent independent sterling weakness, and will also argue that the government’s support package could increase medium-term inflation given it reduces the risk of recession.

That means it’s a close meeting to call, but if we’re right and the committee does move more cautiously than the Fed and ECB next week, then we expect another 50bp move in November and at least another 25bp in December. That would take Bank Rate to the 3% area. Read our full Bank of England Preview here.

Sweden: Riksbank to match ECB’s 75bp hike – and there’s a risk of more

With only two meetings left this year, and facing higher-than-expected inflation and a tight jobs market, we expect the Riksbank to hike rates by at least 75bp on Tuesday. We expect a repeat move in November.

Norway: Norges Bank to repeat August’s 50bp rate hike

Norway’s central bank stepped up the pace of rate hikes in August, and core inflation has continued to push higher than Norges Bank’s most recent forecasts in June. The message from the August meeting was that the central bank is keen to continue front-loading tightening, and we expect another 50bp hike next week. That would take the deposit rate to 2.25%, and we’d expect another 50bp move in November.

Switzerland: SNB will follow the lead of other central banks and hike rates by 75bp

The Swiss National Bank (SNB) meets next week and is ready to raise its key interest rate for a second time, after the 50bp increase in June. Inflation in Switzerland stood at 3.5% in August, still above the SNB's target of 0-2%, although well below the inflation rate in neighbouring countries. The fact that the Swiss franc is relatively strong against the euro is no longer a problem for the SNB, as it reduces imported inflation. The SNB focuses much more on the real exchange rate, which takes into account the inflation differential and has remained very stable in recent months. With no fears of too much appreciation and with inflation above target, there is little reason for the SNB not to follow the lead of other central banks, especially as it only meets once every quarter, so the next meeting will be in December, while the ECB and the Fed will meet in between. We expect a 75bp rate hike next week.

Eurozone: PMIs expected to remain below 50

In the eurozone, we get the first look at economic activity in September with PMIs due on Friday. After two months below 50, we expect another one to follow as manufacturing production cuts due to high energy prices and the end of the tourist season are set to impact business activity. Consumer confidence will also be released next week, where we expect confidence to remain near historical lows for the moment as the cost-of-living crisis continues.

Key events in developed markets next week

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Our view on next week’s key events

- This bundle contains 3 Articles