Key events in developed markets next week

- 12 May 2023

- Key Events

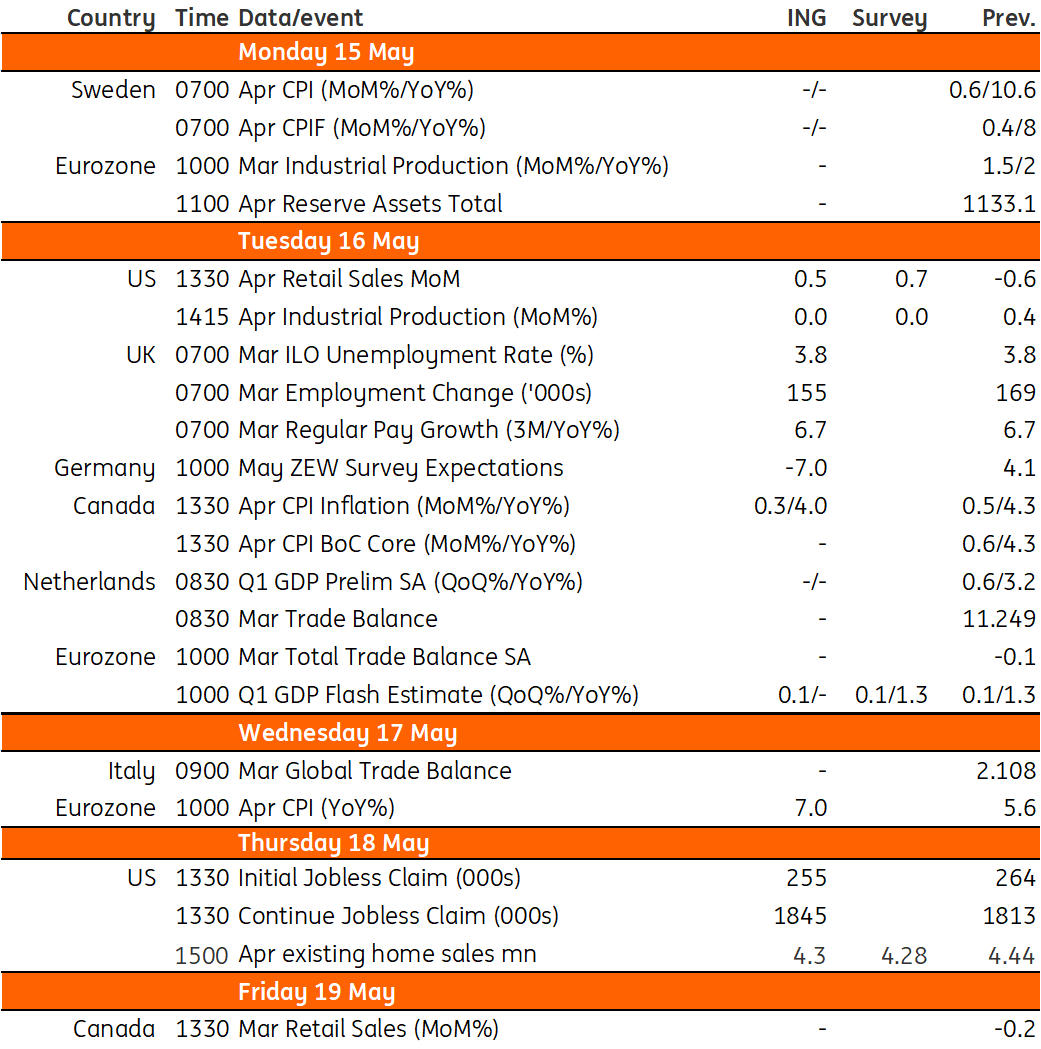

Retail sales and industrial production are the highlights for US data next week. The former should get a lift from robust auto sales, while the latter will be held back by falling production. As for UK's wage growth data next Tuesday, the last couple of month's readings have been more benign, and the Bank's own business survey points to a moderation in growth

US: Initial jobless claims moving higher due to surge in lay-offs

Markets are increasingly confident that the Federal Reserve has implemented its final rate hike and we will see a pause at the June Federal Open Market Committee meeting. In fact, the next move is now priced to be a cut in September with the prospect of 75bp of rate cuts before the end of the year. Next week we will get a raft of Federal Reserve officials offering their views on the state of the economy and they are likely to continue pushing back against the market pricing given inflation continues to run hot and the jobs market remains tight. Nonetheless, the banking story is likely to dominate market sentiment with the fear that tightening lending conditions will weigh heavily on the economy and could be enough to tip it into recession.

In terms of data, we have retail sales and industrial production as the highlights. Retail sales will probably get a lift from the robust auto sales numbers for April. Outside of this component, the release will be softer with credit card figures pointing to very modest growth on most items. Industrial production will also be held back by the fact that manufacturing surveys continue to point to falling production with lower energy prices limiting the upside for oil and gas extraction.

Home sales numbers are also released and will probably soften given the decline witnessed in mortgage applications for home purchases. Also, pay close attention to initial jobless claims which now appear to be moving higher as a lagged response to the surge in job lay-off announcements.

UK: Wages data to help determine June rate hike probability

The Bank of England has made it pretty clear that the decision on whether to hike again in June will come down to the two sets of wages and inflation data out before the next meeting. Wage data has been volatile recently, and last month’s surprise increase in regular pay growth followed a couple of months of more benign readings. We’ll get another reading on Tuesday, but the BoE’s own survey of businesses has been pointing to a moderation in wage growth. Assuming we see fresh signs of that in the official data before the June meeting, and barring a surprise resurgence in services inflation, we think the Bank will be comfortable with pausing rate hikes next month.

Key events in developed market next week

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Our view on next week’s key events

- This bundle contains 3 Articles